City

of hobart

AGENDA

Finance and Governance Committee Meeting

Open Portion

Tuesday, 16 October 2018

at 5.00 pm

Lady Osborne Room, Town Hall

City

of hobart

AGENDA

Finance and Governance Committee Meeting

Open Portion

Tuesday, 16 October 2018

at 5.00 pm

Lady Osborne Room, Town Hall

THE MISSION

Our mission is to ensure good governance of our capital City.

THE VALUES

The Council is:

|

about people |

We value people – our community, our customers and colleagues. |

|

professional |

We take pride in our work. |

|

enterprising |

We look for ways to create value. |

|

responsive |

We’re accessible and focused on service. |

|

inclusive |

We respect diversity in people and ideas. |

|

making a difference |

We recognise that everything we do shapes Hobart’s future. |

|

|

Agenda (Open Portion) Finance and Governance Committee Meeting |

Page 3 |

|

|

16/10/2018 |

|

Business listed on the agenda is to be conducted in the order in which it is set out, unless the committee by simple majority determines otherwise.

APOLOGIES AND LEAVE OF ABSENCE

1. Co-Option of a Committee Member in the event of a vacancy

3. Consideration of Supplementary Items

4. Indications of Pecuniary and Conflicts of Interest

6.1 2017-18 Financial Statements

6.2 Occupancy Rates - Multi-Storey Car Parks

6.3 Council Committees - Quorums

6.4 Aldermanic Development and Support Policy - International Relations.

6.5 Complaints Against the Principles of the Customer Service Charter 2017/18

6.6 Hobart Town Hall Ballroom - Acoustics

6.7 Waste Strategy Summit - 26 to 28 June 2018

6.8 Conference Reporting - Include Conference - August 2018 Wrest Point

7 Motions of which Notice has been Given

7.1 kunanyi/Hobart Visitation Policy and Strategy

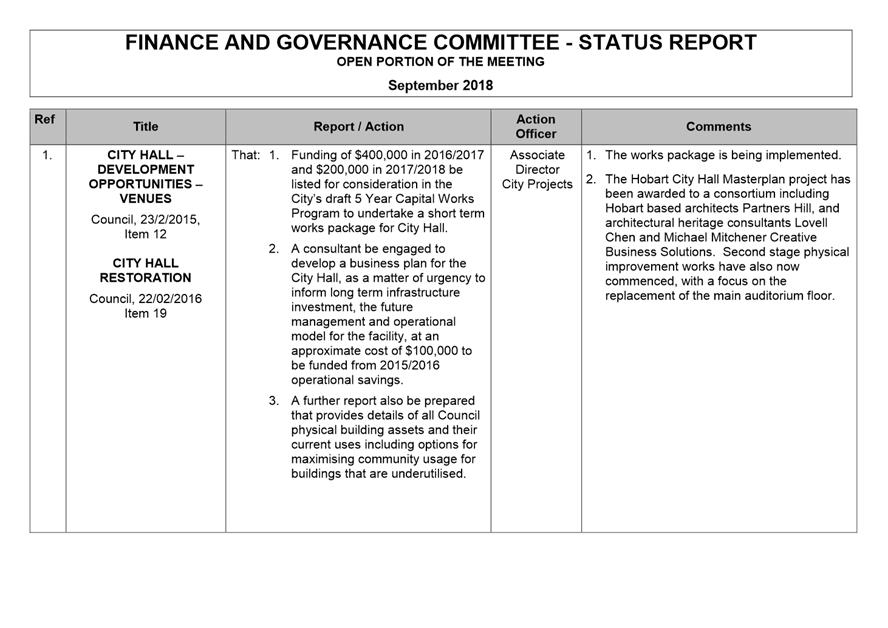

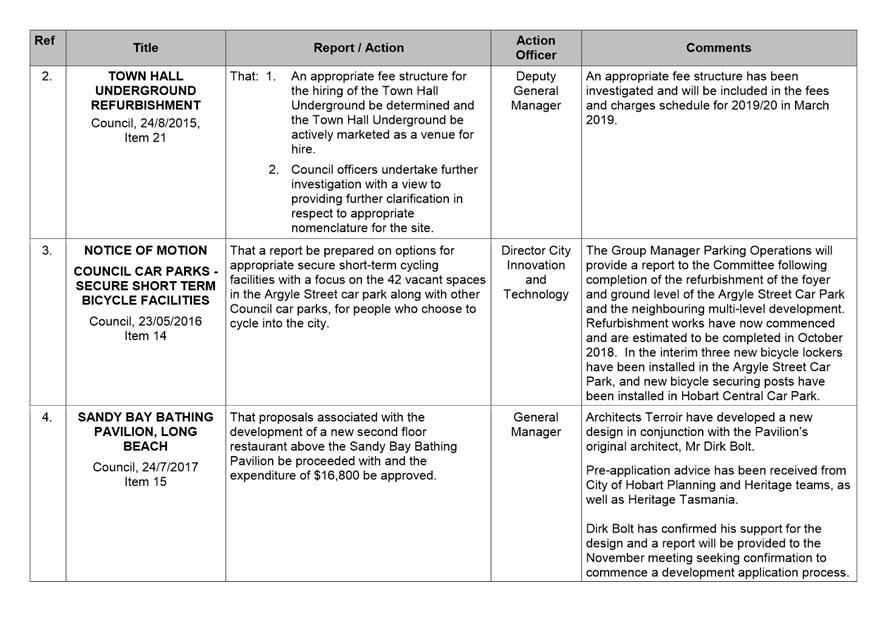

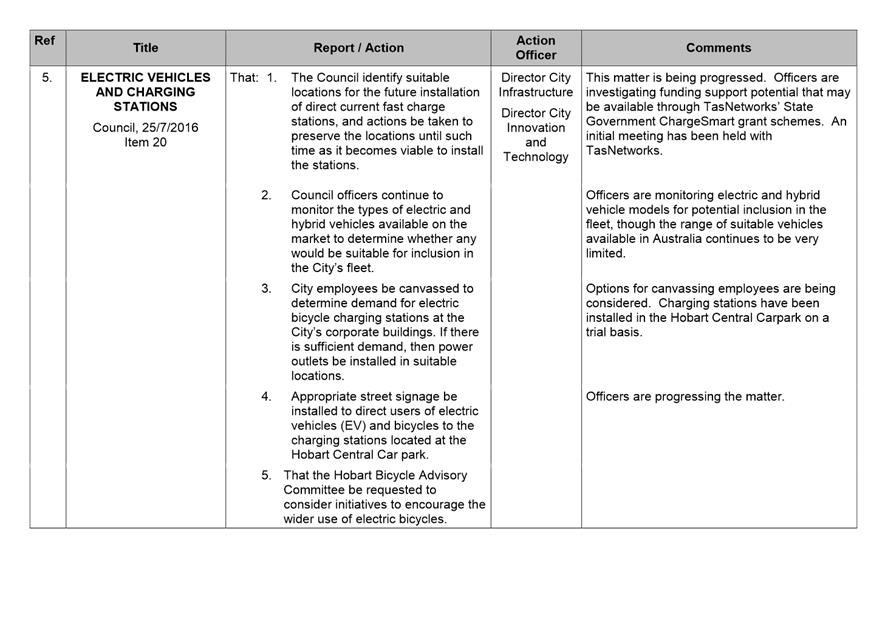

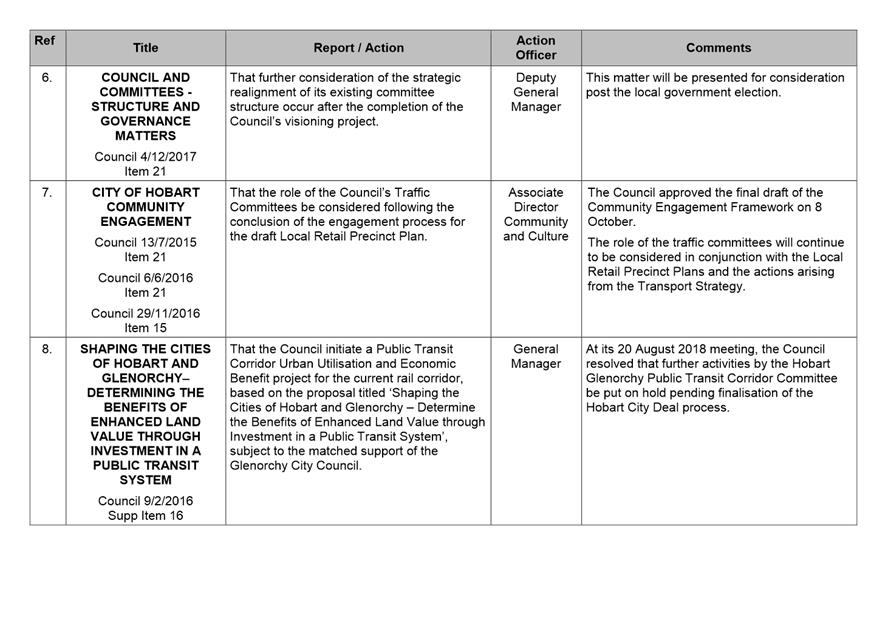

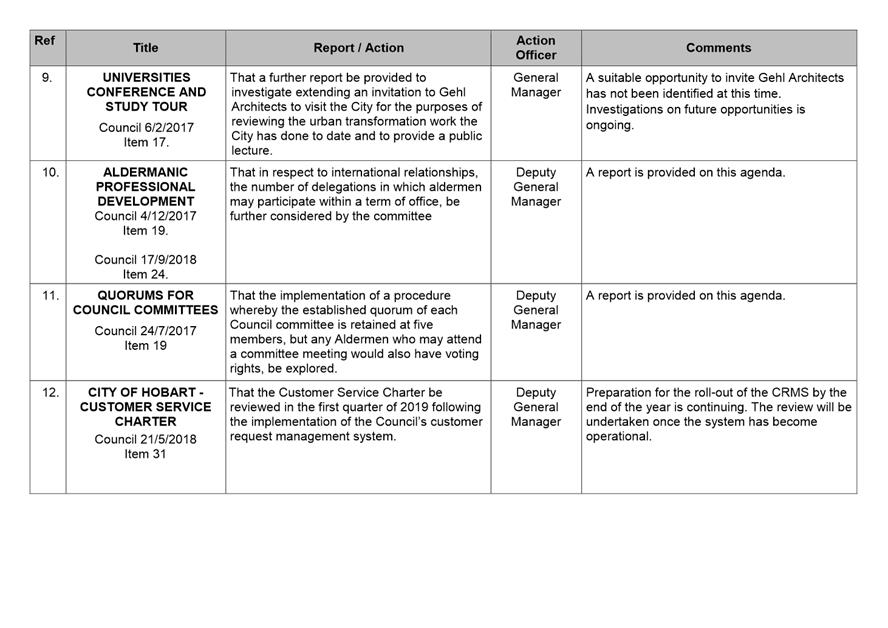

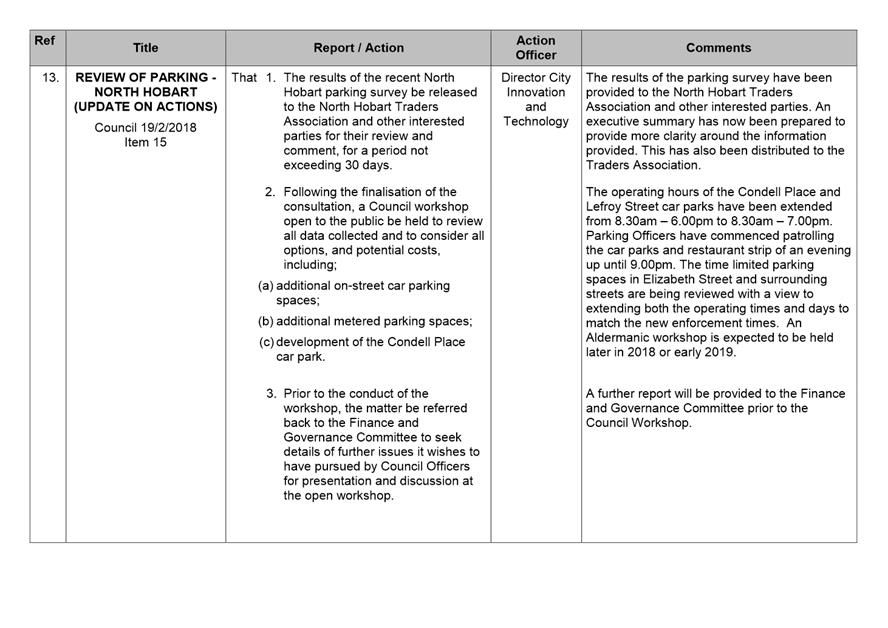

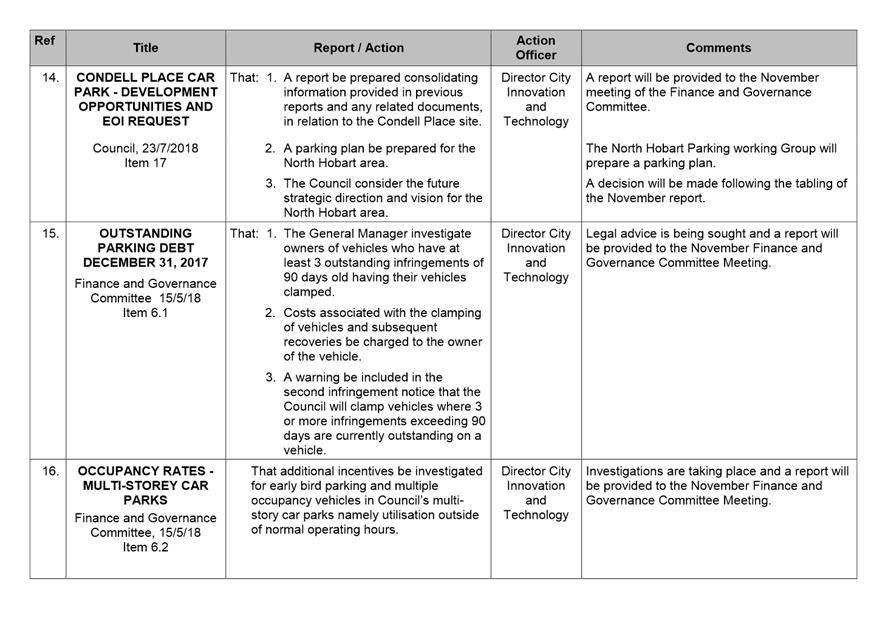

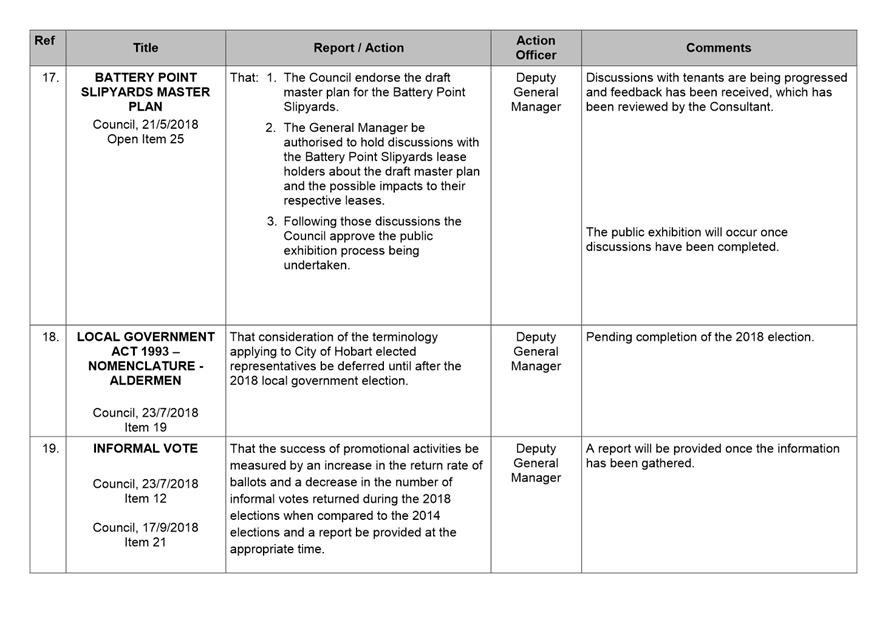

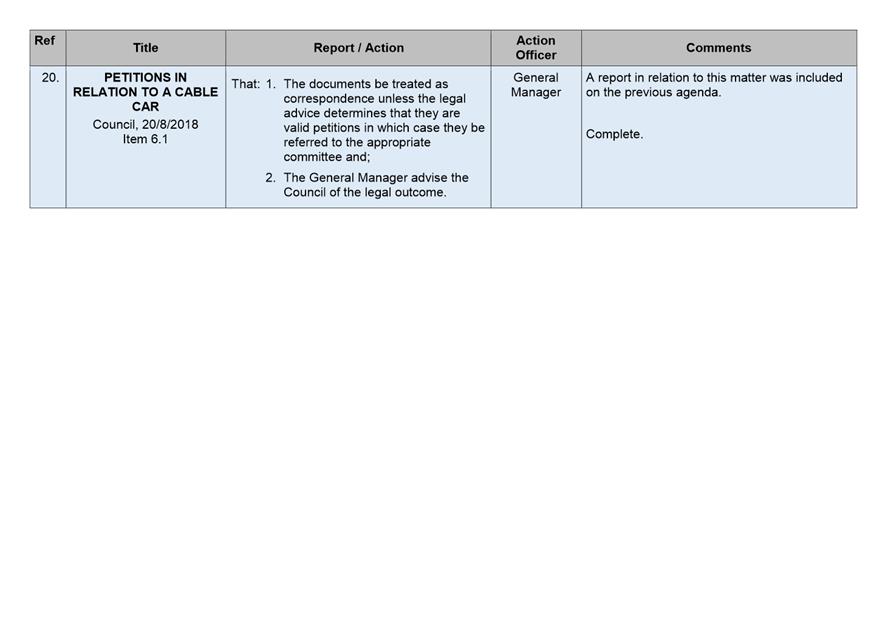

8 Committee Action Status Report

8.1 Committee Actions - Status Report

9. Responses to Questions Without Notice

9.1 Potential Mapping of Council Services

9.2 Development of an International Association for Public Participation Program for Aldermen

11. Closed Portion Of The Meeting

|

|

Agenda (Open Portion) Finance and Governance Committee Meeting |

Page 5 |

|

|

16/10/2018 |

|

Finance and Governance Committee Meeting (Open Portion) held Tuesday, 16 October 2018 at 5.00 pm in the Lady Osborne Room, Town Hall.

|

COMMITTEE MEMBERS Ruzicka (Joint Chairman) Thomas (Joint Chairman) Lord Mayor Christie Deputy Lord Mayor Sexton Zucco Cocker Reynolds

ALDERMEN Briscoe Burnet Denison Harvey |

Apologies: Nil

Leave of Absence: Nil

|

|

The minutes of the Open Portion of the Finance and Governance Committee meeting held on Tuesday, 11 September 2018, are submitted for confirming as an accurate record.

|

Ref: Part 2, Regulation 8(6) of the Local Government (Meeting Procedures) Regulations 2015.

|

That the Committee resolve to deal with any supplementary items not appearing on the agenda, as reported by the General Manager.

|

Ref: Part 2, Regulation 8(7) of the Local Government (Meeting Procedures) Regulations 2015.

Aldermen are requested to indicate where they may have any pecuniary or conflict of interest in respect to any matter appearing on the agenda, or any supplementary item to the agenda, which the committee has resolved to deal with.

Regulation 15 of the Local Government (Meeting Procedures) Regulations 2015.

A committee may close a part of a meeting to the public where a matter to be discussed falls within 15(2) of the above regulations.

In the event that the committee transfer an item to the closed portion, the reasons for doing so should be stated.

Are there any items which should be transferred from this agenda to the closed portion of the agenda, or from the closed to the open portion of the agenda?

|

Agenda (Open Portion) Finance and Governance Committee Meeting |

Page 7 |

|

|

|

16/10/2018 |

|

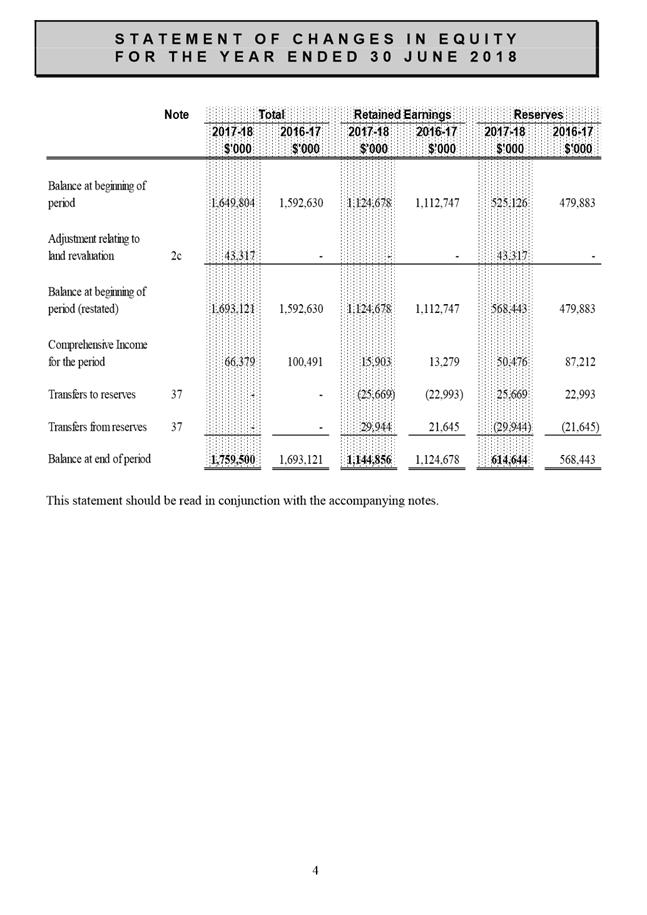

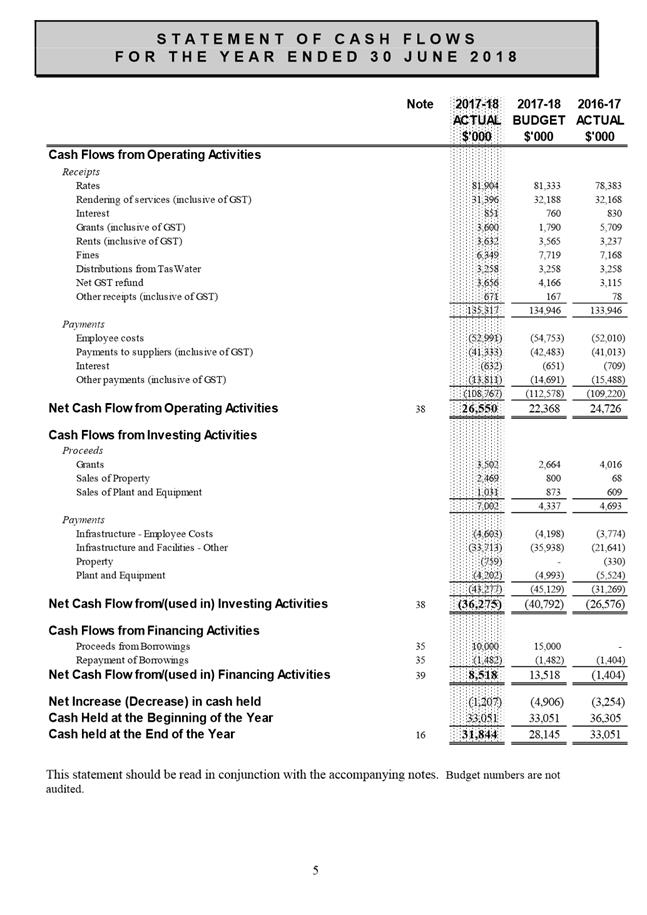

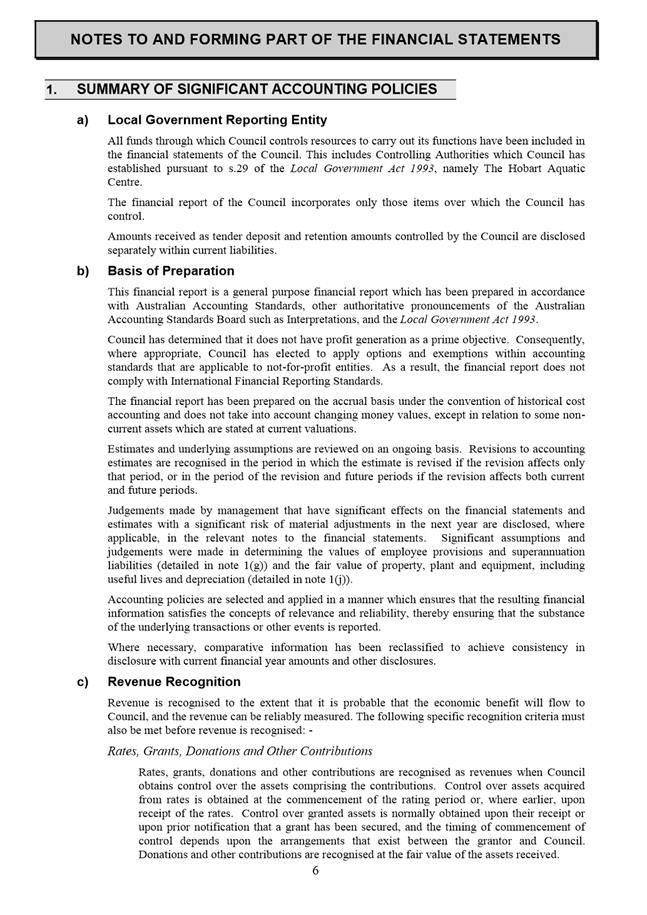

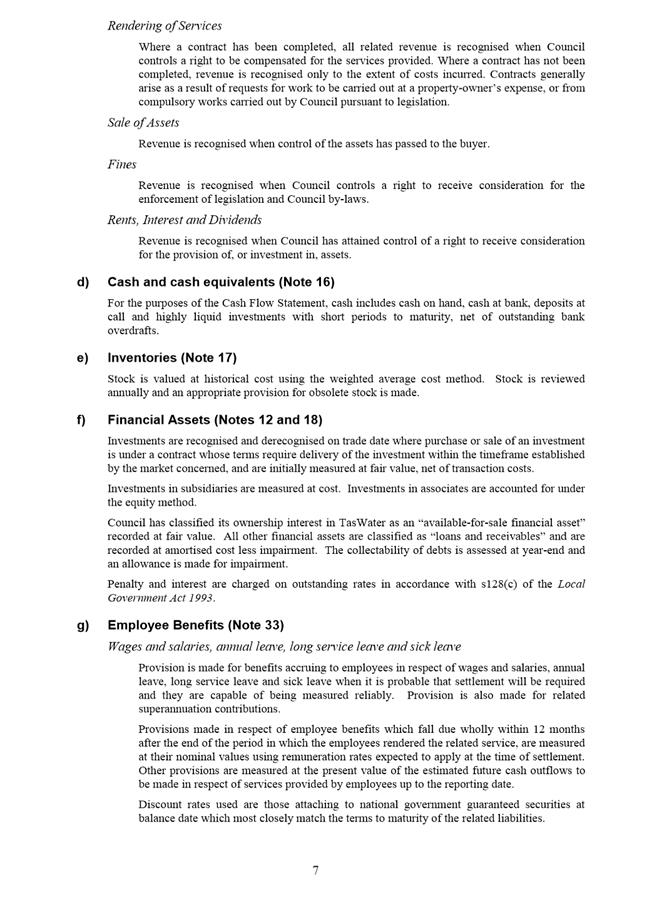

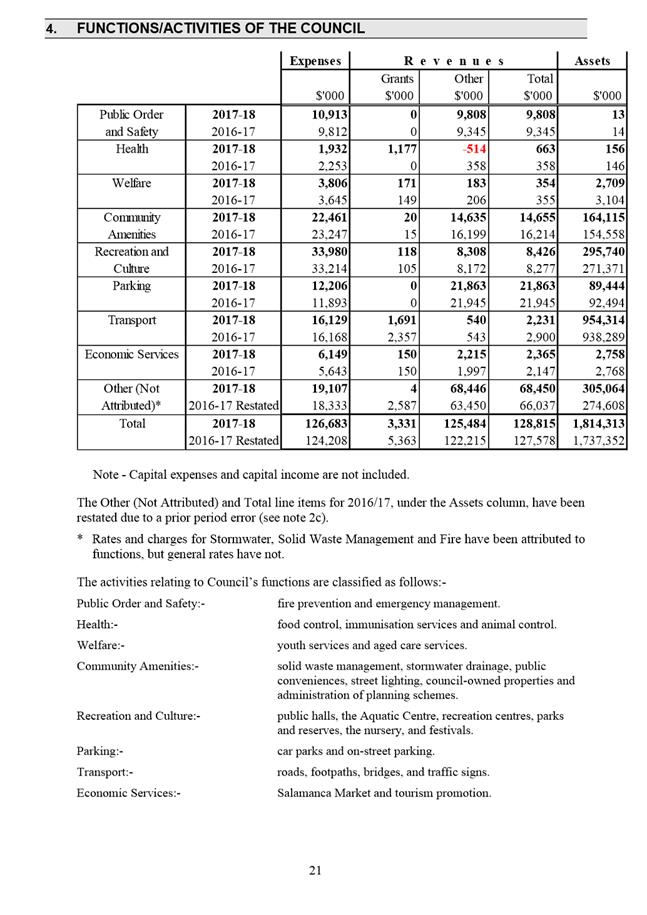

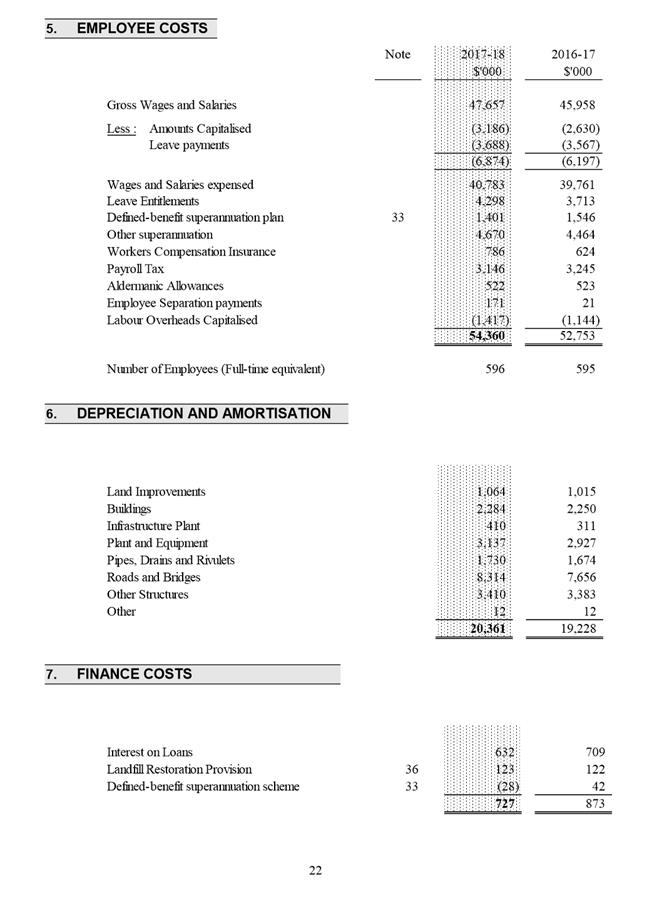

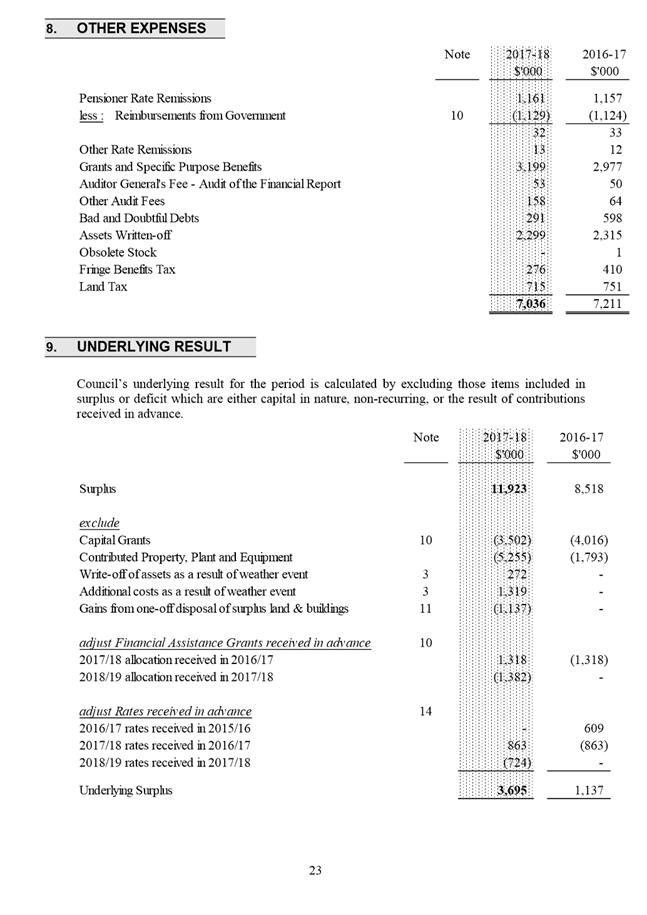

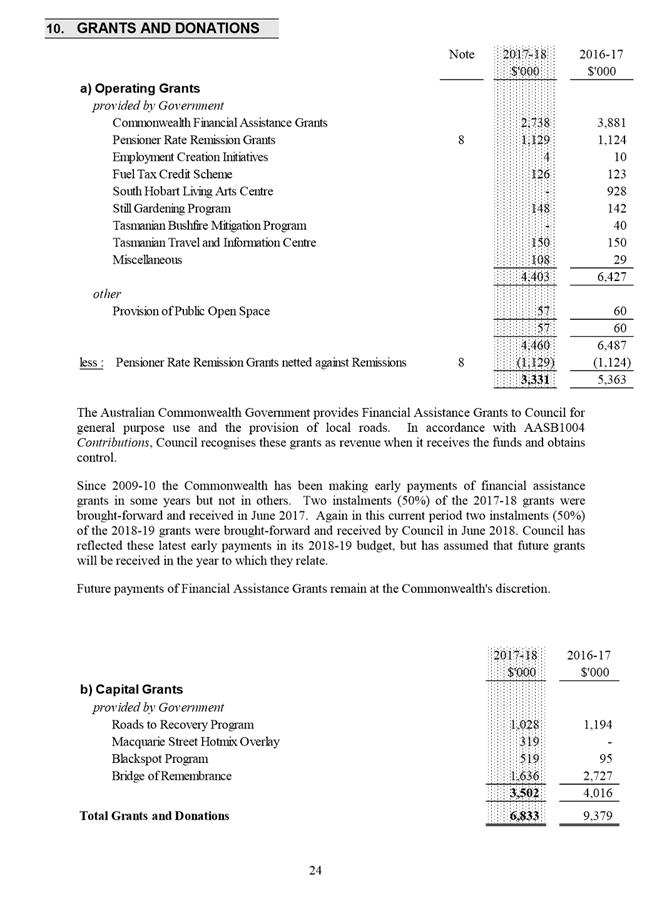

6.1 2017-18 Financial Statements

Report of the Director Financial Services and the Manager Finance of 11 October 2018 and attachments.

Delegation: Council

|

Item No. 6.1 |

Agenda (Open Portion) Finance and Governance Committee Meeting |

Page 8 |

|

|

16/10/2018 |

|

REPORT TITLE: 2017-18 Financial Statements

REPORT PROVIDED BY: Director Financial Services

Manager Finance

1. Report Purpose and Community Benefit

1.1. The purpose of this report is to present the financial statements for the year ended 30 June 2018 for adoption by Council.

2. Report Summary

2.1. The Council’s financial statements for the year ended 30 June 2018 have been prepared and independently audited.

2.2. The Auditor-General has completed his audit and issued an unqualified audit opinion on the financial statements (see Attachments B and C).

2.3. The financial statements demonstrate that Council remains in a strong sustainable financial position, achieving benchmarks for all financial sustainability indicators.

2.4. Council’s 2017-18 underlying surplus of $3.695 million is more than both the original 2017-18 budget position and the most recent 2017-18 forecast.

2.5. At its meeting on 21 September 2015 Council resolved that annually, as part of the review of the September quarter financial report, the Council consider the prior year’s operating result – it’s size and what, if anything, to allocate it to. Therefore, further information on the 2017-18 operating surplus in excess of budget will be provided as part of the September quarter financial report.

|

That the Council formally adopt the financial statements for the year ended 30 June 2018 marked as Attachment A to this report.

|

4. Background

4.1. The financial statements for the year ended 30 June 2018 have been prepared on a consistent basis with prior years.

4.2. The financial statements were presented to the Risk and Audit Panel on 7 August 2018 and received the endorsement of that Panel subject to the following changes: -

4.2.1. Updating the value of Council’s ownership interest in TasWater,

4.2.2. Updating wording in note 2b on quantitative impacts from new and revised Accounting Standards and Interpretations not yet adopted, and

4.2.3. Other minor presentation changes.

4.3. The financial statements were delivered to the Auditor-General on 14 August 2018.

4.4. The Auditor-General requested a number of changes to the financial statements, including the following: -

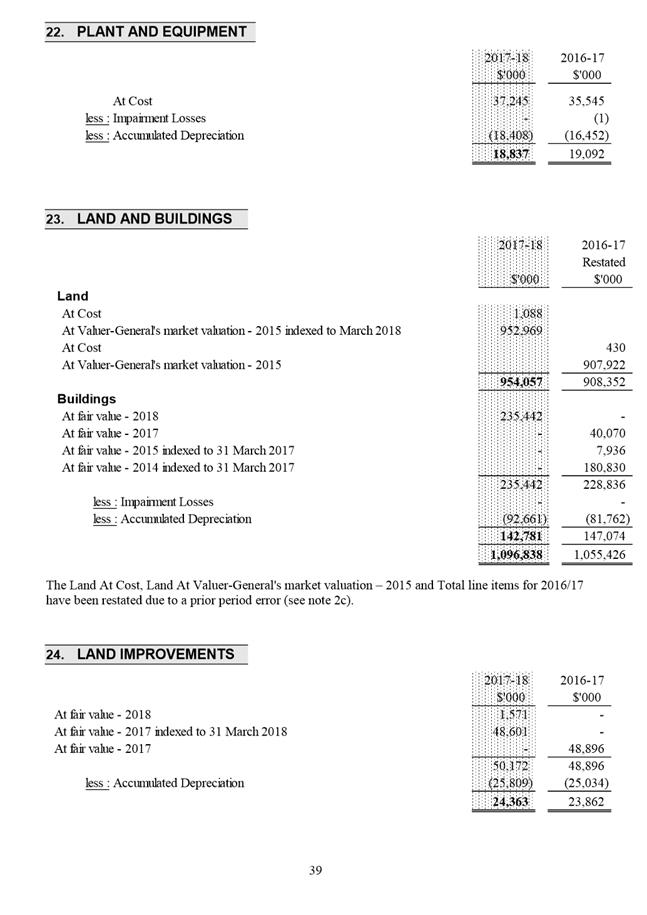

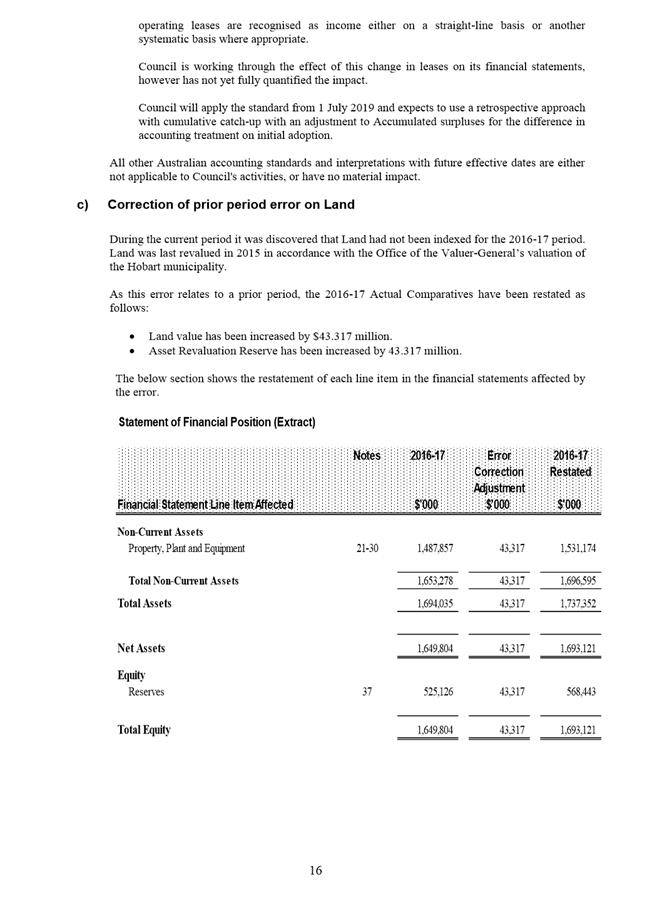

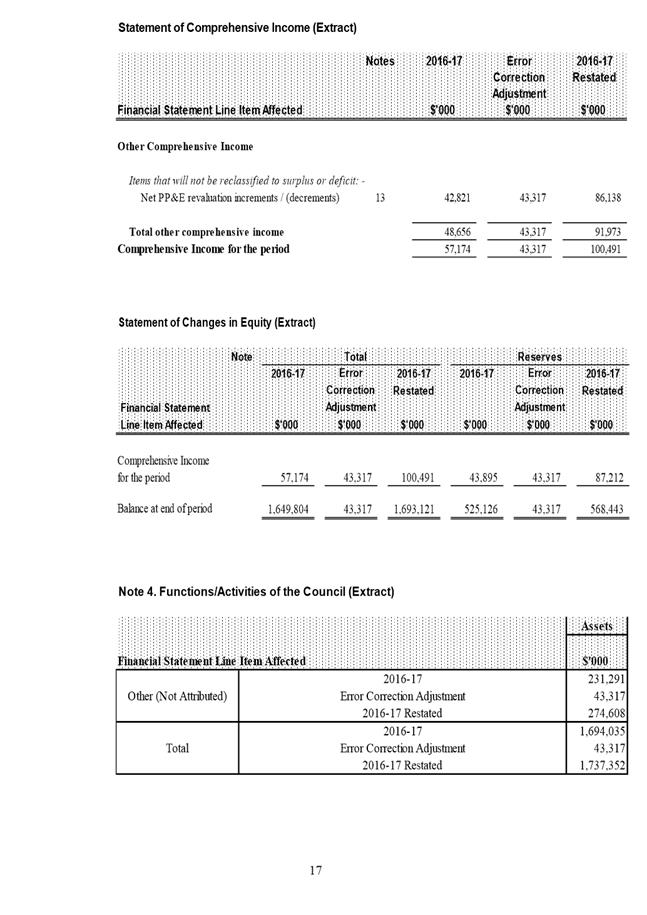

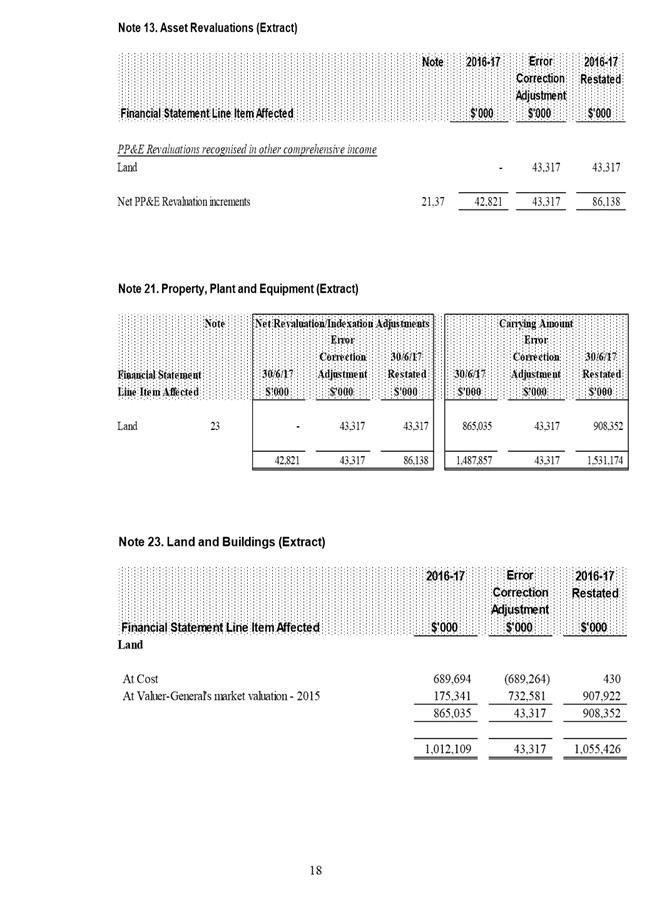

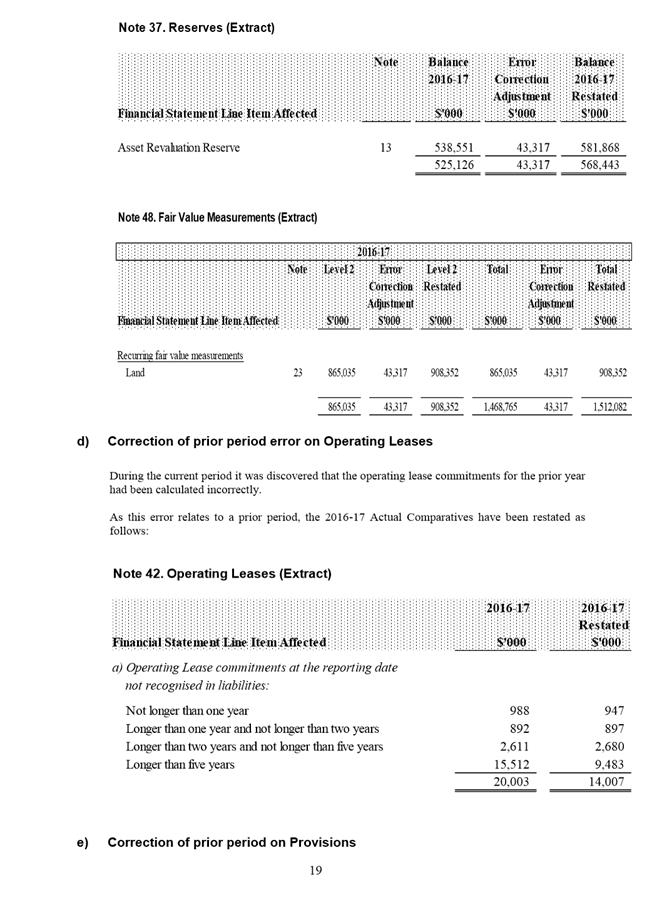

4.4.1. Update land indexation values, including restating the 2016-17 comparatives. The Council applied land indexation as if the factors were for each individual year, however it was discovered that the factors were in fact cumulative for each year, resulting in indexation being taken at 15% rather than 10%. It was also concluded that as land indexation had not been applied in the prior year that the 2016-17 comparatives would also need to be adjusted. The end result was land being indexed by 5% in 2016-17 and 5% in 2017-18,

4.4.2. Take up indexation on land under roads. Indexation had been applied to land, however not to land under roads as it was deemed that they were held at cost. It was decided that land under roads should be indexed as well. As with the land, land under roads 2016-17 comparatives also needed to be adjusted,

4.4.3. Adjust Buildings not for replacement that were valued as zero. In the past any specialised assets that Council deemed it would not replace could be valued at zero. However under the new AASB 2016-4 Amendments to Australian Accounting Standards – Recoverable Amount of Non-Cash-Generating Specialised Assets of Not-for-Profit Entities, effective from 1 July 2017, any assets that are providing a benefit to the public or generating income must be valued,

4.4.4. Split the Provisions classification between current and non-current, which also involved changing the 2016-17 comparatives,

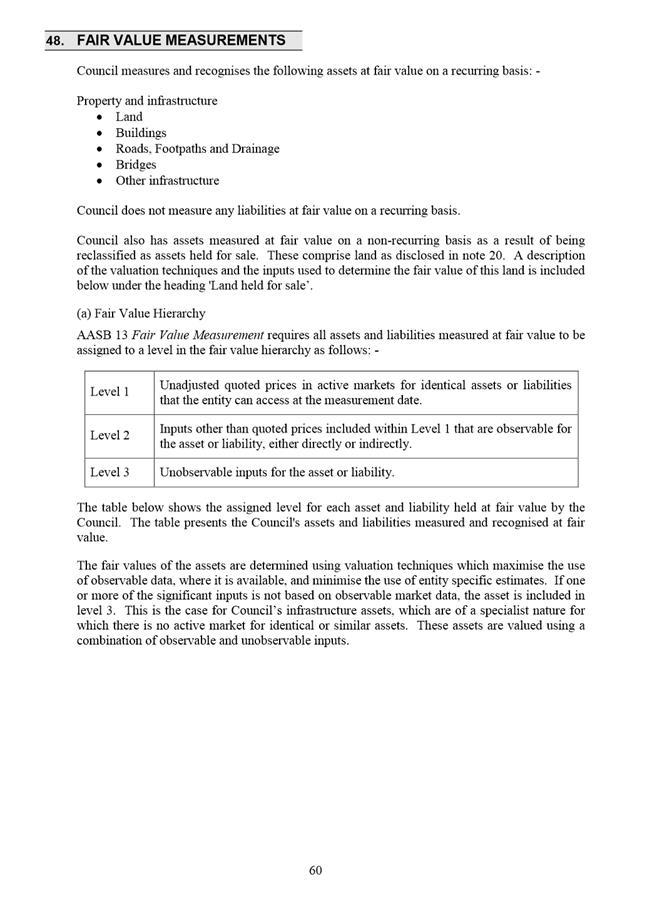

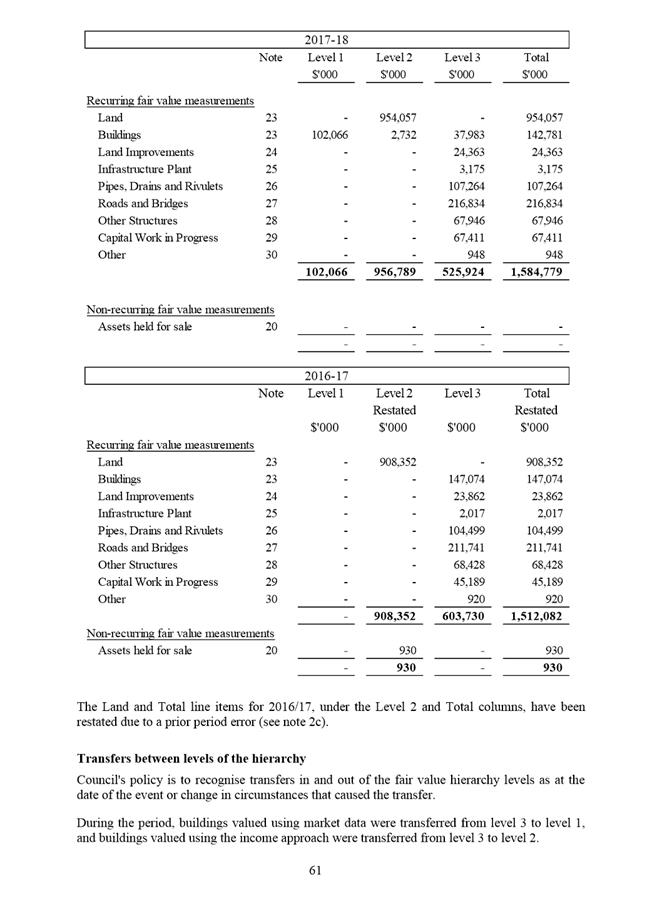

4.4.5. Update the classification of fair value on buildings between level 1, 2 and 3 in note 48. Buildings valued using our external valuer (Opteon) were valued using actual market data and these were classified as level 1. Buildings that were generating income were valued using the income approach and these were classified as level 2. All other buildings valued using current replacement cost were classified as level 3, and

4.4.6. Other minor disclosure and presentation changes.

4.5. The financial statements will be re-presented to the Risk and Audit Panel on 15 October 2018 for endorsement for formal adoption by Council.

4.6. The financial statements are attached to this report (see Attachment A). Highlights of the financial statements are detailed in Section 7 below.

5. Proposal and Implementation

5.1. It is proposed that Council formally adopt the financial statements.

6. Strategic Planning and Policy Considerations

6.1. There are no direct strategic planning implications.

7. Financial Implications

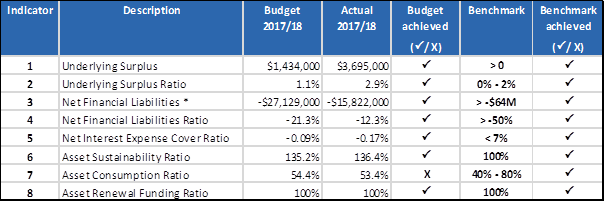

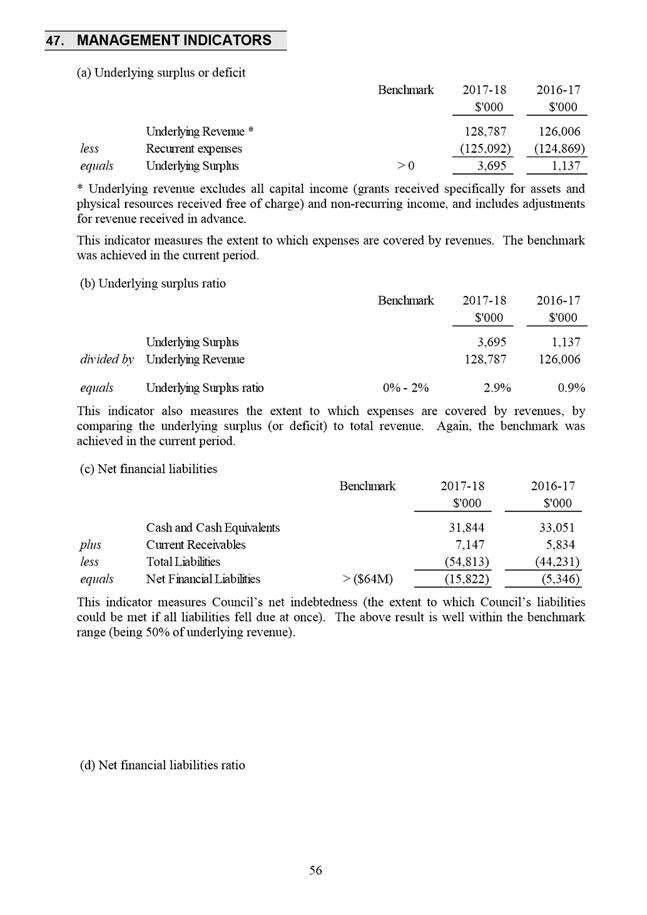

7.1. Financial Sustainability Outcomes

7.1.1. As outlined in Council’s Long-term Financial Management Plan (LTFMP), eight financial sustainability measures have been adopted for the purpose of measuring Council’s financial sustainability.

7.1.2. Indicators 1-2 are measures of profit and performance and the extent to which expenses are covered by revenues.

7.1.3. Indicators 3-4 are measures of indebtedness and the amount Council owes others (loans, employee provisions, creditors) net of financial assets (cash and amounts owed to Council).

7.1.4. Indicator 5 measures the proportion of income required to meet net interest costs.

7.1.5. Indicators 6-8 are measures of asset management.

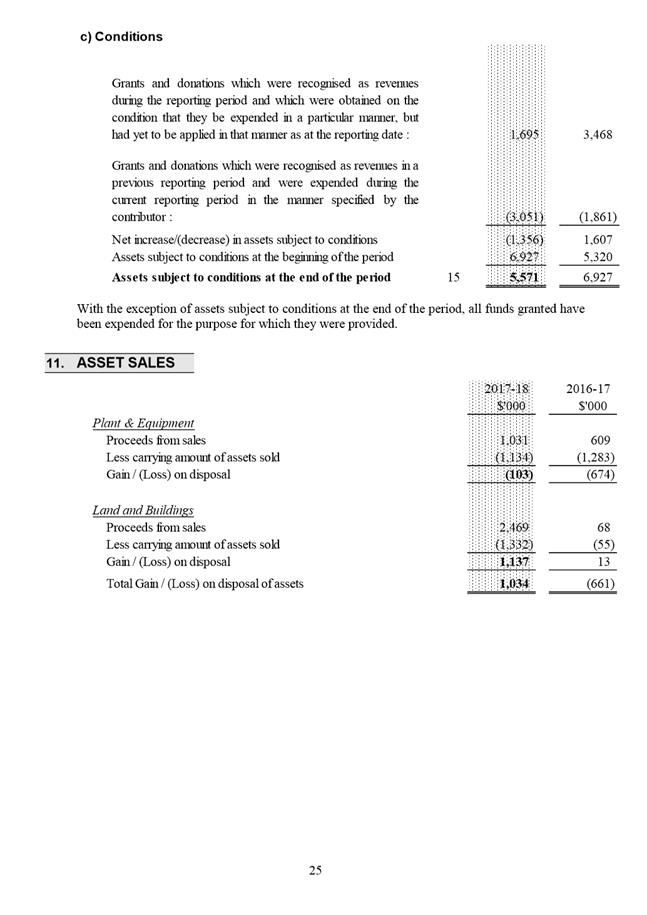

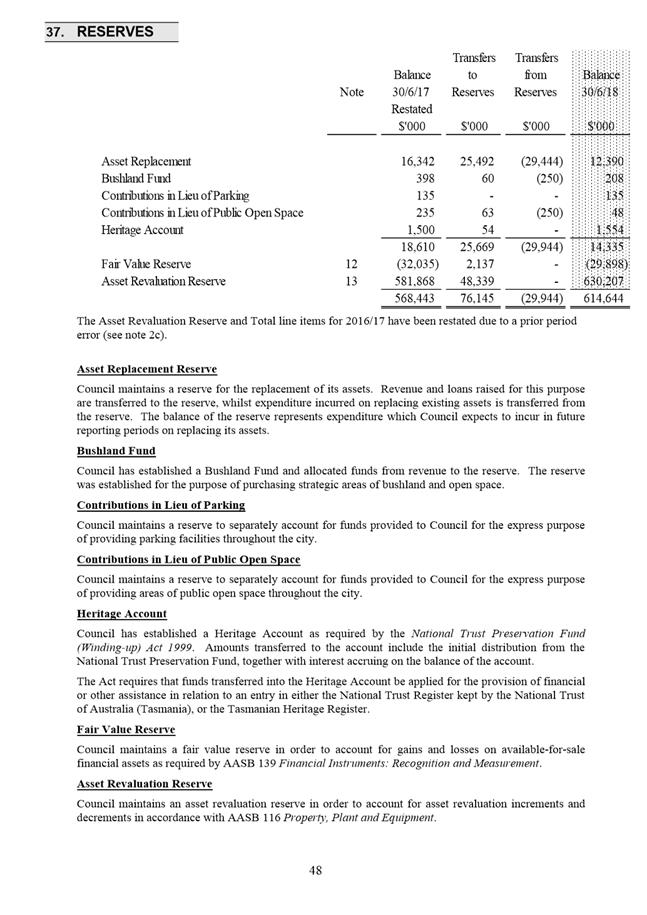

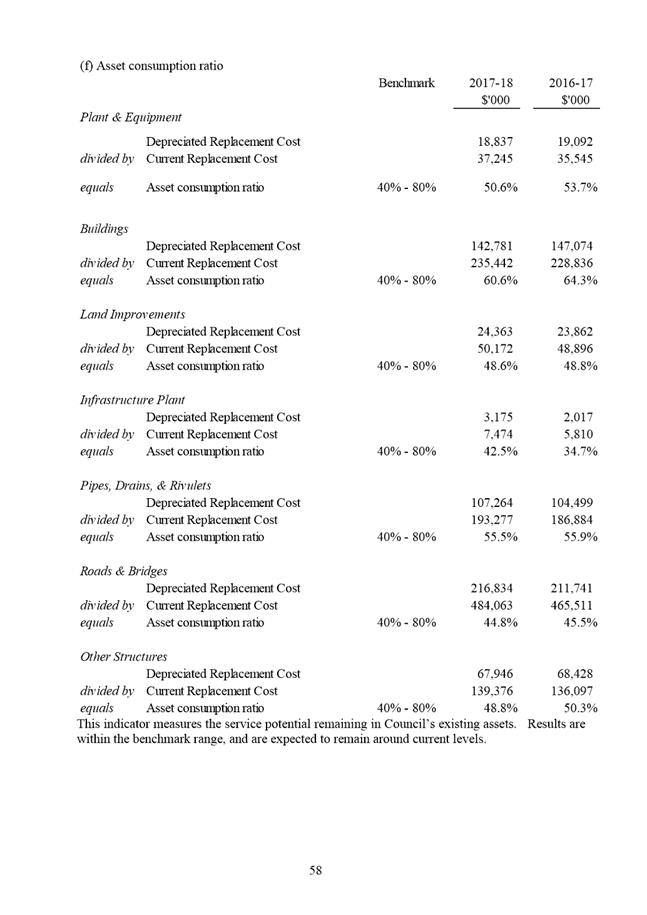

7.1.6. Council’s performance against the eight financial sustainability indicators is shown in Table 1 below: -

Table

1: Performance against Financial Sustainability Indicators

*Note - Net Financial Liabilities includes all liabilities, and therefore differs from the value shown in note 18 of the financial statements (which only includes financial liabilities).

7.1.7. The budget has not been achieved for indicator 7 as the revaluation of buildings (see 7.5 below) changed the consumption ratio of that class. However, the result is still well within the benchmark range.

7.2. Operating Result

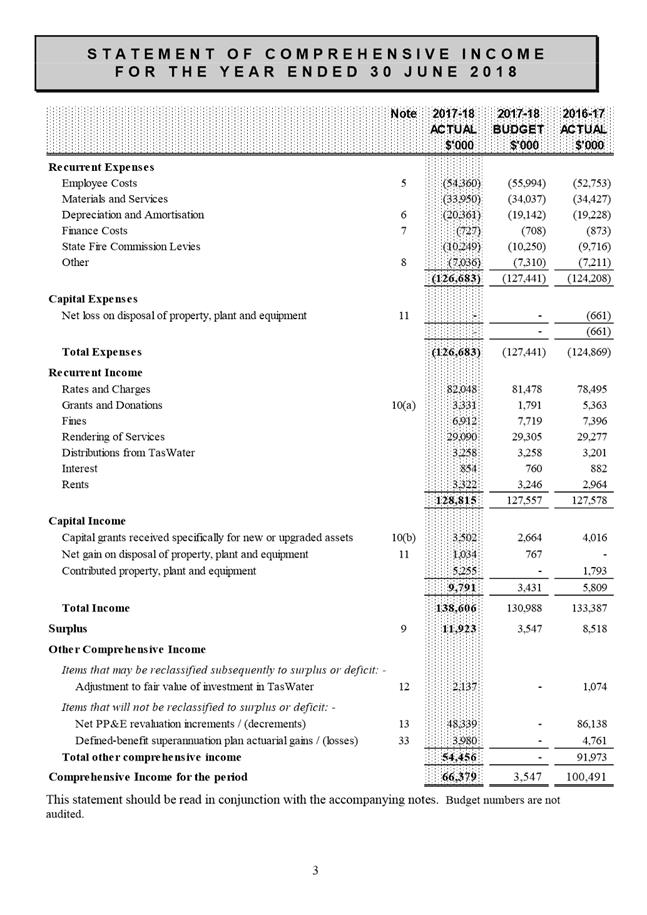

7.2.1. The Operating Result for 2017-18 is a surplus of $11.923 million (2016-17 $8.518 million). This result includes capital grants, contributed infrastructure assets, property sales, expenses incurred as a direct result of the May ’18 significant weather event, and the advance receipt of financial assistance grants and rates.

7.2.2. Excluding these items produces an underlying surplus of $3.695 million (2016-17 $1.137 million), or 2.9% of underlying revenue. This result is $2.26 million favourable against the original budget position ($1.43 million surplus) and $2.04 million favourable against the most recent forecast ($1.65 million surplus). Council seeks to record modest annual surpluses.

7.2.3. The $2.26 million favourable variance against the original budget position is mainly due to favourable variances in employee costs, grants (half of the 2018-19 Financial Assistance Grants were brought forward and paid in 2017-18) and rate revenue. Unfavourable variances were recorded for external labour costs, fines income, depreciation expense and materials and services.

7.2.4. The Auditor-General last year issued guidelines for calculating the underlying result, and these guidelines have been followed in calculating the above number.

7.2.5. At its meeting on 21 September 2015 Council resolved that annually, as part of the review of the September quarter financial report, the Council consider the prior year’s operating result – it’s size and what, if anything, to allocate it to. Therefore, further information on the 2017-18 operating surplus in excess of budget will be provided as part of the September quarter financial report.

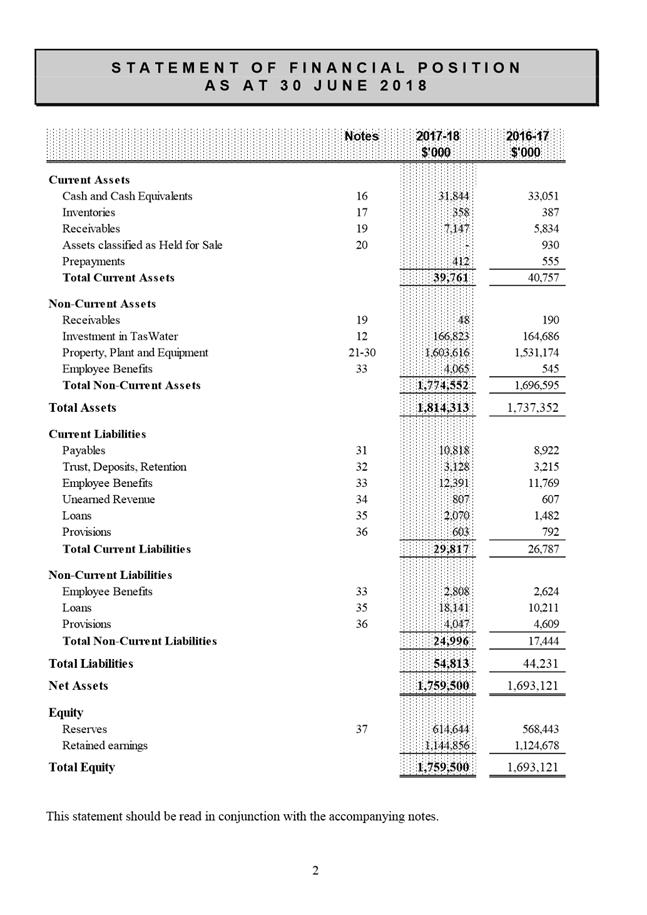

7.3. Cash Position

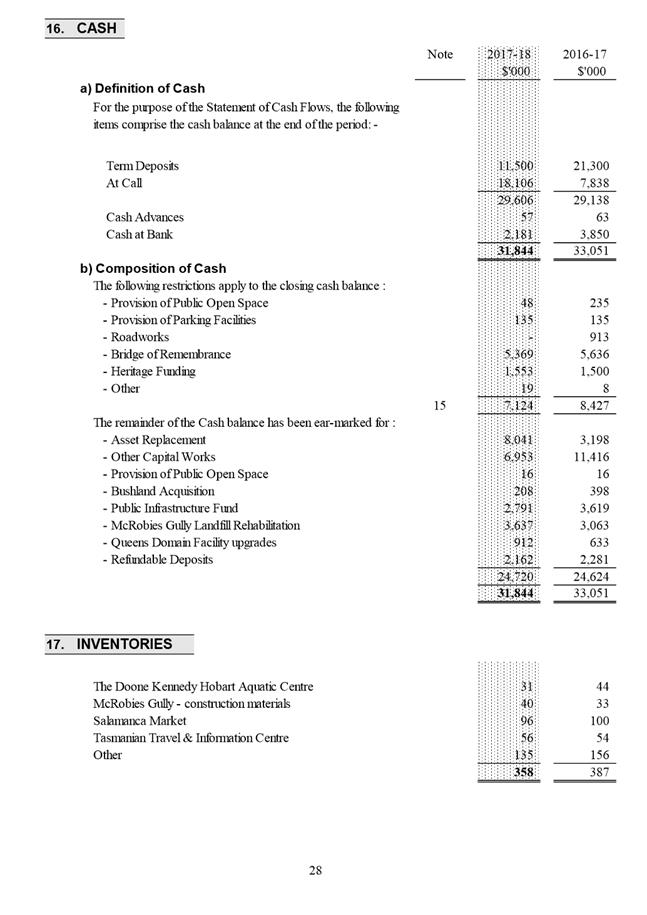

7.3.1. Cash balances have decreased by $1.21 million from $33.05 million to $31.84 million. This amount is allocated to the various purposes listed in note 16 to the financial statements. Note 16 demonstrates that the cash on hand is not “unutilised funds”. In fact, all funds are accounted for in some way. Some funds are restricted (e.g. the Heritage Account and unspent grants) and remaining funds are earmarked for various purposes (e.g. carry-forward capital works).

7.3.2. The decrease in cash is primarily due to increasing levels of capital expenditure, together with various timing issues that contribute to the cash balance at any given point in time. The decrease in cash would have been higher had it not been for the early receipt of 2018-19 financial assistance grants and a $10 million borrowing. The 2017-18 budget was premised on $15 million of new borrowings. Actual and projected cash flows were monitored toward the end of the year and it was determined that $10 million was appropriate.

7.4. Rate revenue

7.4.1. Rate revenue totalled $82.05 million (2016-17 $78.5 million) and continues to represent approximately 64% of underlying revenue.

7.4.2. The increase of $3.55 million (4.52%) is the result of:

· A 3.25% increase to fund the increased cost of providing existing services,

· A 0.67% increase to fund the increase in the State Government fire levy, and

· A 0.6% increase in Council’s rate base (total AAV) due to development activity.

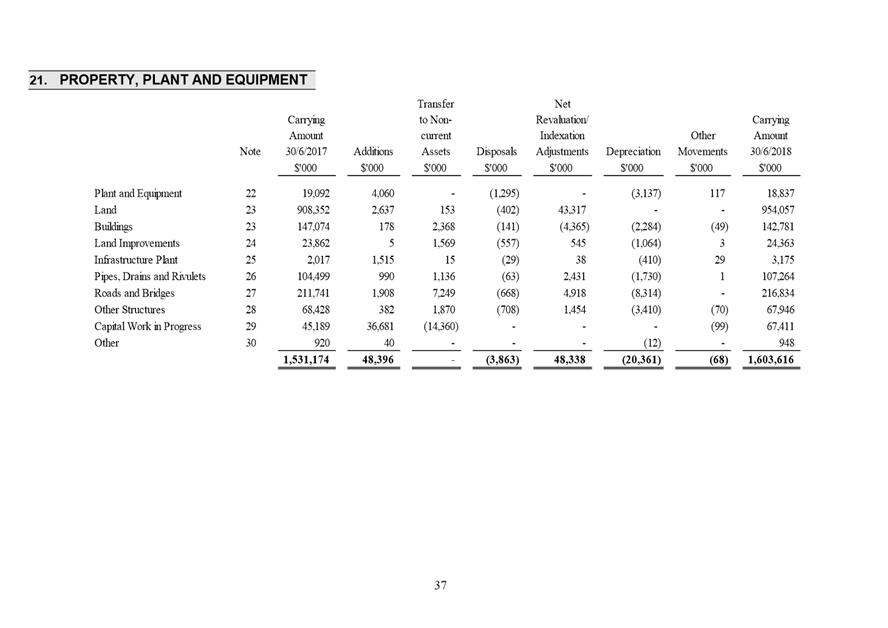

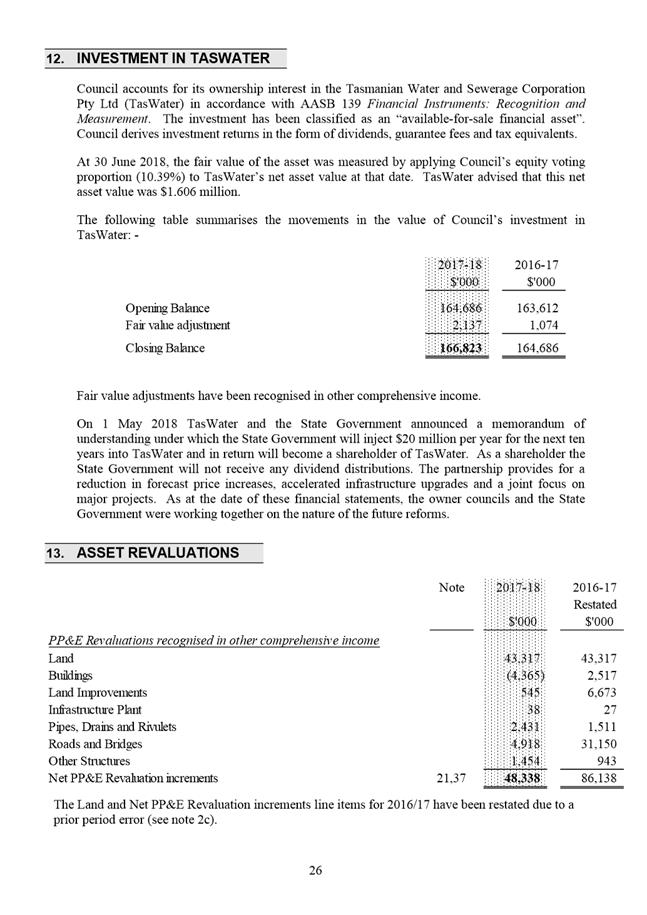

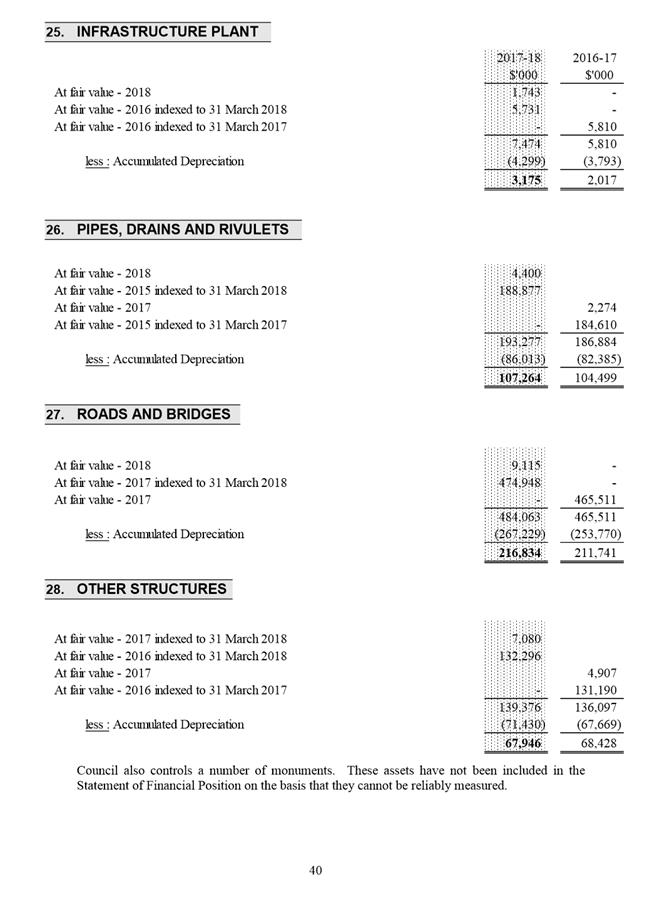

7.5. Asset Revaluations

7.5.1. In accordance with the requirement to ensure that reported asset values do not differ materially from their fair value, some asset classes were revalued during 2017-18, and indexation was applied to others.

7.5.2. The results of the revaluation exercise were:

|

Buildings |

$4.365M |

Decrement |

7.5.3. The results of the indexation exercise were:

|

Land |

$43.317M |

Increment |

|

Land Improvements |

$0.545M |

Increment |

|

Infrastructure Plant |

$0.038M |

Increment |

|

Pipes, Drains and Rivulets |

$2.431M |

Increment |

|

Roads and Bridges |

$4.918M |

Increment |

|

Other Structures |

$1.454M |

Increment |

|

|

$48.338M |

Increment |

7.5.4. The buildings revaluation was undertaken using the same methodology that was used previously. An external valuer was employed to provide market values for those buildings where observable market based valuations could be obtained e.g. Council Centre, car parks, Criterion and Mathers House, and unit replacement rates, on a building type basis, for remaining buildings. This is consistent with the requirements of AASB 116 Property Plant and Equipment and AASB 13 Fair Value Measurement.

7.5.5. The above revaluation increments and decrements have been recognised in “other comprehensive income” rather than in the surplus.

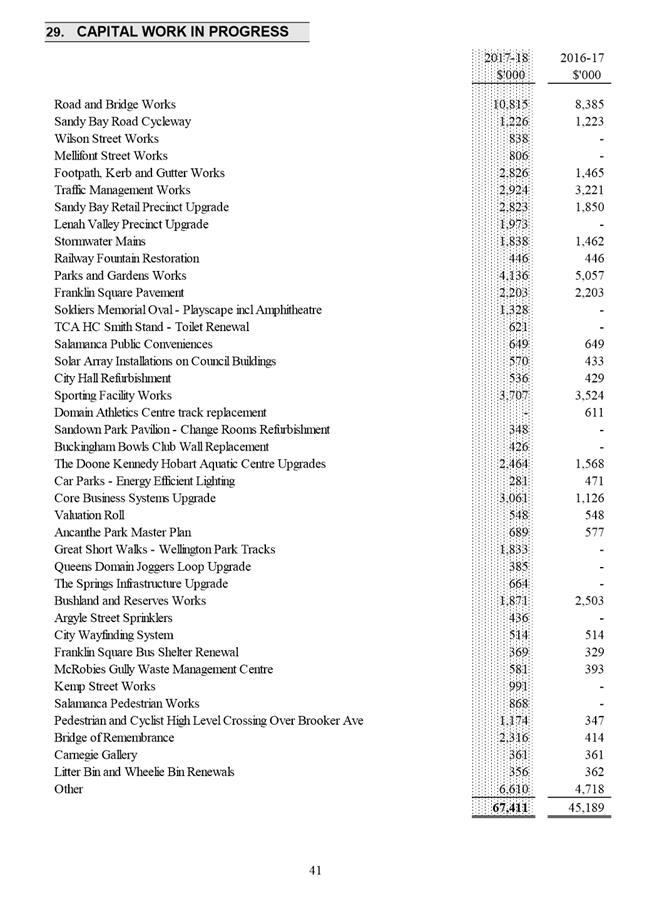

7.6. Contributed Property, Plant and Equipment

7.6.1. Contributed property, plant and equipment essentially comprises assets required to be constructed for Council by developers.

7.6.2. During 2017-18, these amounted to $5.255 million (2016-17 $1.793 million) and were mainly derived from the Garrington Park subdivision located at 110 Giblin Street, and the Tolmans Hill Estate.

7.7. Asset Write-offs

7.7.1. Asset write-offs are mainly comprised of infrastructure assets replaced as part of Council’s on-going asset renewal program.

7.7.2. Asset write-offs totalled $2.299 million (2016-17 $2.315 million) and were in respect of the following asset classes :

|

Land Improvements |

$0.557M |

|

Other Structures |

$0.708M |

|

Roads and Bridges |

$0.668M |

|

Other |

$0.366M |

|

|

$2.299M |

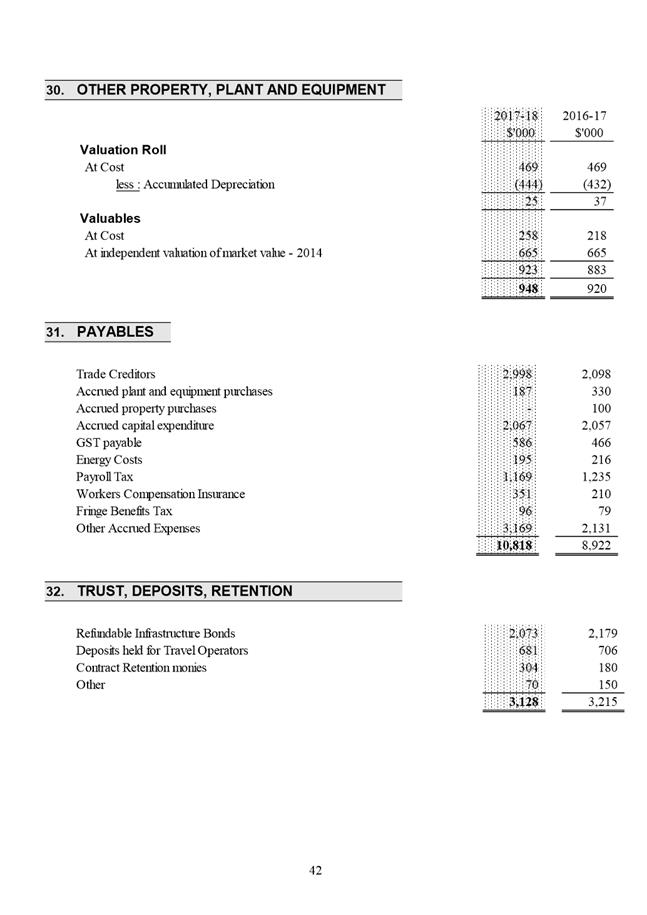

7.8. Investment in TasWater

7.8.1. Council has an ownership interest in TasWater, which is accounted for as an “available-for-sale financial asset”.

7.8.2. Distributions received from TasWater (including dividends) are recognised as revenue and included in Council’s surplus.

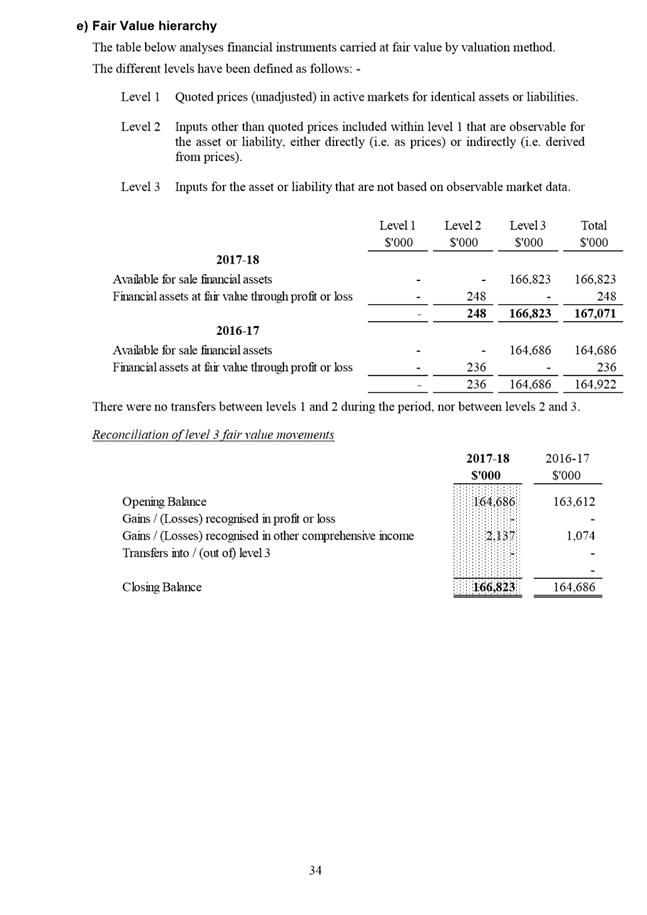

7.8.3. The value of Council’s ownership interest at any point in time is calculated by applying Council’s ownership interest percentage (10.39%) to TasWater’s net asset value. Applying this methodology at 30 June 2018 produces a value for Council’s ownership interest of $166.823 million (30 June 2017 $164.686 million). The $2.137 million increase from the previous year has been recognised in “other comprehensive income” rather than in the surplus.

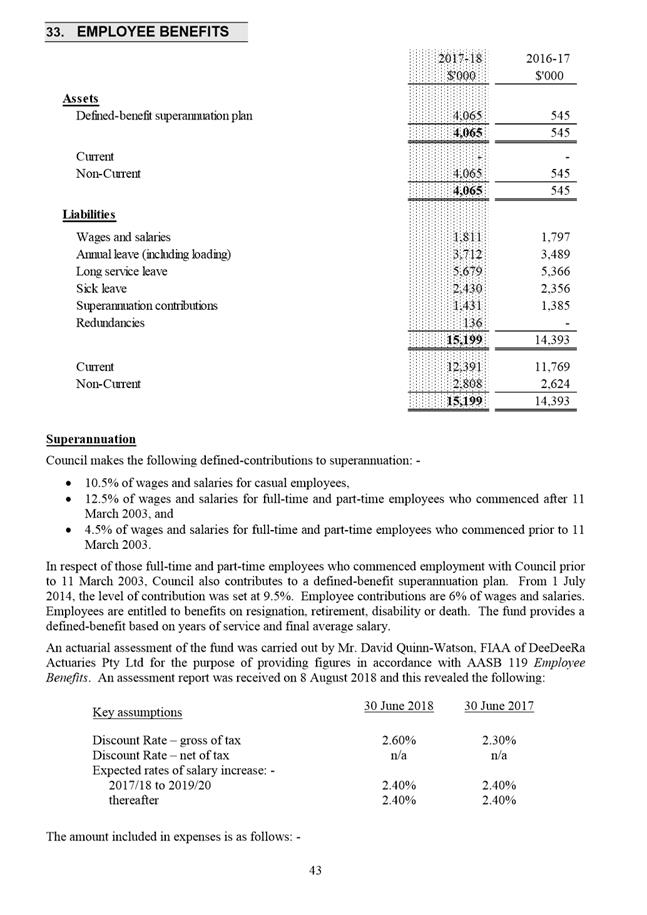

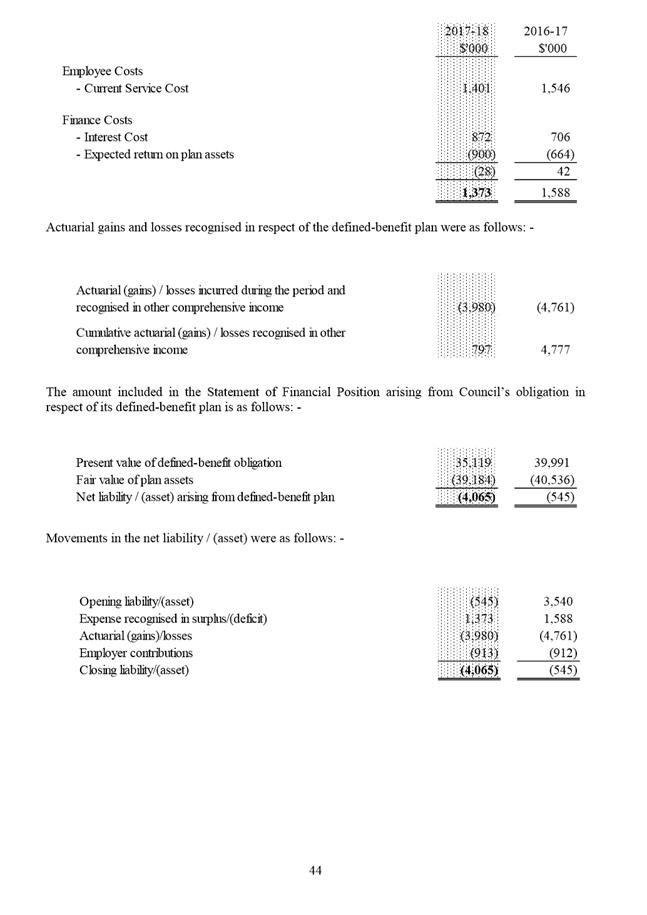

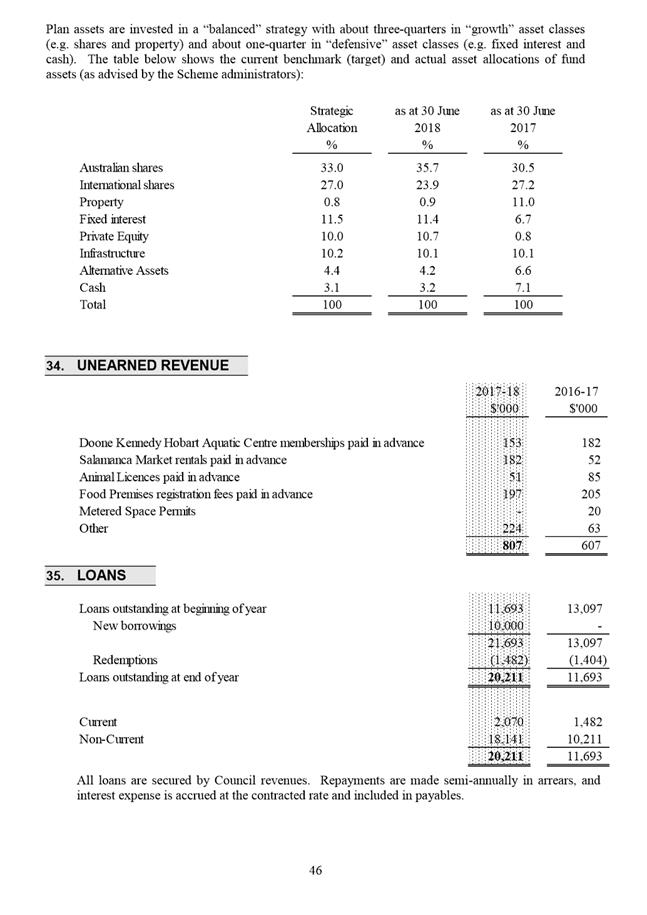

7.9. Defined-Benefit Superannuation Plan

7.9.1. Council’s defined-benefit superannuation plan net asset position has improved by $3.52 million to $4.065 million at 30 June 2018. This improvement is mainly due to: -

7.9.1.1. An increase in the discount rate (from 2.3% to 2.6%) which decreases the defined-benefit obligation, and

7.9.1.2. The significant returns achieved on plan assets during 2017-18 (about 7.9%).

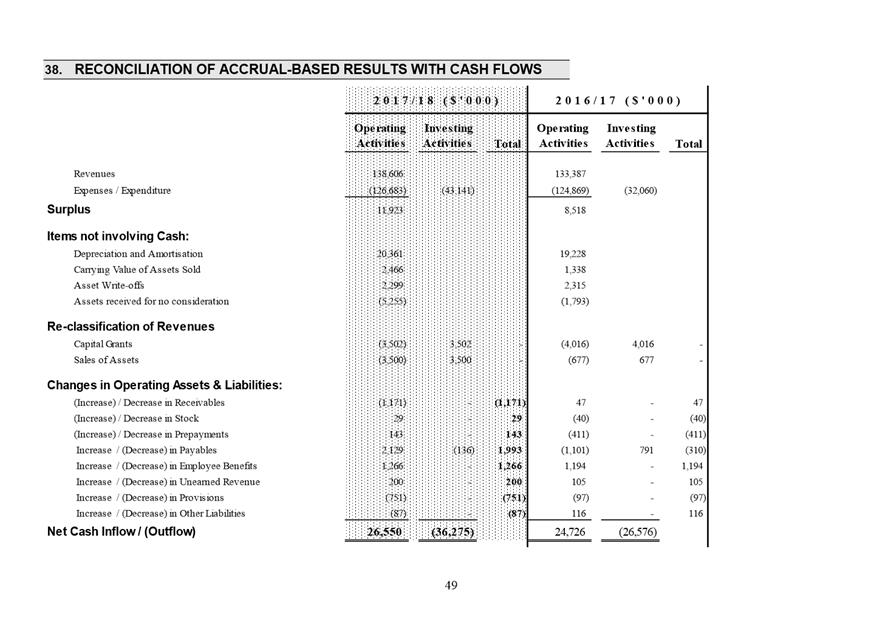

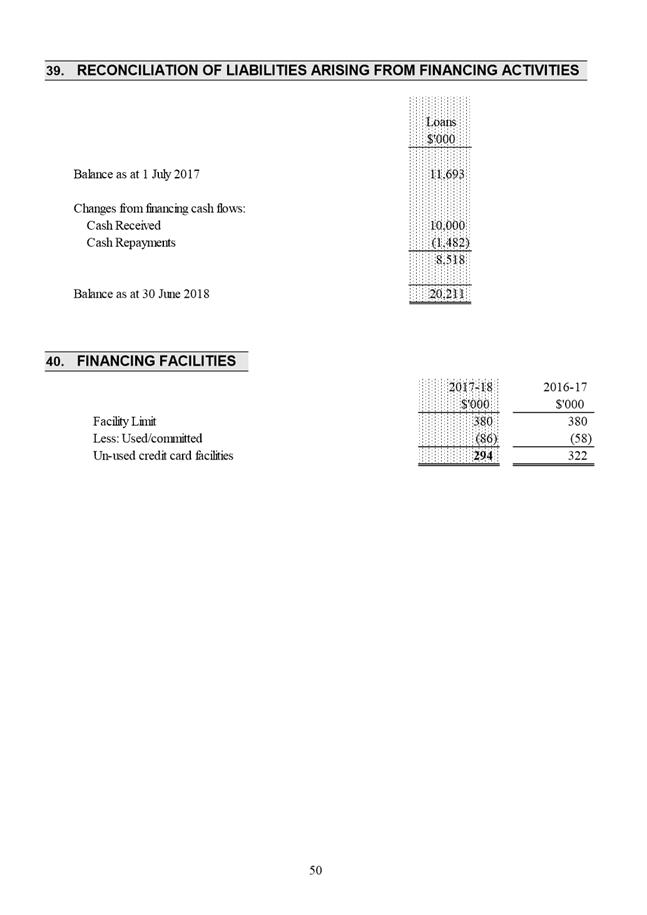

7.10. Reconciliation of Liabilities arising from Financing Activities

7.10.1. Council has adopted Accounting Standard AASB 2016-2 Amendments to Australian Accounting Standards – Disclosure Initiative: Amendments to AASB 107 in 2017-18.

7.10.2. Amendments to AASB 107 require additional disclosures to enable the reader to evaluate changes in liabilities arising from financing activities. These disclosures include both cash flows and non-cash changes between the opening and closing balance of the relevant liabilities.

7.10.3. The required disclosures are contained in note 39 to the financial statements.

8. Legal, Risk and Legislative Considerations

8.1. Section 84(1) of the Local Government Act 1993 requires the General Manager to prepare and forward to the Auditor-General a copy of Council’s financial statements in accordance with the Audit Act 2008.

8.2. Section 17(1) of the Audit Act 2008 requires the General Manager to prepare and forward a copy of Council’s financial statements to the Auditor-General within 45 days after the end of each financial year.

8.3. Section 17(4) of the Audit Act 2008 requires Council’s financial statements to be prepared in accordance with the accounting standards and other requirements issued by the Australian Accounting Standards Board.

8.4. Section 84(3) of the Local Government Act 1993 requires the General Manager to certify that the financial statements fairly represent Council’s financial position, the results of Council’s operations, and the cash flow of Council. This certification is attached (refer Attachment D).

8.5. Section 84(4) of the Local Government Act 1993 requires the General Manager to table the certified financial statements at a meeting of the Council as soon as practicable.

8.6. All of the above legal requirements have been complied with.

9. Delegation

9.1. This matter is delegated to the Council.

As signatory to this report, I certify that, pursuant to Section 55(1) of the Local Government Act 1993, I hold no interest, as referred to in Section 49 of the Local Government Act 1993, in matters contained in this report.

|

David Spinks Director Financial Services |

Michael Greatbatch Manager Finance |

Date: 11 October 2018

File Reference: F18/104506

Attachment a: Financial

Statements for year ended 30 June 2018 ⇩ ![]()

Attachment

b: Final

Management Letter dated 28 September 2018 ⇩ ![]()

Attachment

c: Independent

Audit Report dated 28 September 2018 ⇩ ![]()

Attachment

d: Certification

by General Manager dated 28 September 2018 ⇩ ![]()

|

Item No. 6.1 |

Agenda (Open Portion) Finance and Governance Committee Meeting - 16/10/2018 |

Page 17 ATTACHMENT a |

|

Item No. 6.1 |

Agenda (Open Portion) Finance and Governance Committee Meeting - 16/10/2018 |

Page 53 ATTACHMENT a |

|

Item No. 6.1 |

Agenda (Open Portion) Finance and Governance Committee Meeting - 16/10/2018 |

Page 56 ATTACHMENT a |

|

Item No. 6.1 |

Agenda (Open Portion) Finance and Governance Committee Meeting - 16/10/2018 |

Page 66 ATTACHMENT a |

|

Item No. 6.1 |

Agenda (Open Portion) Finance and Governance Committee Meeting - 16/10/2018 |

Page 67 ATTACHMENT a |

|

Item No. 6.1 |

Agenda (Open Portion) Finance and Governance Committee Meeting - 16/10/2018 |

Page 87 ATTACHMENT b |

|

Agenda (Open Portion) Finance and Governance Committee Meeting - 16/10/2018 |

Page 89 ATTACHMENT c |

|

Agenda (Open Portion) Finance and Governance Committee Meeting - 16/10/2018 |

Page 92 ATTACHMENT d |

|

Agenda (Open Portion) Finance and Governance Committee Meeting |

Page 93 |

|

|

|

16/10/2018 |

|

6.2 Occupancy Rates - Multi-Storey Car Parks

Memorandum of the Operations Manager - Car Parks, Group Manager Parking Operations and Director City Innovation and Technology of 2 October 2018 and attachments.

Delegation: Committee

|

Item No. 6.2 |

Agenda (Open Portion) Finance and Governance Committee Meeting |

Page 94 |

|

|

16/10/2018 |

|

Memorandum: Finance and Governance Committee

Occupancy Rates - Multi-Storey Car Parks

The following memorandum is provided in response to a request from the Finance and Corporate Services Committee on the 20 August 2013 (Open agenda, item 13 - Questions without Notice) to:-

“Please provide Aldermen with regular updates on the occupancy rates of the Council Multi-storey car parks?”

Accordingly, a quarterly memorandum is now provided to the Finance and Governance Committee providing occupation rates, occupation percentages and financials for the three short term multi storey car parks along with a quarterly overview of the Trafalgar permit holders and early bird car park.

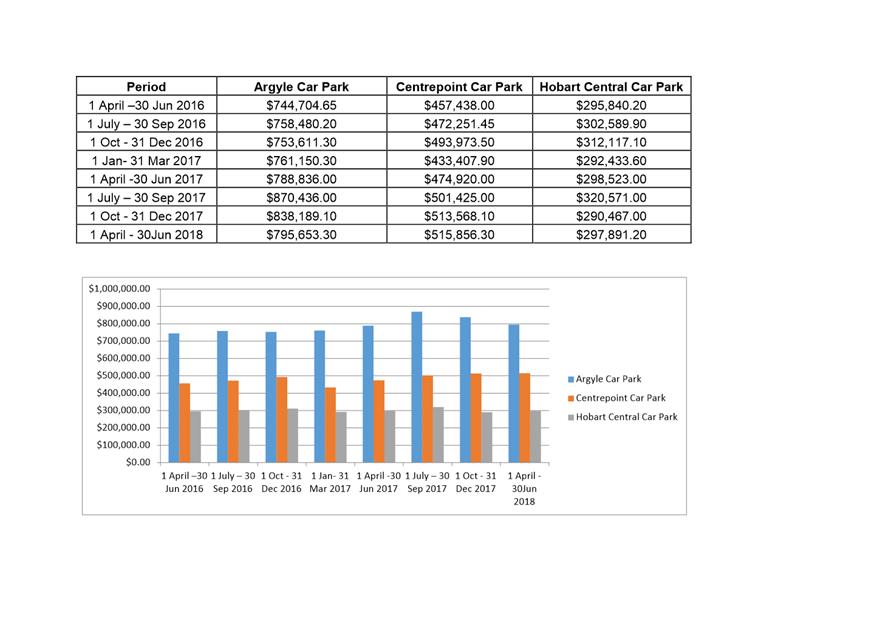

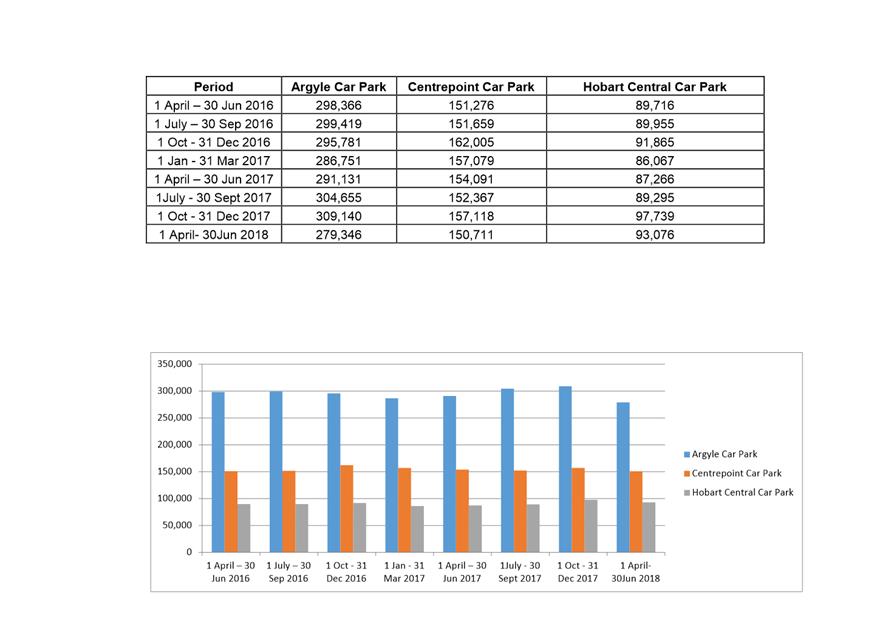

This memorandum provides figures for Quarter four (April - June) of the 2017-18 financial year and contains the following:

· The occupancy rates and income of each of the three multi-storey car parks for the quarter ending June 2018, and a comparison with the same period in 2017 (refer Table 1).

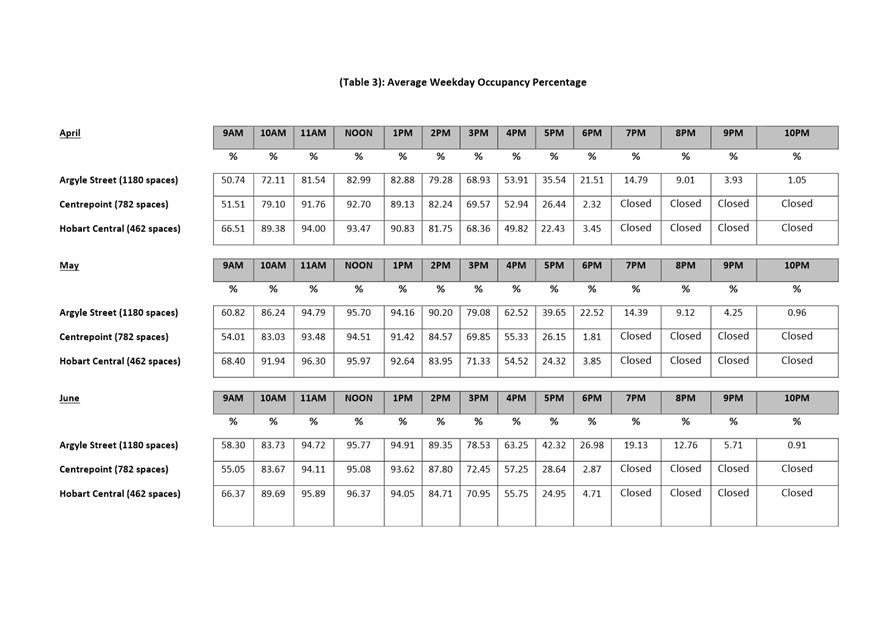

· Weekday hourly occupation percentages for each of the three multi-storey car parks for the same period (refer Attachment A).

· A three month overview of the occupancy rates and income generated by the Trafalgar Car Park through permit and early bird parking (refer Table 2).

Summary of results

The overall result across the car parks is as follows:

· 0.09% decrease in vehicle usage in multi-story car parks;

· 3.01% increase in income in multi-story car parks; and

· Trafalgar Car Park continues to perform well, being slightly ahead of budget.

table 1

|

2017 |

ARGYLE STREET |

CENTREPOINT |

HOBART CENTRAL |

||||

|

|

Cars |

Income |

Cars |

Income |

Cars |

Income |

|

|

April |

87653 |

$223,357.00 |

40391 |

$132,080.60 |

26214 |

$81,438.60 |

|

|

May |

103203 |

$288,974.00 |

55283 |

$180,775.80 |

31590 |

$114,291.80 |

|

|

June |

100275 |

$276,532.80 |

49561 |

$162,065.80 |

29462 |

$102,794.40 |

|

|

Totals |

291131 |

$788,863.80 |

145235 |

$474,922.20 |

87266 |

$298,524.80 |

|

|

|

|||||||

|

2018 |

ARGYLE STREET |

CENTREPOINT |

HOBART CENTRAL |

||||

|

|

Cars |

Income |

Cars |

Income |

Cars |

Income |

|

|

April |

84785 |

$229,165.20 |

46262 |

$154,506.00 |

29111 |

$88,096.00 |

|

|

May |

100256 |

$292,299.10 |

53212 |

$184,811.30 |

33303 |

$111,292.20 |

|

|

June |

94305 |

$274,189.00 |

51237 |

$176,539.00 |

30662 |

$98,593.00 |

|

|

Totals |

279346 |

$795,653.30 |

150711 |

$515,856.30 |

93076 |

$297,981.20 |

|

|

ARGYLE STREET |

CENTREPOINT |

HOBART CENTRAL |

|||||

|

Car park increase/decrease |

-11,785 |

$6,789.50 |

5,476 |

$40,934.10 |

5,810 |

-$543.60 |

|

|

-4.04% |

0.86% |

3.77% |

8.61% |

6.65% |

-0.18 |

||

|

Overall increase/decrease |

Cars |

-499 |

|||||

|

Income |

$47,180.00 |

||||||

· The decrease in Hobart Central revenue was due to the reduction in the number of early bird spaces allocated during the busy periods. Early bird parking provides the optimal revenue opportunity in car parks. The resulting increase in short term spaces provides increased capacity for shoppers’ vehicles and greater turnover of those vehicles, hence the increased car numbers.

· Income increased at the Argyle Street Car Park, which reflects the fee increase from the previous year and the introduction of a limited number of permit parking spaces. Vehicle numbers were generally down over the three month period mainly due to the queuing issues experienced in the car park during the school holiday period. As a result a number of patrons opted to use Hobart Central and Centrepoint car parks, as can be seen by the increased vehicle patronage in both car parks.

· Vehicle numbers and Income both increased in the Centrepoint Car Park as a result of a steady flow of patrons using the car park instead of Argyle Street. The status quo in the provision of early bird parking spaces was able to be maintained during the three month period which provided for an increase in income.

Trafalgar Car Park

Parking Operations assumed operational responsibility of the 544 parking spaces in the Trafalgar Car Park on 1 July 2013. As at that date, 388 spaces were leased to permit holders who now pay a monthly rental of either $268 or $288 depending on the conditions of their permit.

The goal is to fully occupy the car park with monthly tenants however, in the interim the void between actual and full occupancy is being filled with early bird parkers.

As at 30 June 2018, the number of spaces leased to permit holders was 486, with 58 vacant spaces being utilised for early bird parking. Saturday income is steadily increasing due to an increase in Salamanca Market patrons taking advantage of the $6 all day parking fee. As at 30 June 2018, the budget for the Trafalgar Car Park showed a favourable balance.

The income for the period 1 April 2018 – 30 June 2018 was split as follows:

Table 2

|

|

Apr-18 |

May-18 |

June-18 |

Total Income |

Budgeted Income |

|

Permits |

$113,597 |

$112,594 |

$114,600 |

$340,791 |

$324,378 |

|

Early Bird |

$15,160 |

$19,050 |

$15,149 |

$49,359 |

$56,000 |

|

Saturday |

$3,648 |

$2,996 |

$3,994 |

$10,638 |

$10,000 |

|

Total |

$132,405 |

$134,640 |

$133,743 |

$400,788 |

$390,378 |

Car Park Occupancy Percentages April – June 2018 (Refer Attachment A)

During April, Centrepoint Car Park recorded average occupation rates of 88.95% during the peak period of the day (11am – 2pm). Argyle Street averaged 81.67%, and Hobart Central averaged 90.01 % for the same period.

In the following two month period (1 May – 30 June 2018) occupancy rates in all three car parks at the peak period of the day were higher – averaging at or above 92.66 %.

Hobart Central and Centrepoint car parks both accept “early bird” parking. During quieter periods the car park operators manually adjust the number of early birds they accept based on the vehicle usage statistics. The higher percentages of occupation in both of these car parks are reflective of this.

During the three month period vehicular traffic in Argyle Street Car Park decreased, mainly due to queuing issues which saw patrons utilise alternative car parks. This resulted in the car park not quite filling during the three month period. The average number of vacant spaces available during the peak period of the day was 111.

Centrepoint and Hobart Central car parks both had busy periods during April, May and June with both car parks filled but only momentarily. Accordingly, early birds were adjusted in Hobart Central, however Centrepoint remained unchanged.

The usage statistics demonstrate that during the period of 11am – 2pm of a weekday there is a rising peak occupancy demand. Now that the new 102 space Melville Street Car Park is operating, Parking Operations will concentrate on promoting its use as a means of addressing the increase in demand.

|

That the information contained in the memorandum of the Operations Manager – Car Parks, the Group Manager Parking Operations and the Director City Innovation and Technology of 28 September 2018 titled “Occupancy Rates – Multi-Storey Car Parks” be received and noted.

|

As signatory to this report, I certify that, pursuant to Section 55(1) of the Local Government Act 1993, I hold no interest, as referred to in Section 49 of the Local Government Act 1993, in matters contained in this report.

|

David Fox Operations Manager - Car Parks |

Matthew Tyrrell Group Manager Parking Operations |

|

Peter Carr Director City Innovation and Technology |

|

Date: 2 October 2018

File Reference: F18/111362

Attachment a: Graph

1 Revenue ⇩ ![]()

Attachment

b: Graph

2 Vehicle Usage ⇩ ![]()

Attachment

c: Table

3 Percentages ⇩ ![]()

|

Item No. 6.2 |

Agenda (Open Portion) Finance and Governance Committee Meeting - 16/10/2018 |

Page 98 ATTACHMENT a |

|

Agenda (Open Portion) Finance and Governance Committee Meeting - 16/10/2018 |

Page 100 ATTACHMENT b |

|

Agenda (Open Portion) Finance and Governance Committee Meeting - 16/10/2018 |

Page 102 ATTACHMENT c |

|

Agenda (Open Portion) Finance and Governance Committee Meeting |

Page 103 |

|

|

|

16/10/2018 |

|

6.3 Council Committees - Quorums

Report of the Group Manager City Government and Customer Relations and Deputy general Manager of 11 October 2018.

Delegation: Committee

|

Item No. 6.3 |

Agenda (Open Portion) Finance and Governance Committee Meeting |

Page 104 |

|

|

16/10/2018 |

|

REPORT TITLE: Council Committees - Quorums

REPORT PROVIDED BY: Group Manager City Government and Customer Relations

Deputy General Manager

1. Report Purpose and Community Benefit

1.1. The purpose of this report is to respond to a Council resolution to investigate the establishment of a procedure to provide voting rights to Aldermen who are not appointed as members of a council committee, on those occasions where they may be in attendance at a committee meeting.

1.2. The efficient conduct of meetings of the Council and the committees which it has established to assist in dealing with the business of the City engenders community confidence in the professionalism of the organisation.

1.3. The City’s Mission Statement is to ensure good governance of our Capital City.

2. Report Summary/Background

2.1. The Council, at its meeting held on 24 July 2017 resolved in the following terms:

The implementation of a procedure whereby each Council committee is retained at five members, but any Aldermen who may attend a committee meeting would also have voting rights, be explored.

2.2. Council committees are established under Section 23 of the Local Government Act 1993 (the Act).

2.3. Committees established by the City have historically comprised five members, except for the combined Finance and Governance Committee, which as, an interim arrangement until the election, has seven members.

2.4. Meeting procedures are prescribed within the local Government (Meeting Procedures) Regulations 2015, (the Regulations) and establish that a quorum is required for committees to conduct business.

2.5. The use of committees with established membership and clear terms of reference to assist the Council deal with the flow of business, is an effective mechanism in managing the wide range of issues which the City deals with.

|

That the information be received and noted.

|

4. Proposal and Implementation

4.1. The Act provides the following framework for the establishment and membership of committees:

(1) A council may establish, on such terms as it thinks fit, council committees to assist it in carrying out its functions under this or any other Act.

(2) A council committee consists of councillors appointed by the council and any councillor who fills a vacancy for a meeting at the request of the council committee.

(3) A meeting of a council committee is to be conducted in accordance with prescribed procedures.

4.2. The Regulations establish that a quorum for council committees is the majority of members appointed by the Council, which is five members for all City of Hobart committees, other than the Finance and Governance Committee, which temporarily has seven members.

4.3. The legislation provides voting rights to committee members who are appointed by the Council, and in the absence of a committee member, to an Aldermen who may be invited to fill a casual vacancy.

4.4. Without changing the membership of committees to include all Aldermen, it is not possible to extend voting rights to an Alderman who has not been appointed to a committee by the Council.

4.5. The committee structure is robust and its establishment and operation provides consistency and clarity for the community generally, and particularly when our customers wish to consult with committee members regarding Council matters.

5. Strategic Planning and Policy Considerations

5.1. The mission of the City of Hobart is to ensure good governance of our capital city.

6. Financial Implications

6.1. Funding Source and Impact on Current Year Operating Result

6.1.1. No financial implications arise from this report.

7. Legal, Risk and Legislative Considerations

7.1. Legal considerations are addressed.

8. Delegation

8.1. Unless any action is proposed by the committee, the matter is delegated to the committee, as the information provided is to be received and noted.

As signatory to this report, I certify that, pursuant to Section 55(1) of the Local Government Act 1993, I hold no interest, as referred to in Section 49 of the Local Government Act 1993, in matters contained in this report.

|

Margaret Johns Group Manager City Government and Customer Relations |

Heather Salisbury Deputy General Manager |

Date: 11 October 2018

File Reference: F18/69140

|

Item No. 6.4 |

Agenda (Open Portion) Finance and Governance Committee Meeting |

Page 107 |

|

|

16/10/2018 |

|

6.4 Aldermanic Development and Support Policy - International Relations

Memorandum of the Deputy General Manager of 11 October 2018.

Delegation: Council

|

Item No. 6.4 |

Agenda (Open Portion) Finance and Governance Committee Meeting |

Page 108 |

|

|

16/10/2018 |

|

Memorandum: Finance and Governance Committee

Aldermanic Development and Support Policy - International Relations

At its meeting of 17 September 2018 the Council adopted a series of recommendations from the Finance and Governance Committee relating to the policy provisions for Aldermanic professional development.

In reviewing the policy, the committee also considered a number of other matters in relation to Aldermanic activities, including the travel arrangements for Aldermen participating in delegations to Council’s international relationship cities.

The current policy provision for international relationships allows for Aldermen to participate in two Council approved international relationship delegations during a four year term. It also allows for the Council to approve more than two trips, if deemed appropriate.

In considering this provision, the Committee made the following recommendation to the Council:

“In respect to international relationships, the number of delegations in which aldermen may participate within a term of office, be reduced from 2 to 1 and the current policy wording “(or more, if deemed appropriate by the Council)”, be deleted.”

The Council subsequently deferred the recommendation for further consideration by the committee, and accordingly the matter is submitted to the Committee for further discussion.

|

The matter is referred for the Committee’s consideration. |

As signatory to this report, I certify that, pursuant to Section 55(1) of the Local Government Act 1993, I hold no interest, as referred to in Section 49 of the Local Government Act 1993, in matters contained in this report.

|

Heather Salisbury Deputy General Manager |

|

Date: 11 October 2018

File Reference: F18/114622

|

Item No. 6.5 |

Agenda (Open Portion) Finance and Governance Committee Meeting |

Page 110 |

|

|

16/10/2018 |

|

6.5 Complaints Against the Principles of the Customer Service Charter 2017/18

Report of the Group Manager City Government and Customer Relations and Deputy General Manager of 11 October 2018 and attachment.

Delegation: Committee

|

Item No. 6.5 |

Agenda (Open Portion) Finance and Governance Committee Meeting |

Page 111 |

|

|

16/10/2018 |

|

REPORT TITLE: Complaints Against the Principles of the Customer Service Charter 2017/18

REPORT PROVIDED BY: Group Manager City Government and Customer Relations

Deputy General Manager

1. Report Purpose and Community Benefit

1.1. The purpose of this report is to provide a summary of the number and nature of complaints made against the principles of the City of Hobart’s Customer Service Charter, received by the Council during 2017/18.

1.2. The Council adopted its latest Customer Service Charter shown as Attachment A to this report, at its meeting on 21 May 2018.

1.3. The Charter outlines the City’s commitment to our customers.

2. Report Summary

2.1. Section 339F (5) of the Local Government Act 1993 requires the General Manager to provide the Council with a report at least once a year with the number and nature of complaints received.

2.2. A complaint is defined as an expression of dissatisfaction about an unreasonable delay in response to a request, the withdrawal or reduction of service provided by the City, or unsatisfactory employee behaviours.

2.3. By definition, a service request is an appeal for assistance which requires some form of action (e.g. fallen tree or pot hole in the road.)

2.4. During 2017/18, 26 complaints were received.

2.5. By comparison 24 complaints were received during 2016/17.

|

That: 1. The report be received and noted.

|

4. Background

4.1. In accordance with section 339F (5) of the Local Government Act 1993, the General Manager is required to provide the Council with a report at least once a year with the number and nature of complaints received.

4.2. The principles underpinning Council’s performance as stated in the Customer Service Charter are that we will act in the following manner:

· Respectfully

By providing courteous and friendly service, listening to your needs and valuing and considering the perspective and contribution of our diverse community.

· Responsively

By keeping you informed using your preferred method of contact.

· Resourcefully

By delivering a range of relevant and accessible services on your behalf and managing and maintaining facilities to ensure a high standard of presentation ad performance for your use and enjoyment.

4.3. Our contact standards are:

· We will answer your phone call promptly and where possible resolve general enquiries.

Where we need to take specific action, we will refer you to the relevant service area and let you know what we will do.

· We will reply to your correspondence including e-mails and advise you of our intended actions, within ten business days.

· We will answer your social media message within one business day and where some form of action is required by the City, we will inform you of the next steps.

4.4. During 2017/18 a total of 26 complaints were received.

4.5. Of the complaints received during 2017/18, eight related to Parking and Information Officer conduct. The balance related to driving behaviour, contact standards, procedural processes, delay in works, and employee and contractor behaviour.

4.6. All of the complaints have been resolved. In all cases an investigation was carried out by the respective manager with feedback provided to the complainant.

4.7. While generally consistent with statistics in previous years, no complaints are acceptable.

4.8. The introduction of the Council’s first whole of organisation customer request system will considerably assist in better managing customer request and direct complaints.

5. Proposal and Implementation

5.1. Section 339F (5) of the Local Government Act 1993, provides that the General Manager is required to provide the Council with a report at least once a year with the number and nature of complaints received

5.2. For 2017/18 there were 26 complaints made against the principles of the Customer Service Charter.

5.3. By comparison 24 complaints were received during 2016/17.

6. Strategic Planning and Policy Considerations

6.1. The Capital City Strategic Plan 2015-2025 includes the following objective.

6.1.1. Deliver best practice customer service across the organisation.

7. Legal, Risk and Legislative Considerations

7.1. In accordance with section 339F (5) of the Local Government Act 1993, the General Manager is required to provide the Council with a report at least once a year with the number and nature of complaints received.

8. Delegation

8.1. This matter is delegated to the Finance and Governance Committee

As signatory to this report, I certify that, pursuant to Section 55(1) of the Local Government Act 1993, I hold no interest, as referred to in Section 49 of the Local Government Act 1993, in matters contained in this report.

|

Margaret Johns Group Manager City Government and Customer Relations |

Heather Salisbury Deputy General Manager |

Date: 11 October 2018

File Reference: F17/5756; 11-15-9

Attachment a: Customer

Service Charter ⇩ ![]()

|

Item No. 6.5 |

Agenda (Open Portion) Finance and Governance Committee Meeting - 16/10/2018 |

Page 115 ATTACHMENT a |

|

Agenda (Open Portion) Finance and Governance Committee Meeting |

Page 120 |

|

|

|

16/10/2018 |

|

6.6 Hobart Town Hall Ballroom - Acoustics

Report of the Group Manager City Government and Customer Relations and Deputy General Manager of 11 October 2018 and attachments.

Delegation: Council

|

Item No. 6.6 |

Agenda (Open Portion) Finance and Governance Committee Meeting |

Page 121 |

|

|

16/10/2018 |

|

REPORT TITLE: Hobart Town Hall Ballroom - Acoustics

REPORT PROVIDED BY: Group Manager City Government and Customer Relations

Deputy General Manager

1. Report Purpose and Community Benefit

1.1. The purpose of this report is to address options for improving the acoustics within the Town Hall Ballroom.

1.2. The ballroom is a popular community facility which is used for a wide range of functions, each requiring differing performance standards from the space.

1.3. The Town Hall is an iconic heritage building within the City, featuring the ornate ballroom which is highly valued for its design and features, as well as its availability for use as a community space.

2. Report Background

2.1. As the result of community concerns regarding the poor acoustic quality of the ballroom for speaking engagements and some musical events, the Council requested that a report be prepared documenting the quality of acoustics for the space.

2.2. The report was to identify any deficit in audio and instrumental acoustic quality and make recommendations as to how improved levels of instrumental and speech intelligibility could be achieved, and what steps needed to be taken to achieve the desired outcomes.

2.3. A detailed acoustic assessment of the ballroom was conducted over a four-month period, during which time the consultant established the existing acoustic conditions of the room and created an acoustic model of the space, which formed the basis for simulations of various remedial options.

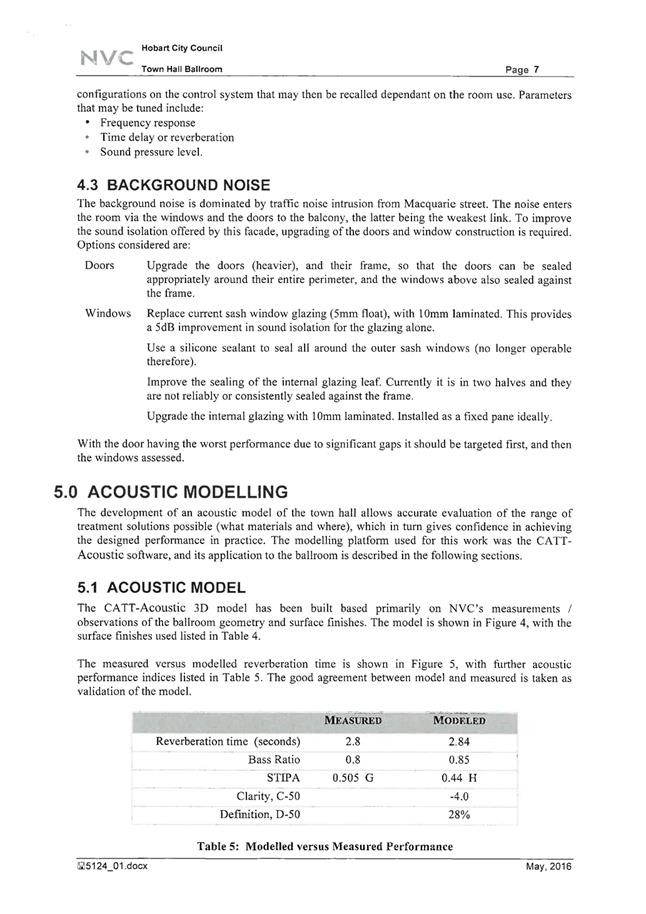

2.4. The findings were presented to the Finance Committee at its meeting of 14 November 2017, together with the report from the consultant engineers NVC (Noise Vibration Consulting). The report and consultants findings are attached to this report as Attachments A and B.

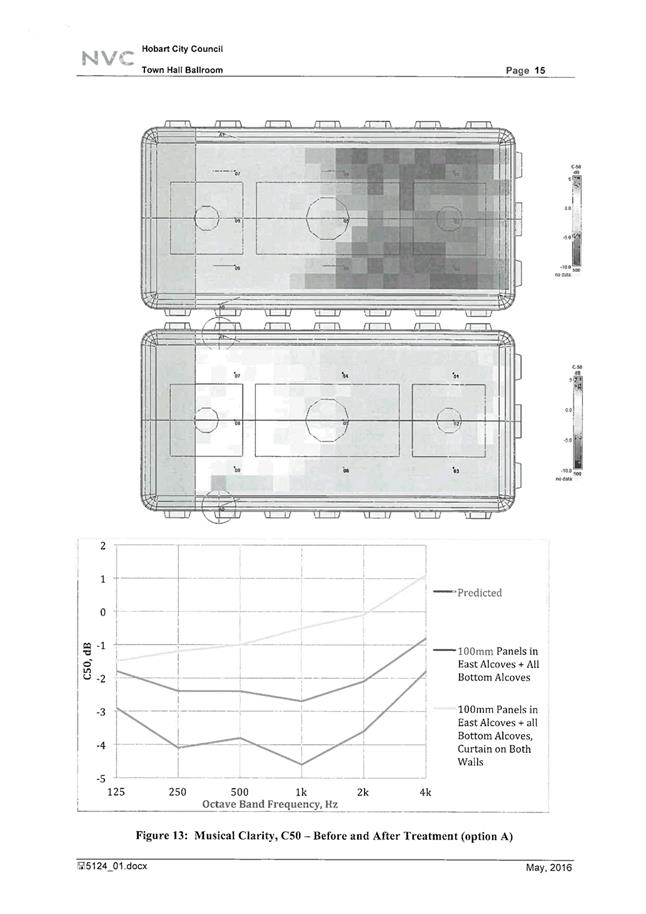

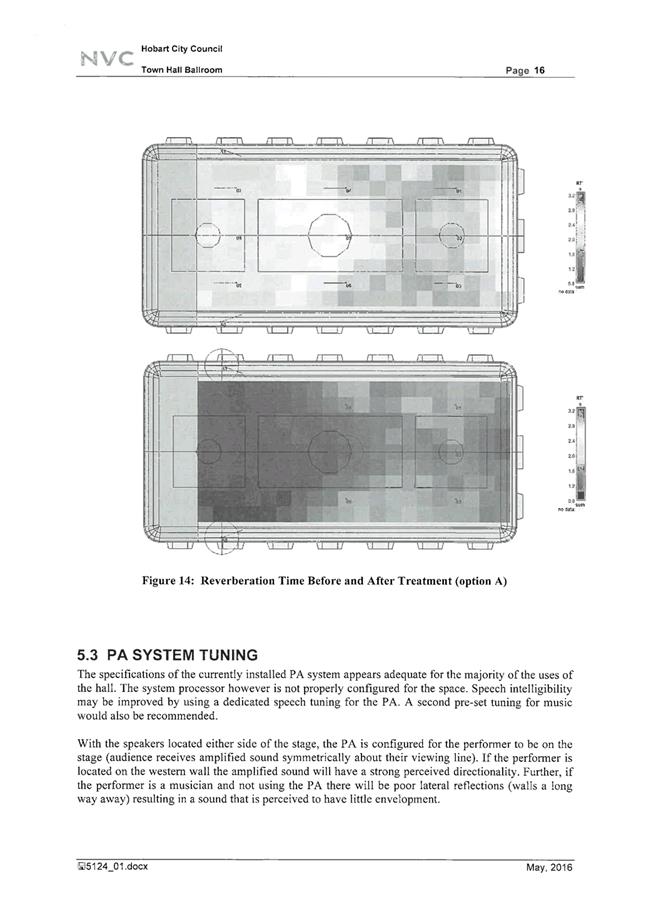

2.4.1. Notable aspects of the assessment include;

· The optimum suitability of the ballroom’s acoustics is for organ recitals;

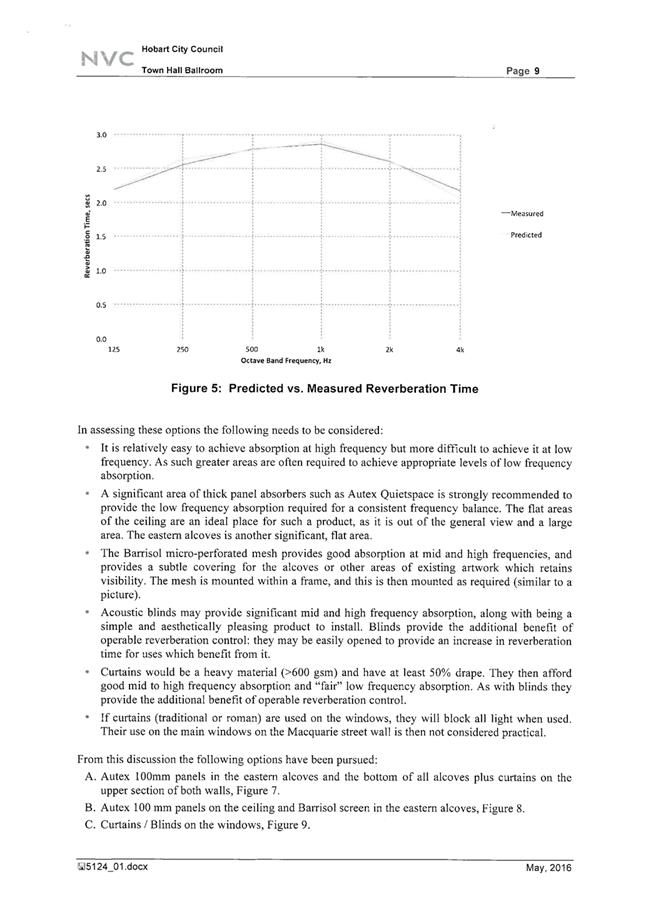

· Reverberation and background noise are both issues, with the former being problematic to address given the design of the space and the importance of retaining its heritage fabric;

· Speaking engagements present the most significant problems;

2.4.2. Given the varied use of the ballroom for events involving both speech and music, the consultant’s assessment worked towards a compromise, with a leaning towards improved speech conditions.

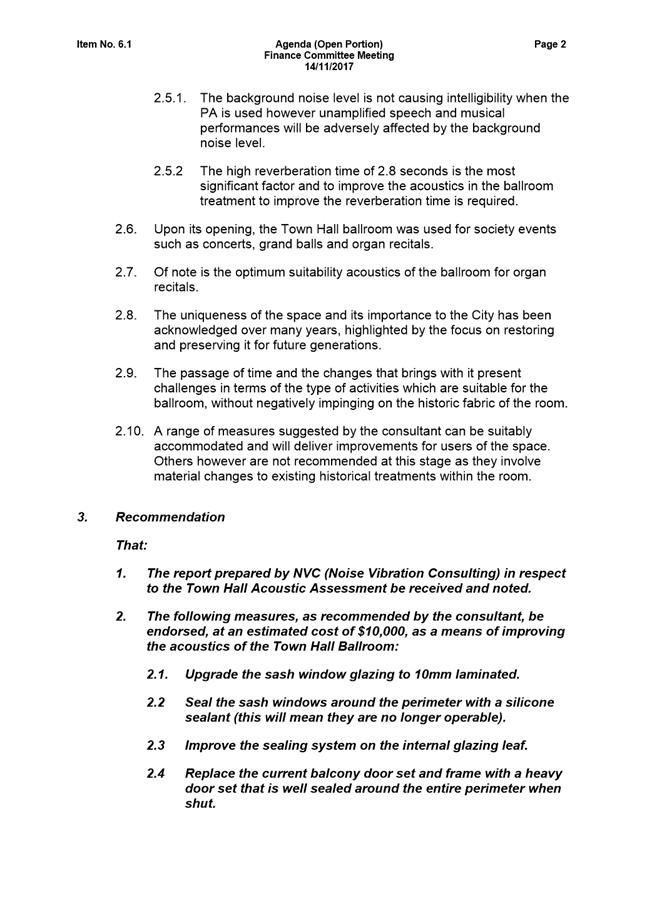

2.4.3. A range of recommended treatments were suggested which would reduce both the reverberation and background noise.

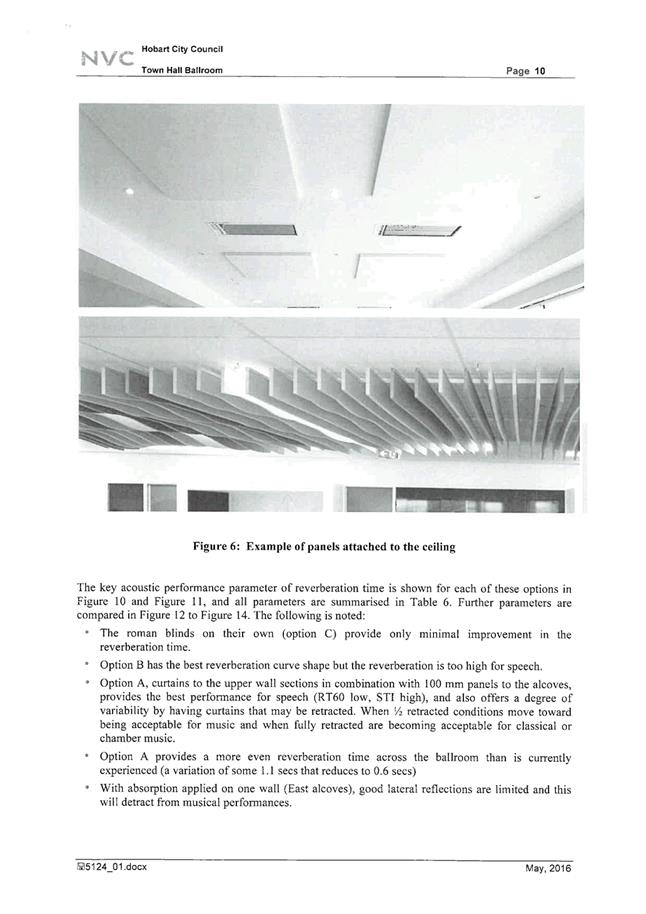

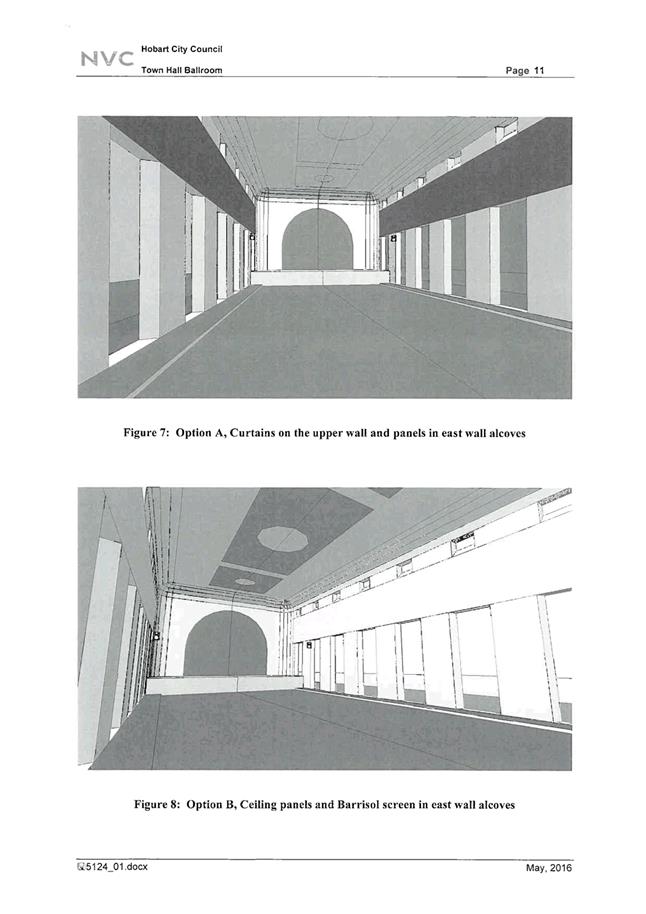

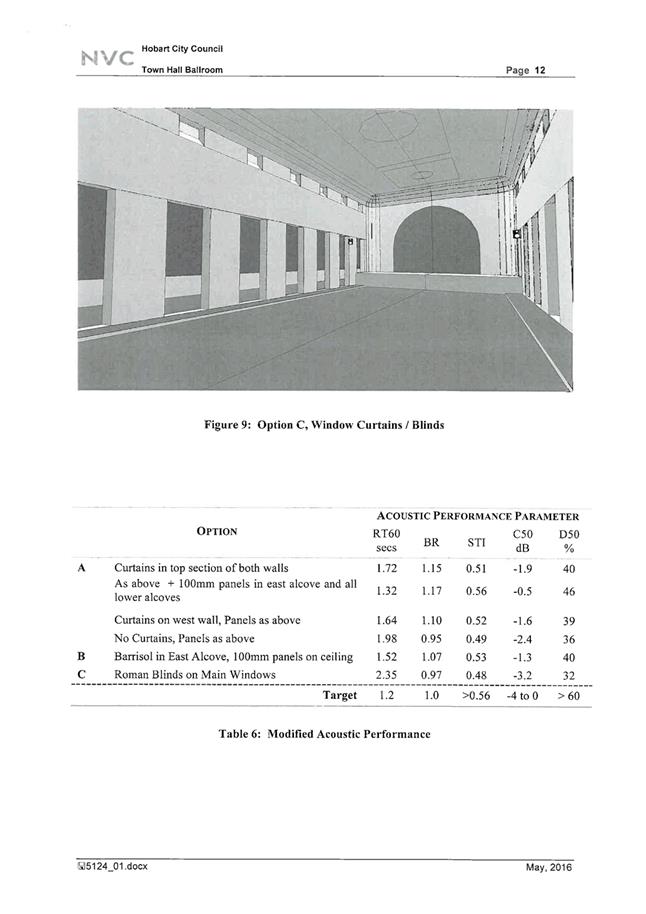

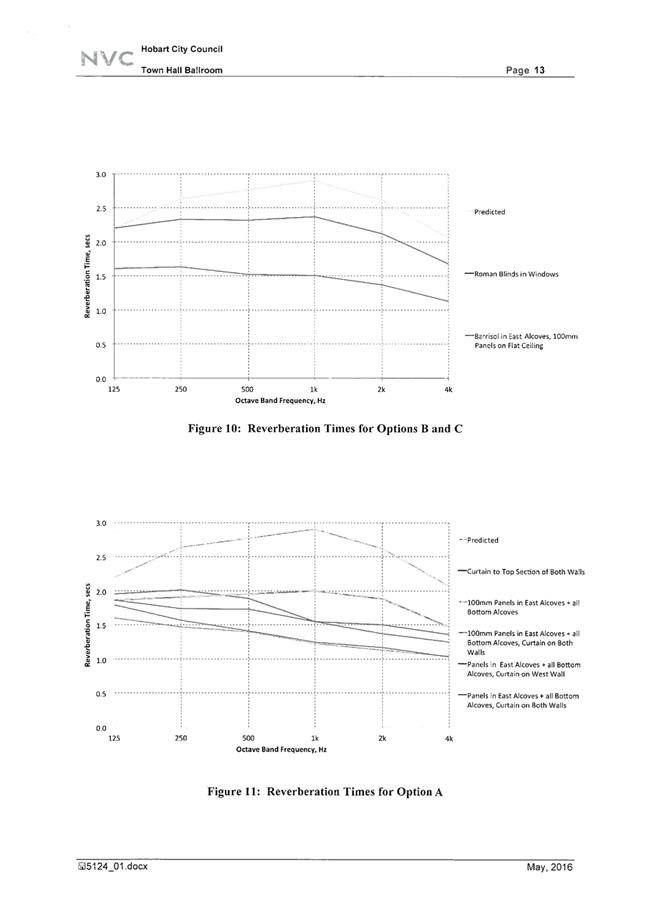

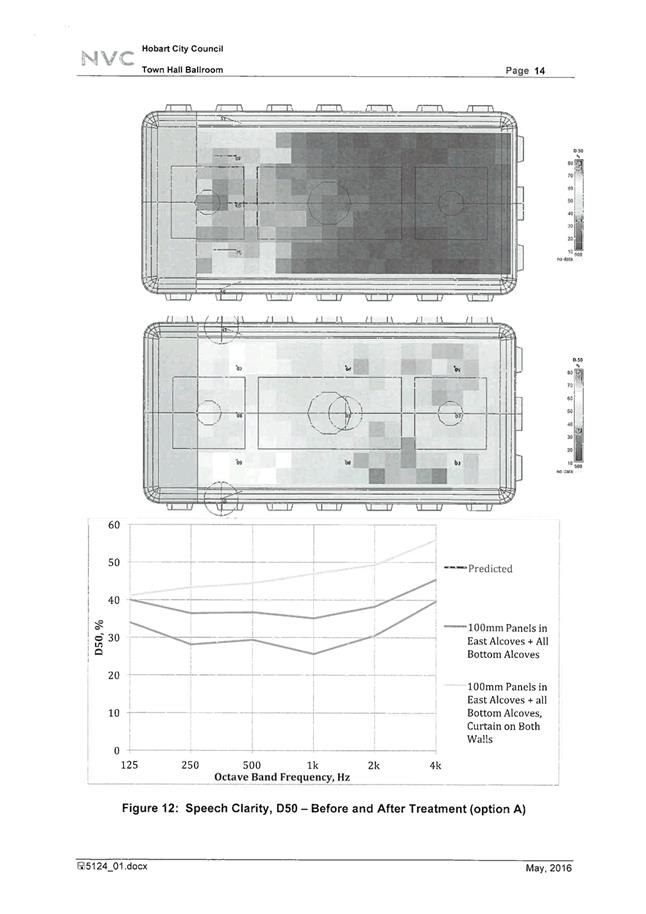

2.4.4. The suggested measures included a range of “soft” surface treatments to absorb sound and included installations such as sound panels in the ballroom alcoves, heavy weight curtains to the upper windows on both sides of the room and sound absorbing panelling to the ceiling of the room.

2.4.5. These measures, which essentially involve fixings and changes to the window furnishings were not favoured due to their impact on the heritage fabric of the ballroom.

2.4.6. Treatments which address the reduction of background noise are easier to deliver as they involve little or no impact on the presentation of the venue.

2.4.7. In this regard, the consultant’s recommendation involved replacement of the existing sash windows with thicker glass and the installation of fixed sealant preventing future opening. Improved sealing to the internal glazing leaf windows was also recommended.

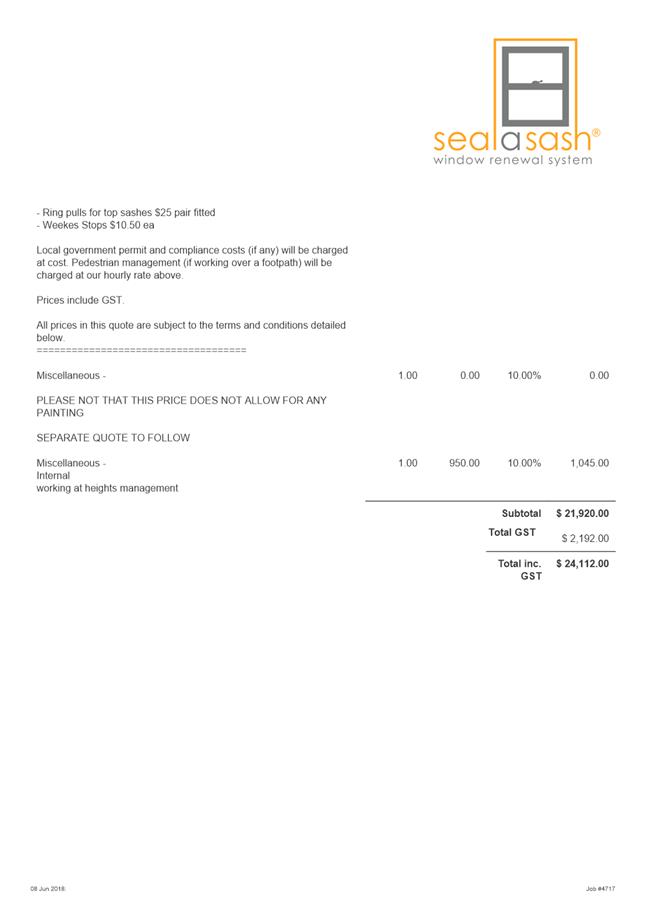

2.4.8. Whilst the Committee supported improvements to the windows to reduce noise, there was some concern that they would be inoperable after sealing. In considering the proposed treatment, the Committee also requested that other alternatives be addressed.

2.5. The Committee subsequently deferred the matter for further discussion with the consultant regarding additional glazing and sealing options for the Town Hall Ballroom windows.

|

That

1. In order to reduce the impact of background noise within the Town Hall ballroom, the improvements contained in the proposal outlining the Seal a Sash window renewal system, as outlined in attachment C to this report, be approved, at a cost of $25,000.

2. Funding be provided from the 2018/2019 Corporate Property budget.

|

4. Proposal and Implementation

4.1. In line with the Committee’s resolution, further discussions were conducted with the consultant in relation to other available options, including the potential use of Seal a Sash treatments and window shutters which were also discussed at the meeting.

4.2. The option of attaching window shutters was not considered to be an appropriate solution for the ballroom, due to their impact on the fabric of the space and given that the windows are the principal source of noise intrusion as they are inadequately sealed, allowing significant draught and noise infiltration, and the glass is old and thin.

4.3. Subsequent to these discussions, the proprietors of the window renewal system known as Seal a Sash were invited to inspect the windows and provide a suggested solution and costing.

4.4. Their proposal is shown as Attachment C to this report, and includes overhauling the seven existing double hung sash windows, providing draught sealing and replacing the existing glazing with Viridian ComfortHush 6.5mm glass.

4.4.1. ComfortHush glass includes a 3 layer laminate interlayer within 6.5mm glass which is designed to dampen noise, limit vibrations, and radiant heat, whilst maximising light and energy efficiency. It also provides UV protection to reduce fading of interior fittings and furnishings.

5. Strategic Planning and Policy Considerations

5.1. The reduction of sound bleed into the ballroom will provide a more pleasant experience for those who utilise this well-loved and important community space.

5.2. The opportunity to upgrade the windows will also provide asset maintenance to the City’s Town Hall building.

6. Stakeholder Consultation

6.1. The City’s Cultural Heritage Officer has been consulted in respect to heritage considerations of the ballroom, and concurs with the improvements recommended.

7. Financial Implications

7.1. Funding Source and Impact on Current Year Operating Result

7.1.1. The quoted price is $25,000.

7.1.2. Funding is available from the 2018/2019 Corporate Property budget

8. Legal, Risk and Legislative Considerations

8.1. There are no legal or risk implications arising from this report.

9. Delegation

9.1. This matter is reserved to the Council.

As signatory to this report, I certify that, pursuant to Section 55(1) of the Local Government Act 1993, I hold no interest, as referred to in Section 49 of the Local Government Act 1993, in matters contained in this report.

|

Margaret Johns Group Manager City Government and Customer Relations |

Heather Salisbury Deputy General Manager |

Date: 11 October 2018

File Reference: F18/117168

Attachment a: Report

Finance Committee 14 November 2017 ⇩ ![]()

Attachment

b: Consultants

Report ⇩ ![]()

Attachment

c: Seal

A Sash Proposal ⇩ ![]()

|

Item No. 6.6 |

Agenda (Open Portion) Finance and Governance Committee Meeting - 16/10/2018 |

Page 125 ATTACHMENT a |

|

Agenda (Open Portion) Finance and Governance Committee Meeting - 16/10/2018 |

Page 130 ATTACHMENT b |

|

Agenda (Open Portion) Finance and Governance Committee Meeting - 16/10/2018 |

Page 151 ATTACHMENT c |

|

Agenda (Open Portion) Finance and Governance Committee Meeting |

Page 158 |

|

|

|

16/10/2018 |

|

6.7 Waste Strategy Summit - 26 to 28 June 2018

Memorandum of the General Manager of 27 September 2018.

Delegation: Committee

|

Item No. 6.7 |

Agenda (Open Portion) Finance and Governance Committee Meeting |

Page 159 |

|

|

16/10/2018 |

|

Memorandum: Finance and Governance Committee

Waste Strategy Summit - 26 to 28 June 2018

In accordance with clause C(7)(1)(i) of the Council’s policy titled Aldermanic Development and Support, Alderman Harvey will be providing a verbal report to the Committee on his attendance at the Waste Strategy Summit in Sydney from 26 to 28 June 2018.

|

That the verbal report be received and noted.

|

As signatory to this report, I certify that, pursuant to Section 55(1) of the Local Government Act 1993, I hold no interest, as referred to in Section 49 of the Local Government Act 1993, in matters contained in this report.

|

N.D Heath General Manager |

|

Date: 27 September 2018

File Reference: F18/112417

|

Item No. 6.8 |

Agenda (Open Portion) Finance and Governance Committee Meeting |

Page 160 |

|

|

16/10/2018 |

|

6.8 Conference Reporting - Include Conference - August 2018 Wrest Point

Memorandum of the General Manager of 10 October 2018 and attachment.

Delegation: Committee

|

Item No. 6.8 |

Agenda (Open Portion) Finance and Governance Committee Meeting |

Page 161 |

|

|

16/10/2018 |

|

Memorandum: Finance and Governance Committee

Conference Reporting - Include Conference - August 2018 Wrest Point

Alderman Burnet has submitted the attached report in accordance with Clause C(7)(i) of the Council’s policy titled Aldermanic Development and Support.

|

That: 1. That the information be received and noted.

|

As signatory to this report, I certify that, pursuant to Section 55(1) of the Local Government Act 1993, I hold no interest, as referred to in Section 49 of the Local Government Act 1993, in matters contained in this report.

|

N.D Heath General Manager |

|

Date: 10 October 2018

File Reference: F18/114691

Attachment a: Include

Conference - August 2018 Wrest Point ⇩ ![]()

|

Item No. 6.8 |

Agenda (Open Portion) Finance and Governance Committee Meeting - 16/10/2018 |

Page 162 ATTACHMENT a |

|

Agenda (Open Portion) Finance and Governance Committee Meeting |

Page 164 |

|

|

|

11/10/2018 |

|

7.1 kunanyi/Hobart Visitation Policy and Strategy

Alderman Bill Harvey

Motion:

“That an officer report be prepared on the benefits and necessity of developing a long-term visitation policy and strategy for the City of Hobart and kunanyi/Mt Wellington to manage projected future tourist numbers.”

Rationale:

“The number of tourists visiting Hobart and kunanyi/Mt Wellington will continue to grow for the foreseeable future and it is important that the council consider and investigate the potential impacts and develop strategies to mitigate such impacts. The increase in tourism needs to be managed in a forward looking strategic way, rather than as a reaction as it occurs. Forward planning could be the key to avoiding some of the many issues that are now being experienced in other places.

Globally, mass tourism is having an impact on local communities and cultures who are feeling the pressure of huge numbers of visitors. Some of the potential impacts of mass tourism include pressure on council infrastructure, facilities and services; an increase in housing shortages and homelessness associated with conversion of permanent housing to short stay; pressure on the local environment and waste management; pressure on local communities who have to live with an increasing number of tourists, traffic and changing social environment and local economies increasingly focused on tourism services rather than provision of local services.

Kunanyi/Mt Wellington especially needs a visitation strategy as number of visitors continues to grow putting more pressure on the fragile alpine environment, biodiversity and water catchment.

Considering the sustained growth in tourism, it is increasingly urgent that the council consider the implications of future tourism and develop a policy and strategies to mitigate potential future issues.”

The General Manager reports:

“In line with the Council’s policy in relation to Notices of Motion, I advise that the matter is considered to be within the jurisdiction of the Hobart City Council as it relates to Council owned land.”

|

Agenda (Open Portion) Finance and Governance Committee Meeting |

Page 166 |

|

|

|

16/10/2018 |

|

A report indicating the status of current decisions is attached for the information of Aldermen.

REcommendation

That the information be received and noted.

Delegation: Committee

|

Item No. 8.1 |

Agenda (Open Portion) Finance and Governance Committee Meeting - 16/10/2018 |

Page 167 ATTACHMENT a |

|

Agenda (Open Portion) Finance and Governance Committee Meeting |

Page 177 |

|

|

|

16/10/2018 |

|

Regulation 29(3) Local Government

(Meeting Procedures) Regulations 2015.

File Ref: 13-1-10

The General Manager reports:-

“In accordance with the procedures approved in respect to Questions Without Notice, the following responses to questions taken on notice are provided to the Committee for information.

The Committee is reminded that in accordance with Regulation 29(3) of the Local Government (Meeting Procedures) Regulations 2015, the Chairman is not to allow discussion or debate on either the question or the response.”

9.1 Potential Mapping of Council Services

File Ref: F18/92883; 13-1-10

Memorandum of the Deputy General Manager of 9 October 2018.

9.2 Development of an International Association for Public Participation Program for Aldermen

File Ref: F18/93058; 13-1-10

Memorandum of the Acting Associate Director Community and Culture of 10 October 2018.

Delegation: Committee

|

That the information be received and noted.

|

|

Item No. 9.1 |

Agenda (Open Portion) Finance and Governance Committee Meeting |

Page 178 |

|

|

16/10/2018 |

|

Memorandum: Lord Mayor

Deputy Lord Mayor

Aldermen

Response to Question Without Notice

Potential Mapping of Council Services

|

Meeting: Finance and Governance Committee

|

Meeting date: 14 August 2018

|

|

Raised by: Alderman Ruzicka |

|

Question:

Will Council consider mapping out a set of its services as a means of demonstrating how efficiently and effectively they meet user focus, a delivery mindset and are learning/iterative processes?

Response:

The City is currently in the process of preparing for the staged implementation of a suite of upgraded and new business systems across the organisation through Project Phoenix.

In addition to the delivery of updated systems supporting our existing core business functions, including finance, payroll, asset services and planning; a suite of new systems will assist the organisation to improve customer service and importantly, make it easier for customers to do business with the City.

In order to effectively plan for the design and implementation of updated and new systems which provide improved functionality and integration and deliver improved outcomes for the City’s customers, it is necessary to have a detailed knowledge and understanding of the processes which underpin existing service delivery.

Mapping of the processes which support current, and future service delivery is integral to the identification and delivery of improved systems and services for our community.

The undertaking of the City’s business systems transformation through Project Phoenix has provided the opportunity for the City to undertake what is possibly the most significant review of service delivery across the whole of Council.

As signatory to this report, I certify that, pursuant to Section 55(1) of the Local Government Act 1993, I hold no interest, as referred to in Section 49 of the Local Government Act 1993, in matters contained in this report.

|

Heather Salisbury Deputy General Manager |

|

Date: 9 October 2018

File Reference: F18/92883; 13-1-10

|

Item No. 9.2 |

Agenda (Open Portion) Finance and Governance Committee Meeting |

Page 180 |

|

|

16/10/2018 |

|

Memorandum: Lord Mayor

Deputy Lord Mayor

Aldermen

Response to Question Without Notice

Development of an International Association for Public Participation Program for Aldermen

|

Meeting: Finance and Governance Committee

|

Meeting date: 14 August 2018

|

|

Raised by: Alderman Ruzicka |

|

Question:

Can an International Association for Public Participation program be developed as part of elected members’ professional development with the aim of ensuring best practice in community engagement with continuous updates on knowledge and practice?

Response:

The Council at its meeting of October 8, 2018, endorsed its Community Engagement Framework to guide the City’s work in relation to community engagement practice into the future.

The City’s approach to community engagement is based on the process set out within the IAP2 Quality Assurance Standard for Community and Stakeholder Engagement (2015).

In addition to adopting the IAP2 core values for community and stakeholder engagement and using the IAP2 code of ethics to enhance the integrity of the City’s practices, a standard process for engagement is undertaken to ensure a quality community engagement result.

The Engaged Communities team within the Community and Culture Division work closely across the organisation to provide specialist advice and support, thereby ensuring that the City employs a consistent, community-focused approach to decision-making.

These officers, together with key staff from across the organisation are trained in International Association for Public Participation (IAP2) engagement techniques, which enable them to support and champion excellence in community engagement practice and build the City’s organisational capacity.

The International Association for Public Participation offers training specifically designed for decision makers and it is intended that in 2019, consideration be given as to the interest of Aldermen for a session of training to be delivered in Hobart.

As signatory to this report, I certify that, pursuant to Section 55(1) of the Local Government Act 1993, I hold no interest, as referred to in Section 49 of the Local Government Act 1993, in matters contained in this report.

|

Kimbra Parker Acting Associate Director Community and Culture |

|

Date: 10 October 2018

File Reference: F18/93058; 13-1-10

|

|

Agenda (Open Portion) Finance and Governance Committee Meeting |

Page 182 |

|

|

16/10/2018 |

|

Section 29 of the Local Government (Meeting Procedures) Regulations 2015.

File Ref: 13-1-10

An Alderman may ask a question without notice of the Chairman, another Alderman, the General Manager or the General Manager’s representative, in line with the following procedures:

1. The Chairman will refuse to accept a question without notice if it does not relate to the Terms of Reference of the Council committee at which it is asked.

2. In putting a question without notice, an Alderman must not:

(i) offer an argument or opinion; or

(ii) draw any inferences or make any imputations – except so far as may be necessary to explain the question.

3. The Chairman must not permit any debate of a question without notice or its answer.

4. The Chairman, Aldermen, General Manager or General Manager’s representative who is asked a question may decline to answer the question, if in the opinion of the respondent it is considered inappropriate due to its being unclear, insulting or improper.

5. The Chairman may require a question to be put in writing.

6. Where a question without notice is asked and answered at a meeting, both the question and the response will be recorded in the minutes of that meeting.

7. Where a response is not able to be provided at the meeting, the question will be taken on notice and

(i) the minutes of the meeting at which the question is asked will record the question and the fact that it has been taken on notice.

(ii) a written response will be provided to all Aldermen, at the appropriate time.

(iii) upon the answer to the question being circulated to Aldermen, both the question and the answer will be listed on the agenda for the next available ordinary meeting of the committee at which it was asked, where it will be listed for noting purposes only.

|

|

Agenda (Open Portion) Finance and Governance Committee Meeting |

Page 183 |

|

|

16/10/2018 |

|

|

That the Council resolve by absolute majority that the meeting be closed to the public pursuant to regulation 15(1) of the Local Government (Meeting Procedures) Regulations 2015 because the items included on the closed agenda contain the following matters:

· proposals for the council to acquire land or an interest in land or for the disposal of land the sale of land for unpaid rates · information of a personal and confidential nature or information provided to the council on the condition it is kept confidential · the security of the property of the council

The following items are listed for discussion:-

Item No. 1 Minutes of the last meeting of the Closed Portion of the Council Meeting Item No. 2 Consideration of supplementary items to the agenda Item No. 3 Indications of pecuniary and conflicts of interest Item No. 4 Reports Item No. 4.1 3 Morrison Street, Hobart - Short Term Lease LG(MP)R 15(2)(f) Item No. 4.2 Remissions of Rates and Charges Granted LG(MP)R 15(2)(g) Item No. 4.3 Town Hall Security - Installation of Additional Door LG(MP)R 15(2)e(ii) Item No. 5 Committee Action Status Report Item No. 5.1 Committee Actions - Status Report LG(MP)R 15(2)(a) Item No. 6 Questions Without Notice

|