City

of hobart

AGENDA

Finance Committee Meeting

Open Portion

Tuesday, 16 May 2017

at 5.00 pm

Lady Osborne Room, Town Hall

City

of hobart

AGENDA

Finance Committee Meeting

Open Portion

Tuesday, 16 May 2017

at 5.00 pm

Lady Osborne Room, Town Hall

THE MISSION

Our mission is to ensure good governance of our capital City.

THE VALUES

The Council is:

|

about people |

We value people – our community, our customers and colleagues. |

|

professional |

We take pride in our work. |

|

enterprising |

We look for ways to create value. |

|

responsive |

We’re accessible and focused on service. |

|

inclusive |

We respect diversity in people and ideas. |

|

making a difference |

We recognise that everything we do shapes Hobart’s future. |

|

|

Agenda (Open Portion) Finance Committee Meeting |

Page 3 |

|

|

16/5/2017 |

|

Business listed on the agenda is to be conducted in the order in which it is set out, unless the committee by simple majority determines otherwise.

APOLOGIES AND LEAVE OF ABSENCE

1. Co-Option of a Committee Member in the event of a vacancy

3. Consideration of Supplementary Items

4. Indications of Pecuniary and Conflicts of Interest

6.1 Sandy Bay Bathing Pavilion - Proposed Development of a Second Floor

6.2 Property Valuation Adjustments (Indexation)

6.3 Financial Report as at 31 March 2017

6.4 Grants and Benefits Listing as at 31 March 2017

6.5 Write-Off of Debts - Further Information

6.6 2017/2018 Fees and Charges - Financial Services

6.7 2017/2018 Fees and Charges - Parking Operations

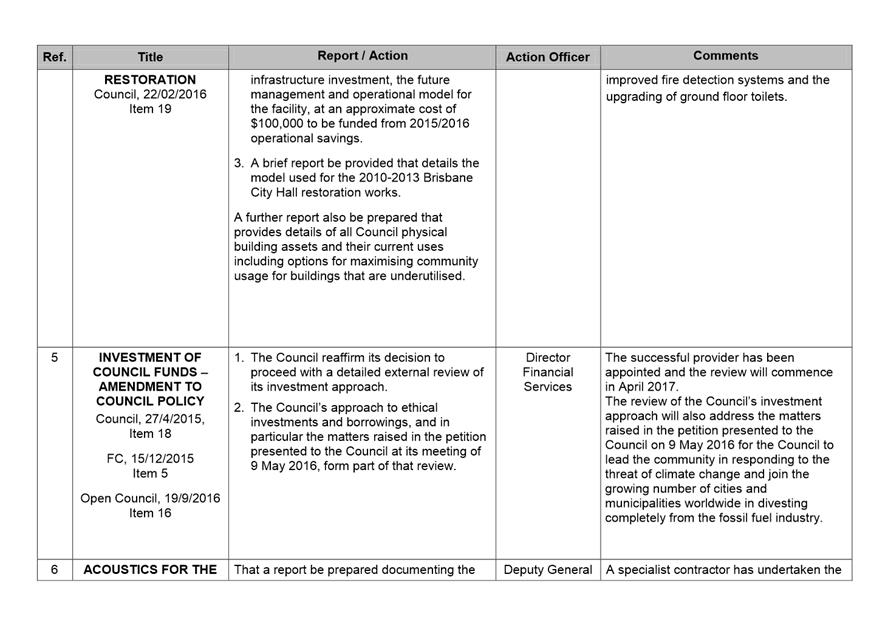

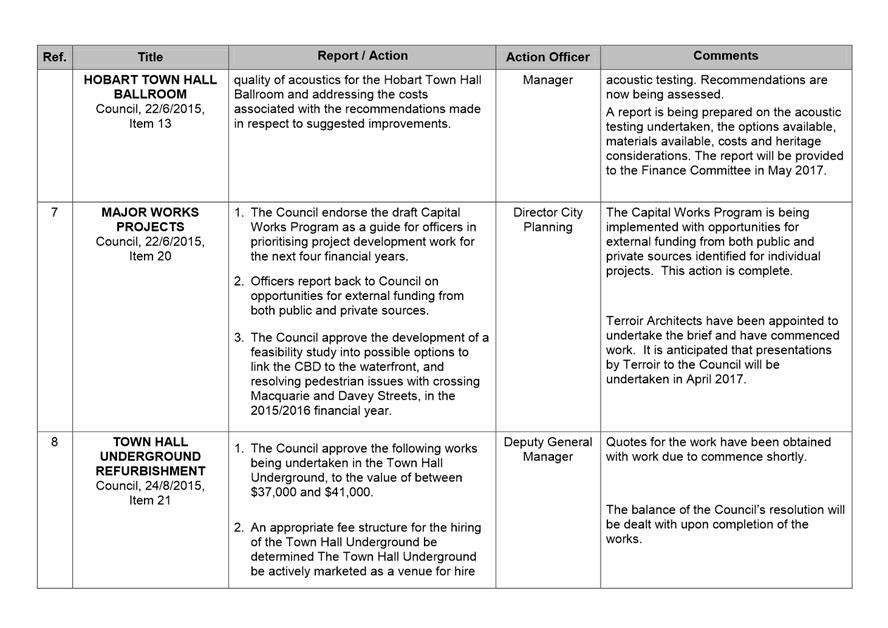

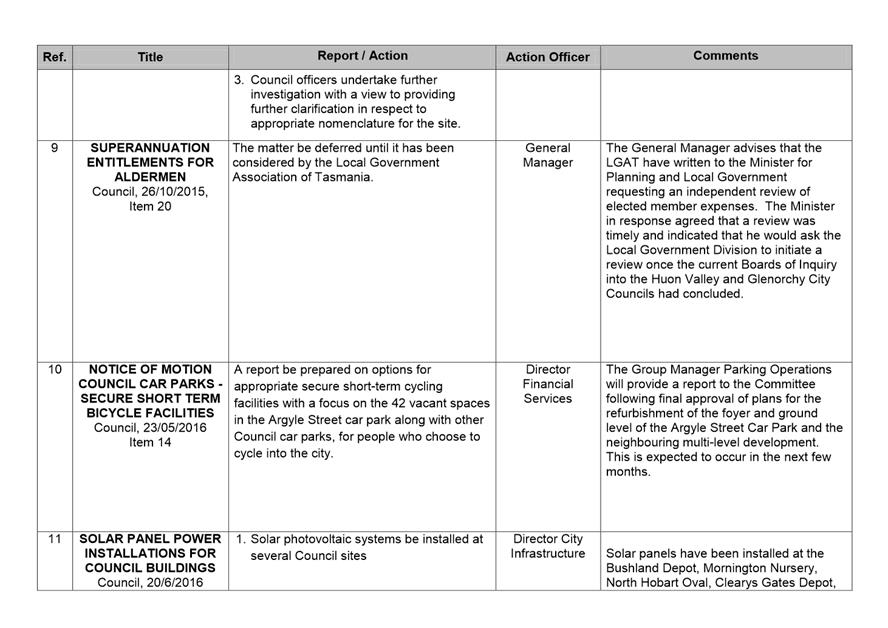

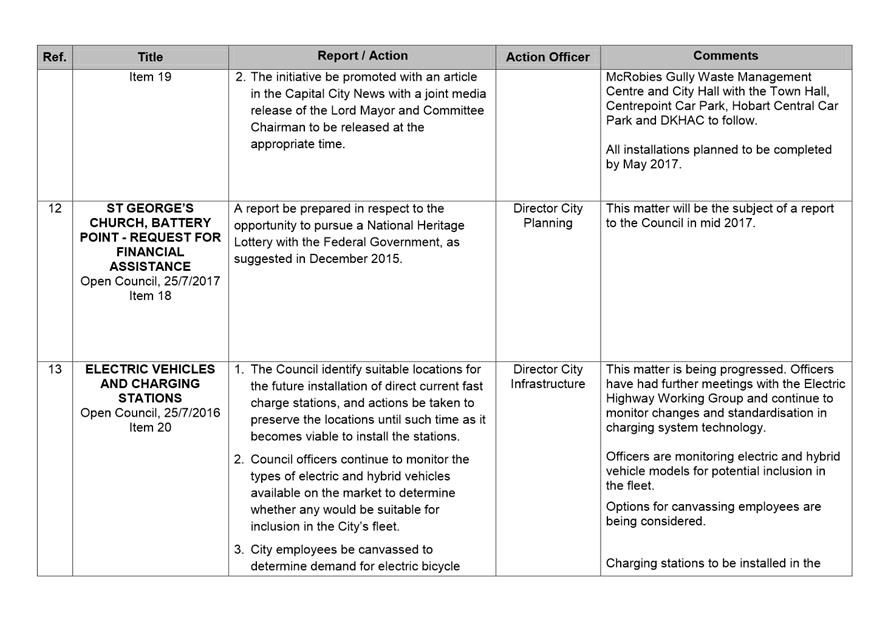

7 Committee Action Status Report

7.1 Committee Actions - Status Report

9. Closed Portion Of The Meeting

|

|

Agenda (Open Portion) Finance Committee Meeting |

Page 5 |

|

|

16/5/2017 |

|

Finance Committee Meeting (Open Portion) held Tuesday, 16 May 2017 at 5.00 pm in the Lady Osborne Room, Town Hall.

|

COMMITTEE MEMBERS Thomas (Chairman) Deputy Lord Mayor Christie Zucco Ruzicka Sexton

ALDERMEN Lord Mayor Hickey Briscoe Burnet Cocker Reynolds Denison Harvey |

Apologies: Nil.

Leave of Absence: Alderman Thomas. Alderman Zucco.

|

|

The minutes of the Open Portion of the Finance Committee meeting held on Tuesday, 11 April 2017, are submitted for confirming as an accurate record.

|

Ref: Part 2, Regulation 8(6) of the Local Government (Meeting Procedures) Regulations 2015.

|

That the Committee resolve to deal with any supplementary items not appearing on the agenda, as reported by the General Manager.

|

Ref: Part 2, Regulation 8(7) of the Local Government (Meeting Procedures) Regulations 2015.

Aldermen are requested to indicate where they may have any pecuniary or conflict of interest in respect to any matter appearing on the agenda, or any supplementary item to the agenda, which the committee has resolved to deal with.

Regulation 15 of the Local Government (Meeting Procedures) Regulations 2015.

A committee may close a part of a meeting to the public where a matter to be discussed falls within 15(2) of the above regulations.

In the event that the committee transfer an item to the closed portion, the reasons for doing so should be stated.

Are there any items which should be transferred from this agenda to the closed portion of the agenda, or from the closed to the open portion of the agenda?

|

Agenda (Open Portion) Finance Committee Meeting |

Page 6 |

|

|

|

16/5/2017 |

|

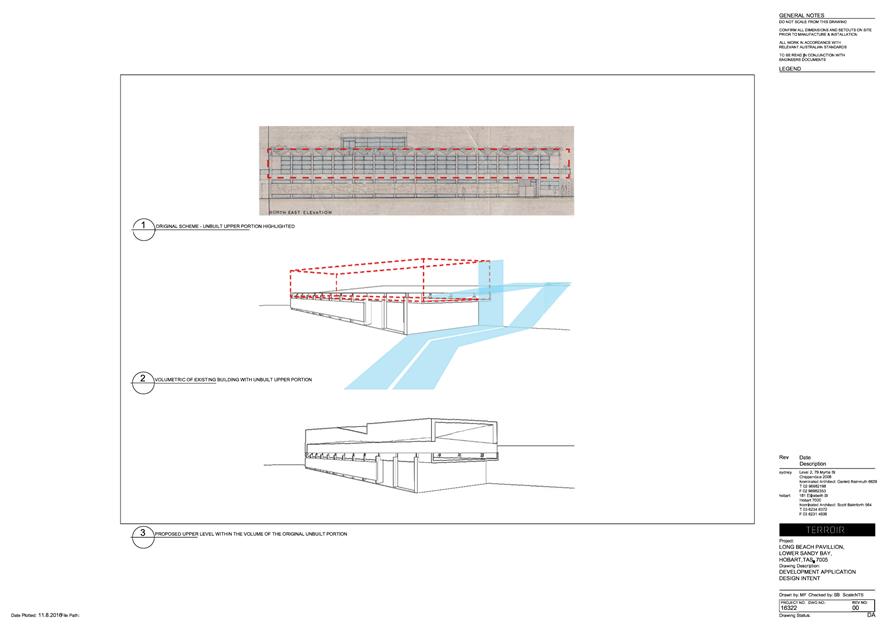

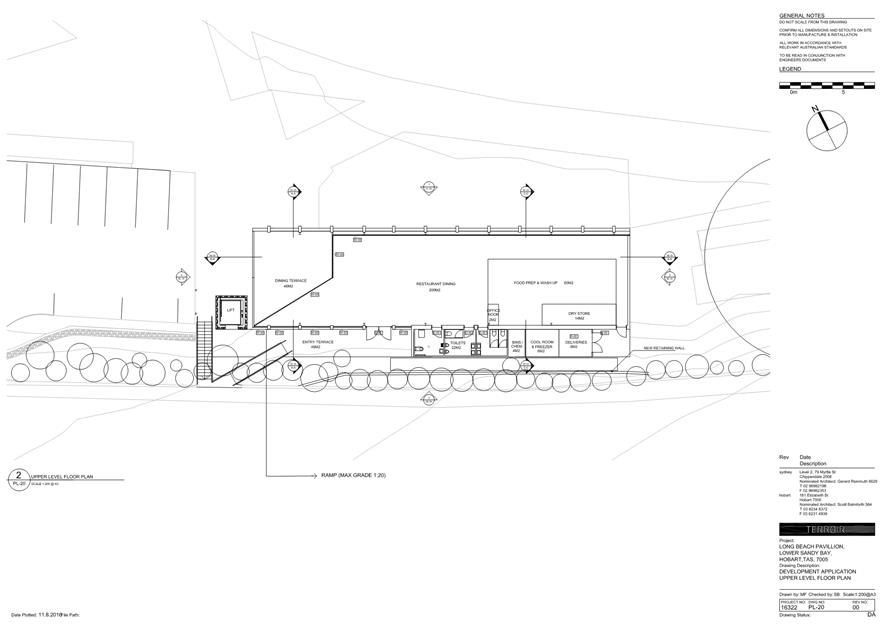

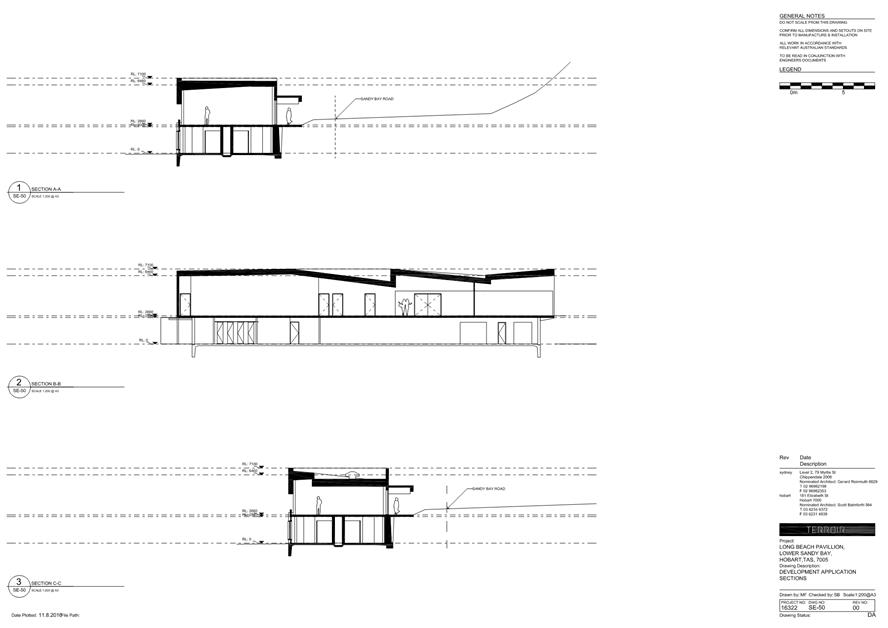

6.1 Sandy Bay Bathing Pavilion - Proposed Development of a Second Floor

File Ref: F17/33781

Report of the Economic Development Project Officer and the Director Parks and City Amenity of 11 May 2017 and attachment.

Delegation: Council

|

Item No. 6.1 |

Agenda (Open Portion) Finance Committee Meeting |

Page 8 |

|

|

16/5/2017 |

|

REPORT TITLE: Sandy Bay Bathing Pavilion - Proposed Development of a Second Floor

REPORT PROVIDED BY: Economic Development Project Officer

Director Parks and City Amenity

1. Report Purpose and Community Benefit

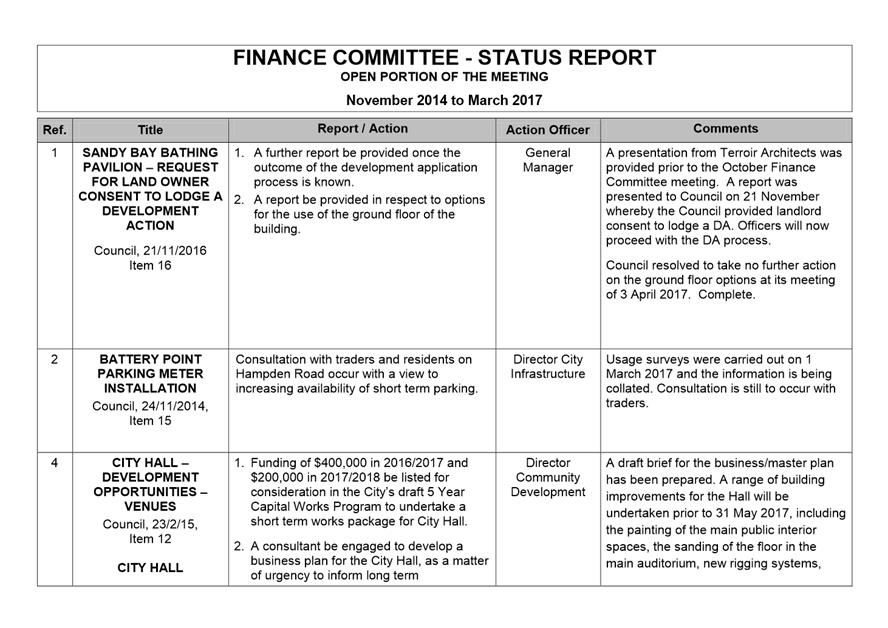

1.1. The purpose of this report is to provide an update on the potential development of a second floor restaurant above the existing Sandy Bay Bathing Pavilion.

1.2. The community benefit associated with this development is that it would increase the community use of a Council owned building located in a prime position overlooking Long Beach, Lower Sandy Bay.

2. Report Summary

2.1. The Council as landowner granted consent for the lodgement of a development application on 21 November, 2016 for a second floor restaurant above the existing Pavilion.

2.2. City officers are in the process of completing all necessary actions needed for the submission of a development application (DA) for the construction of a second floor restaurant above the Sandy Bay Bathing Pavilion (Pavilion).

2.3. As part of the process of submitting a DA, supporting information has been developed and gathered, including a Conservation Management Plan.

2.4. A Conservation Management Plan was requested by the Tasmanian Heritage Council before a development application for the Pavilion could be considered. The Pavilion was permanently placed on the Tasmanian Heritage Register, under the Historic Cultural Heritage Act 1995) which means changes to the Pavilion require approval from not only the City of Hobart as planning authority, but also the Tasmanian Heritage Council.

2.5. Policy 14 in the Conservation Management Plan states:

Prior to making decisions about change to the Pavilion, consult with the architect of the Pavilion, or his agent, in accordance with the provisions of the Copyright (Moral Rights) Amendment Act 2000.”

2.6. The design for a second floor restaurant has been shared with the original architect of the Pavilion (Mr Dirk Bolt). Mr Bolt’s response indicated that he is not supportive of this design concept.

2.7. The Tasmanian Heritage Council has provided feedback that Mr Bolt’s view is significant and that it would be prudent to submit a design that Mr Bolt had endorsed.

2.8. This presents the Council with three options in relation to this project:

Option 1

Submit a development application with the current design (Attachment A)

for a second floor restaurant above the existing Pavilion that is not supported

by Mr Bolt.

Option 2

Re-consider the design for the second floor restaurant in conjunction with Mr

Bolt. Submit a development application with a new design endorsed by Mr

Bolt.

Option 3

Do not proceed with any form of development application for a second floor

restaurant above the existing Pavilion at the present time.

2.9. It is recommended that option three is endorsed by Council. The main reasons for this recommendation are:

2.9.1. Capping costs relating to a redesign of the second floor or an appeal associated with a development application.

2.9.2. Current uncertainty about the future use of the ground floor of the Pavilion.

2.9.3. Current uncertainty about the future operations of Prossers Restaurant (500 metres away from the Pavilion).

|

That proposals associated with the development of a new second floor restaurant above the existing Sandy Bay Bathing Pavilion not be proceeded with, at this time. |

4. Background

4.1. The Sandy Bay Bathing Pavilion (Pavilion) is a City asset, located at 646A Sandy Bay Road, Lower Sandy Bay.

4.2. It was designed by architect Mr Dirk Bolt and constructed in 1962.

4.3. The Council has considered the development of a second floor on a number of occasions (2001, 2009 and 2013).

4.3.1. A planning permit was issued in 2001 for a 90 seat restaurant. This was later replaced with a refusal following appeal.

4.4. Following a notice of motion in May 2013, the Council proceeded to examine the possible re-development and future uses of a new upper level of the Pavilion.

4.5. The City contacted the Tasmanian Heritage Council (THC) in November 2013 in relation to development plans. THC advised that a conservation management plan would be required before consideration of a development proposal.

4.6. As the Pavilion is permanently listed in the Tasmanian Heritage Register, approval for development is required from the City of Hobart as planning authority and also the Tasmanian Heritage Council.

4.7. A Conservation Management Plan (CMP) was completed in May 2015.

4.8. Policy 14 in the CMP states:

Prior to making decisions about change to the Pavilion, consult with the architect of the Pavilion, or his agent, in accordance with the provisions of the Copyright (Moral Rights) Amendment Act 2000.”

4.9. A design for a second floor of the Pavilion was presented to the Council on 21 November 2016 with the Council as landowner granting consent for the lodgement of a DA.

4.9.1. This design was sent to Mr Bolt in February 2017 for comment.

4.10. Mr Bolt responded promptly and questioned the rationale of the new design. Mr Bolt also made a number of suggestions for the design of a second floor on top of the existing Pavilion. Mr Bolt’s response made it clear that he did not support the design.

5. Proposal and Implementation

5.1. The recent feedback from Mr Bolt and advice from THC give the Council three options in relation to the potential development of a second floor on top of the Pavilion. Each option has differing implications for the Council.

Option 1

5.2. Submit a development application with the current design for a second floor restaurant above the existing Pavilion that is not supported by Mr Bolt.

5.2.1. This option would present the most risk to the City as the THC has provided feedback that the view of Mr Bolt will be significant in the its consideration of the development application. Submission of the existing design would be unlikely to be approved by THC.

Option 2

5.3. Re-consider the design for the second floor restaurant in conjunction with Mr Bolt. Submit a development application with a new design endorsed by Mr Bolt. Amend supporting reports that are currently relevant to the current designs (e.g. Heritage Impact Assessment).

5.3.1. This option would pose less initial risk to the City in terms of the THC’s consideration of a development application for a second floor restaurant.

5.3.2. It must be acknowledged however that should the THC and the City as planning authority grant a development application for a second floor restaurant, there is potential for the decision to be appealed by parties such as nearby residents or businesses. Should this occur, it is likely that costs associated with this project would escalate.

5.3.3. Both re-designing the second floor of the restaurant and / or taking part in an appeal process is likely to incur significant cost to the City.

5.3.3.1. $20,000 was budgeted to progress the project to a development application submission stage.

5.3.3.2. It is not unreasonable to estimate costs associated with a re-design including architect fees, heritage services and planning advice would incur a further $20,000. This has not been included in the 2017/18 budget.

Option 3

5.4. Do not proceed with any form of development application for a second floor restaurant above the existing Pavilion, at the present time.

5.4.1. The notice of motion of May 2013 pre-dates the current Council. Given the lapse of time since the original decision, there is the question of the appetite of the current Council to continue to proceed with this project, given rising costs.

5.4.2. Costs associated with the lodgement of a development application have now been expended. This project has not been included in the ten year capital works program.

5.4.3. Arriving at a design that is acceptable to Mr Bolt, the City, the THC and the planning authority could prove a complex and lengthy process.

5.4.4. A nearby restaurant (Prossers) is currently for sale. Any subsequent change of operator at this location could impact the viability of the proposed restaurant development at the Pavilion. The two locations are approximately 500 metres apart.

5.4.5. The Council on 3 April 2017 has additionally been considering the use of the existing ground floor of the Pavilion and resolved:

Consideration of the future expanded or amended use of the leased ground floor area of the Sandy Bay Bathing Pavilion, Long Beach be deferred until 2020, noting that:

(i) Surf Life Saving Tasmania hold a lease on the area until September 2020;

(ii) The Council is progressing a proposal to seek development of a second floor of the building.

It may be appropriate for the Council to re-visit the potential of a second

floor development in 2020 when it can look at the building holistically and

with more clarity around operations at Prossers restaurant.

5.4.6. Opting not to proceed with a development at this time would ensure that no more costs are incurred by the City.

5.4.7. Opting

not to proceed would however not present a positive outcome for the community

in terms of enabling a wider use of the Pavilion and its prime location.

It must be noted that the Conservation Management Plan advocates public access

to the building of the existing ground floor and a potential second floor.

6. Strategic Planning and Policy Considerations

6.1. Consideration of development of the Pavilion is in line with the following ‘Future Directions’ detailed in the City of Hobart 2025 Community Vision.

-Offers opportunities for all ages and a city for life.

-Is well governed at a regional and community level.

-Achieves good quality development and urban management.

-Is dynamic, vibrant and culturally expressive.

6.2. Development of this facility is in line with the following strategic objectives of the Economic Development Strategy 2013-2018.

3.1.3 - Visitor Attraction

3.3.1 - Facilitation of significant city developments

7. Financial Implications

7.1. Funding Source and Impact on Current Year Operating Result

7.1.1. The Council on 21 December 2015 resolved:

That the Council authorise the General Manager to progress an expansion of the use of the Sandy Bay Bathing Pavilion by developing and submitting a development application for a generic restaurant facility, on a second floor, at an estimated cost of up to $20,000.

7.1.2. The sum of $20,000 referred to above has been expended on activities associated with the development application including architect designs, traffic impact assessment and heritage impact assessment.

7.1.3. Any future costs associated with the continued pursuit of a development application have not been included in the current year’s budget.

7.1.4. Should the Council support the re-design of the second floor restaurant concept and submission of a development application, it is not unreasonable to estimate that costs associated (including design, re-consideration of heritage impact etc.) would total a further $20,000.

7.1.5. Should an appeal be lodged against a DA decision, costs could escalate significantly.

7.2. Impact on Future Years’ Financial Result

7.2.1. Impact on future years’ financial results will be dependent on the approach advocated by the Council.

7.2.2. It must be noted that the development of the Sandy Bay Bathing Pavilion has not been included in the Council-endorsed 10 year capital works program.

7.3. Asset Related Implications

7.3.1. This asset is owned by the City and as such will require ongoing maintenance. Commercial development of the Pavilion would assist in off-setting the maintenance costs.

8. Legal, Risk and Legislative Considerations

8.1. The degree of legal, risk and legislative conditions will be dependent on the approach advocated by the Council.

8.2. Option 1 (submit a development application for the existing design) would involve significant risk of not securing THC approval.

8.3. Option 2 (re-design the proposed second floor of the Pavilion, secure the endorsement of Mr Dirk Bolt and submit development application) presents the significant risk of further costs associated with the re-design. Should a development application be granted, there is the potential that this decision could be appealed which would have significant cost implications for the Council.

8.4. Option 3 (do not pursue development at this time) minimises costs and legal challenges but does not provide the community with an expanded use of this facility.

9. Social and Customer Considerations

9.1. The development of a second floor restaurant facility at the Pavilion would increase the community use of this Council owned building located in a prime position overlooking Little Sandy Bay Beach.

9.2. Some members of the community such as local residents and businesses may not support the development of a second floor.

9.3. Should Council continue to pursue the development of the Pavilion, costs associated with this may be questioned by community members.

10. Community and Stakeholder Engagement

10.1. Mr Dirk Bolt (Architect of the Sandy Bay Bathing Pavilion).

10.2. Tasmanian Heritage Council.

10.3. Architect of current design for a second floor of the Pavilion.

10.4. Manager Legal & Governance.

11. Delegation

11.1. This matter is delegated to the Council.

As signatory to this report, I certify that, pursuant to Section 55(1) of the Local Government Act 1993, I hold no interest, as referred to in Section 49 of the Local Government Act 1993, in matters contained in this report.

|

Lucy Knott Economic Development Project Officer |

Glenn Doyle Director Parks and City Amenity |

Date: 11 May 2017

File Reference: F17/33781

Attachment a: Finance

Committee - 15 November 2016 - Final Designs Second Floor Restaurant Sandy Bay

Bathing Pavilion ⇩ ![]()

|

Item No. 6.2 |

Agenda (Open Portion) Finance Committee Meeting |

Page 19 |

|

|

16/5/2017 |

|

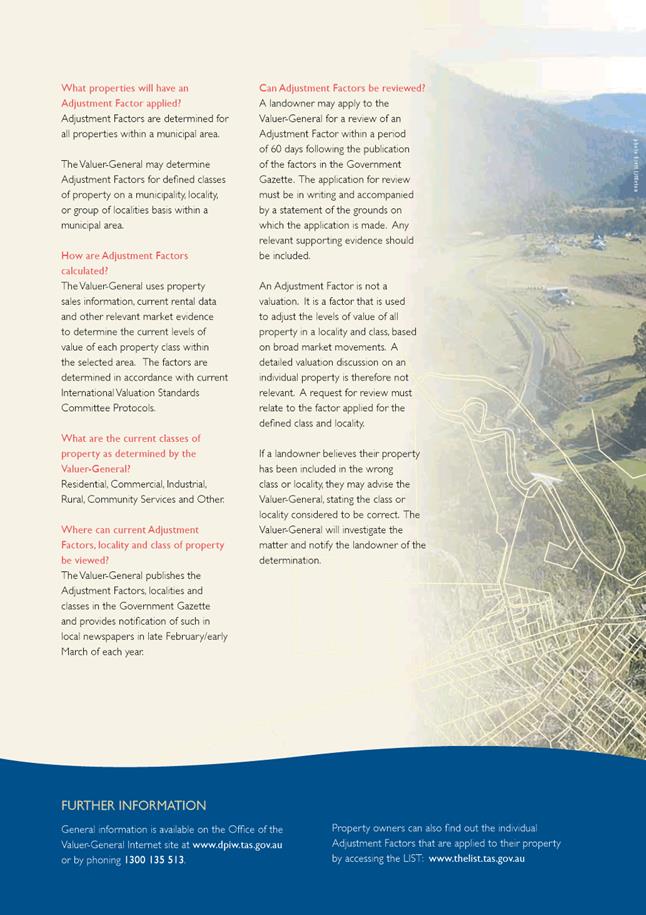

6.2 Property Valuation Adjustments (Indexation)

File Ref: F17/40149; 22-1-3

Report of the Group Manager Rates and Procurement and the Director Financial Services of 11 May 2017 and attachment.

Delegation: Committee

|

Item No. 6.2 |

Agenda (Open Portion) Finance Committee Meeting |

Page 21 |

|

|

16/5/2017 |

|

REPORT TITLE: Property Valuation Adjustments (Indexation)

REPORT PROVIDED BY: Group Manager Rates and Procurement

Director Financial Services

1. Report Purpose and Community Benefit

1.1. The purpose of this report is to:

1.1.1. Provide information to the Committee on the impact of property valuation adjustment factors received from the Valuer-General for the 2017/2018 rating year on individual property owners in respect of rates levied for 2017/2018; and

1.1.2. Consider the impact on Council’s rating strategy resulting from indexation.

1.2. The community benefits from the continual review of Council’s rating strategy to ensure the City has a rating system that supports fairness, capacity to pay and effectiveness.

2. Report Summary

2.1. This report provides information on the impacts of Assessed Annual Value (AAV) adjustment factors for the 2017/2018 rating year.

2.2. Generally, the AAVs for residential properties will increase by 5%, however, the AAVs for most non-residential properties will stay the same. The only exceptions to this is that all vacant land AAVs will increase by 10% as will the AAVs of properties classed as primary production.

2.3. The effect of higher adjustment factors for residential properties than for non-residential properties is a shift in the rate burden from non-residential to residential.

2.4. Rates modelling undertaken to analyse the impacts of indexation on individual ratepayers has found that 2,290 properties will experience a rates decrease and 21,543 will experience a rates increase. However, of those receiving an increase the vast majority will receive only modest increases with 83% increasing by $50 or less. It should be noted this is based on current year rates and before any increase for 2017/2018 is included.

2.5. To ensure ratepayers have adequate information and are well informed, communications for the community and ratepayers will be prepared.

2.6. It is proposed that Council note the impacts of indexation and maintain its current rating strategy.

|

That the report of the Group Manager Rates and Procurement and the Director Financial Services titled ‘Property Valuation Adjustments (Indexation)’ dated 11 May 2017, be received and noted.

|

4. Background

4.1. Pursuant to the Valuation of Land Act 2001 the Valuer-General is required to revalue each municipal area within a seven year period. Following consultation with State and local government, a six-year cycle has been agreed for Tasmania with one-third of councils being revalued every two years.

4.2. The last Hobart municipal revaluation was effective 1 July 2015. The next revaluation will be effective from 1 July 2021.

4.3. In 2007 market-based adjustment factors (also called ‘indexation’) were introduced as a mechanism to index property values and minimise large fluctuations to valuations that can occur between the six-yearly revaluation cycle.

4.4. Currently, adjustment factors are determined annually for Land Value and every two years for Assessed Annual Value (AAV) and Capital Value (CV). The Office of the Valuer-General (OVG) determines these adjustment factors by considering changes in rental market conditions.

4.5. AAV adjustment factors are used by councils to calculate rates and charges and apply for a two year period. An adjustment factor is not a revaluation of an individual property. It is a factor that is used to adjust the levels of value of all property in a locality and class, based on broad market movements.

4.6. Adjustment factors help to ensure that property values more closely reflect changes in the property market. In this way the relative rate burden keeps up with changes in real estate market fluctuations which affect property values and rentals and ultimately Council rates and charges.

4.7. It should be noted that although indexation is designed to minimise large fluctuations to property values between revaluations, shifts are still likely when a revaluation is performed.

4.8. Council last received indexation data in 2013. In 2015, as indicated above, there was a revaluation.

4.9. Council has recently received preliminary AAV adjustment factor data for the Hobart municipal area from the OVG. Final data will be provided to Council in June 2017. The AAV adjustment factors are to take effect from 1 July 2017.

5. Outcomes

5.1. The AAV adjustment factors (excluding vacant land) for the Hobart municipal area are shown in the table below.

|

Valuation District |

Locality |

Non-Vacant Land Class |

|||||

|

|

|

Residential |

Commercial |

Industrial |

Primary Production |

Community Services |

Other |

|

Hobart |

All |

1.05 |

1.00 |

1.00 |

1.10 |

1.00 |

1.00 |

5.1.1. The class of ‘Other’ includes those properties classed as sport & recreation and quarry & mining.

5.1.2. As can be seen from the table above, there is an adjustment factor of 1.05 for residential properties in the Hobart municipal area. This means that all properties in the Hobart municipal area classed as residential will experience a 5% increase in AAVs.

5.1.3. There is an adjustment factor of 1.10 for primary production properties in the Hobart municipal area. This means that all properties in the Hobart municipal area classed as primary production will experience a 10% increase in AAVs. There are only four properties with this classification.

5.1.4. There is one adjustment factor of 1.00 for all properties in the Hobart municipal area classed as commercial, industrial, community services and other. This means there will be no change to the current AAVs for properties classed as commercial, industrial, community services and other.

5.1.5. Over the last two years Hobart’s commercial sector has remained generally static but the residential sector has experienced growth. These factors impact the rental value of these properties and therefore their AAVs.

5.2. The AAV adjustment factors for all classes of vacant land in the Hobart municipal area are shown in the table below.

|

Valuation District |

Locality |

Vacant Land Class |

|||||

|

|

|

Residential |

Commercial |

Industrial |

Primary Production |

Community Services |

Other |

|

Hobart |

All |

1.10 |

1.10 |

1.10 |

1.10 |

1.10 |

1.10 |

5.2.1. There is one adjustment factor of 1.10 for all properties in the Hobart municipal area classed as vacant land. This means that all vacant land in the Hobart municipal area will experience an increase in AAVs of 10%.

5.3. A brochure from the OVG containing more information on the methodology for arriving at adjustment factors is attached for information – refer Attachment A.

5.4. The effect of lower indexation factors for non-residential properties than for residential properties is a shift in the rate burden from non-residential to residential. Residential AAV currently represents 53% of total municipal AAV. Following indexation, the preliminary results show that residential AAV will represent 54.1% of total municipal AAV, a 1.1% increase. Accordingly, residential ratepayers will pay proportionally more in rates.

5.5. Based on the preliminary data received from the OVG, the total AAV for the municipality will increase by approximately 2.79% from $805.5M to $828M.

5.6. To demonstrate the impact, rates modelling has been undertaken of the impact of indexation on the current i.e. 2016/17 rate burden and rates paid by individual ratepayers. It should be noted that this analysis does not factor in the impact of the proposed 2017/18 rate increase or any other matters that may affect the rate base.

5.7. The outcome on a % and $ variance is shown in the table overleaf:

|

Export EasyRev |

||

|

Ranges: Analysis: All Assessments: % and $ variance |

||

|

2 Curr Levies 17/18 Indexed AAV |

||

|

K. -10% to <0% Total |

2289 |

|

|

|

A. <-1000 |

136 |

|

|

B. -1000 to <-800 |

25 |

|

C. -800 to <-600 |

45 |

|

|

D. -600 to <-400 |

111 |

|

|

E. -400 to <-200 |

335 |

|

|

F. -200 to <0 |

1637 |

|

|

L. 0% to <0% Total |

370 |

|

|

|

G. 0 to <0 |

369 |

|

|

H. 0 to <200 |

1 |

|

M. 0% to <10% Total |

21543 |

|

|

|

H. 0 to <200 |

21475 |

|

|

I. 200 to <400 |

43 |

|

J. 400 to <600 |

7 |

|

|

K. 600 to <800 |

6 |

|

|

L. 800 to <1000 |

4 |

|

|

M. 1000 to <1500 |

6 |

|

|

N. 1500 to <3000 |

2 |

|

5.8. Comments on the impact of indexation are as follows:

5.8.1. The properties that have zero impact are mainly Council owned properties that don’t pay rates.

5.8.2. Properties that will experience a reduction in rates are non-residential.

5.8.3. The vast majority of properties paying more will only increase modestly – based on current year rates 83% of those paying more will only increase by $50 or less - noting any rate increase for 17/18 would be additional.

5.8.4. 98% of properties paying up to 10% more in rates will pay <$100 more in rates for 17/18 (noting the budget increase hasn’t been factored in yet).

5.8.5. The properties paying >$200 in rates are properties with high AAVs in Sandy Bay, Battery Point and Hobart. The properties in M and N are independent living unit complexes.

6. Proposal and Implementation

6.1. It is proposed that the Committee note the impacts of the AAV adjustment factors received from the OVG for the 2017/18 rating year and the proposed implementation strategy as follows:

6.1.1. The AAV adjustment factors for all properties will be used to calculate Council rates for the 2017/18 rating year.

6.1.2. The adjusted AAV amount will appear on the front of the annual rates notice.

6.1.3. A flyer explaining indexation and the adjusted AAV values will accompany the annual rates notice to explain indexation.

6.1.4. Information about indexation and its impacts will be included in the June edition of Capital City News and on Council’s website.

6.1.5. Briefing materials will be prepared for relevant Council Officers so customer enquiries can be handled effectively.

6.2. Although there are tools available under the Local Government Act 1993 (LG Act) to mitigate the redistribute effects of indexation, Council at its meeting on 21 March 2016 resolved to continue with its current rating and valuation strategy.

6.3. Indexation has affected how the rating burden is distributed amongst property owners. It has meant that some properties will pay more in rates than previously and some properties will pay less. Council has in the past determined that it is fair and equitable that the valuation system, which is influenced by property sales and market information as well as legislative requirements, influences the rates distribution.

6.4. It is therefore proposed that Council maintains its current rating and valuation strategy.

7. Strategic Planning and Policy Considerations

7.1. This report relates to priority area of activity five, Governance, in the City of Hobart Capital City Strategic Plan 2015-2025.

7.1.1. Strategic objective 5.1.8 – ensure a rating system that supports fairness, capacity to pay and effectiveness.

7.2. Ensuring a municipal area rating and valuation strategy that addresses the following is an important part of organisational sustainability:

7.2.1. The principles of taxation outlined in section 86A(1) of the LG Act.

7.2.2. The objectives, strategies and actions outlined in Council’s Strategic Plan, Annual Plan and Long-term Financial Management Plan.

7.2.3. The needs and expectations of the general community.

7.2.4. The level of the cost of maintaining existing facilities and necessary services.

7.2.5. The need for additional facilities and services.

7.3. Council’s current rating and valuation strategy is outlined in the City of Hobart Rates and Charges Policy.

8. Financial Implications

8.1. Funding Source and Impact on Current Year Operating Result

8.1.1. There are no impacts on the current year operating result.

8.2. Impact on Future Years’ Financial Result

8.2.1. There are no direct financial implications for Council.

8.2.2. Council sets its budget annually to ensure it raises the budgeted amount required. The rate in the dollar is calculated by dividing the amount of money Council needs to raise in its budget by the total $AAV of all rateable properties in the Hobart municipality. Where the total municipal $AAV is less the rate in the dollar will be higher and vice versa.

8.2.3. The rate in the dollar is then multiplied by the value of a property, using the AAV, to establish the amount to be paid by each property owner.

8.2.4. Valuations do not determine the rates income of a Council and as a result, Councils do not gain windfalls from valuation increases or shortfalls from valuation decreases.

8.3. Asset Related Implications

8.3.1. Not applicable.

9. Legal, Risk and Legislative Considerations

9.1. Council’s rating powers are outlined in Part 9 of the LG Act.

9.2. There is a risk of ratepayer concern with rate increases resulting from indexation. Any concerns regarding indexation and the class or locality properties have been assigned can be directed to the Office of the Valuer-General.

10. Social and Customer Considerations

10.1. To ensure ratepayers have adequate information and are well informed, communications for the community and ratepayers will be prepared as detailed in Section 6 above.

11. Community and Stakeholder Engagement

11.1. Communications regarding indexation will be undertaken as described in Section 6 above.

12. Delegation

12.1. This matter is delegated to the Finance Committee.

As signatory to this report, I certify that, pursuant to Section 55(1) of the Local Government Act 1993, I hold no interest, as referred to in Section 49 of the Local Government Act 1993, in matters contained in this report.

|

Lara MacDonell Group Manager Rates and Procurement |

David Spinks Director Financial Services |

Date: 11 May 2017

File Reference: F17/40149; 22-1-3

Attachment a: Brochure

from the Office of the Valuer-General - Property Valuation and Adjustment

Factors ⇩ ![]()

|

Agenda (Open Portion) Finance Committee Meeting |

Page 30 |

|

|

|

16/5/2017 |

|

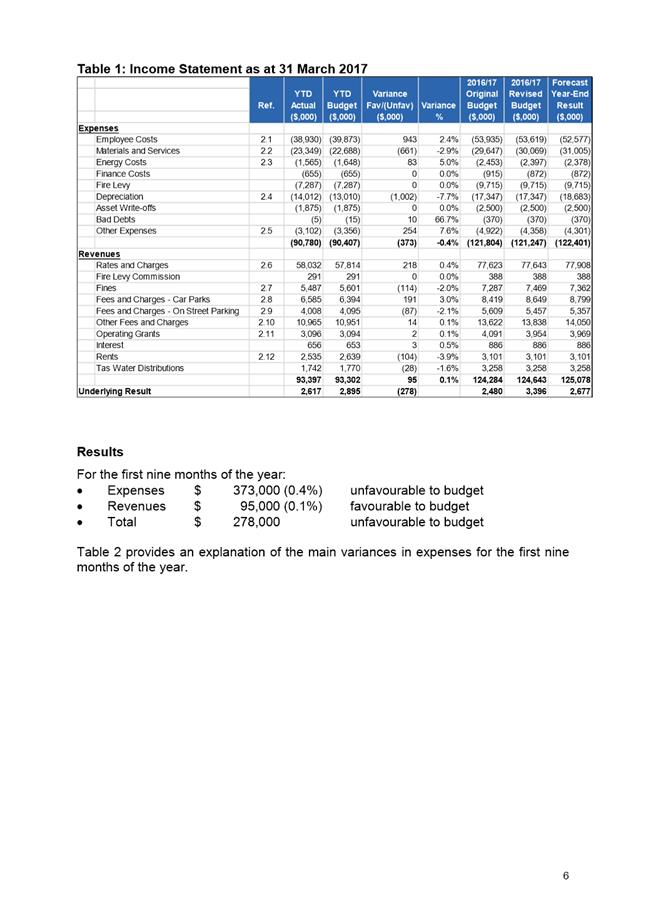

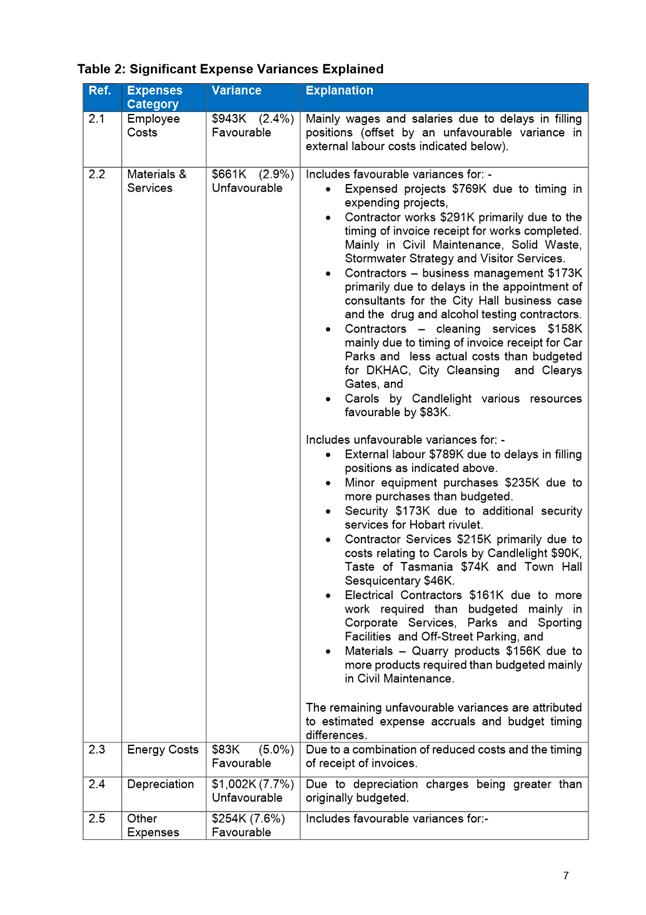

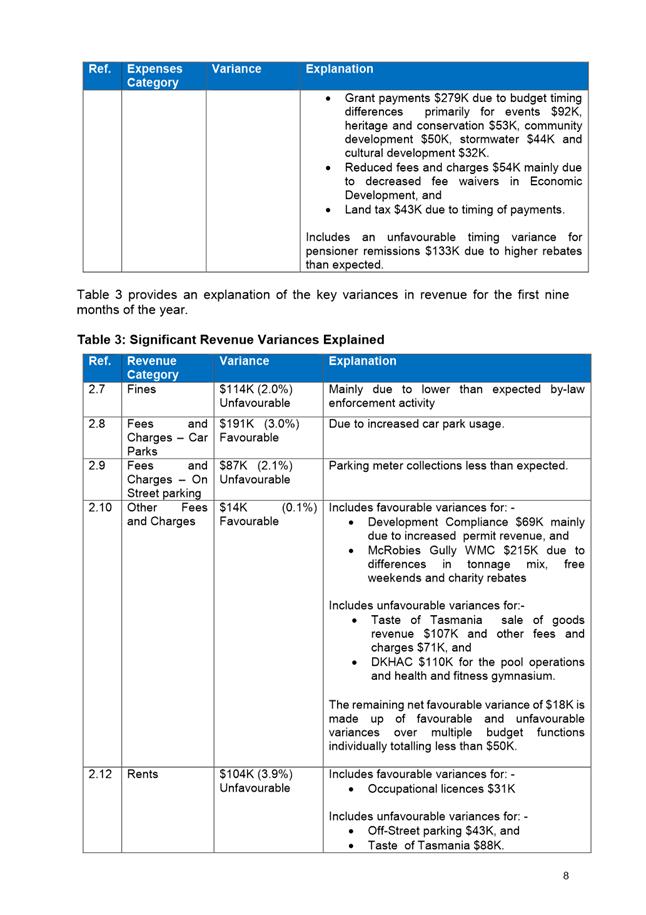

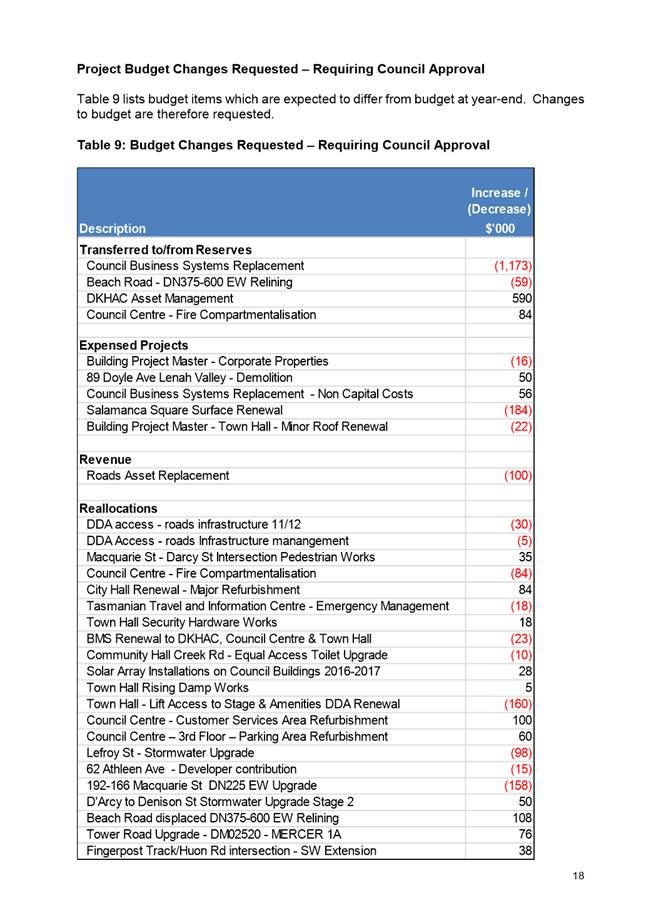

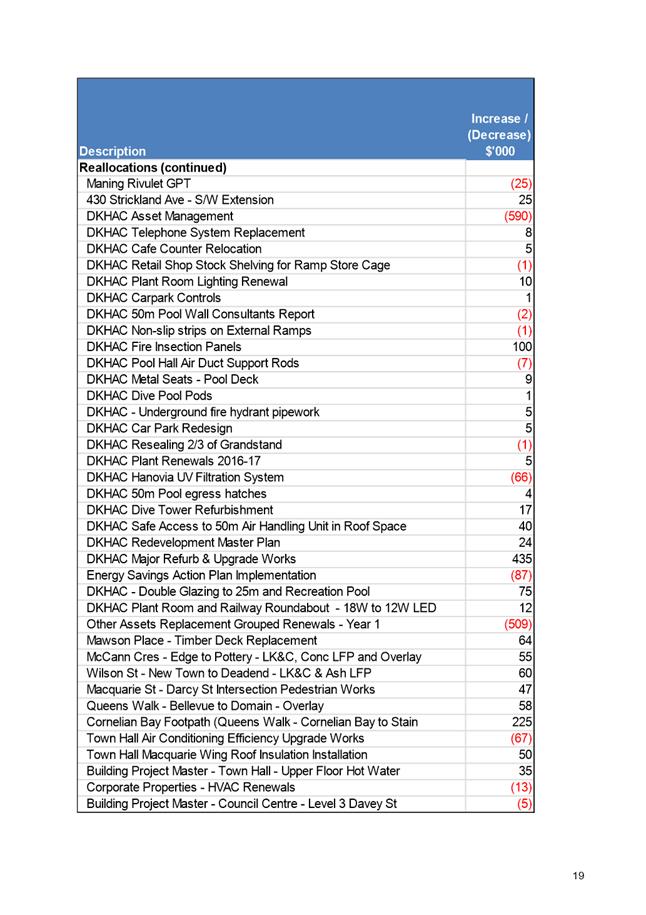

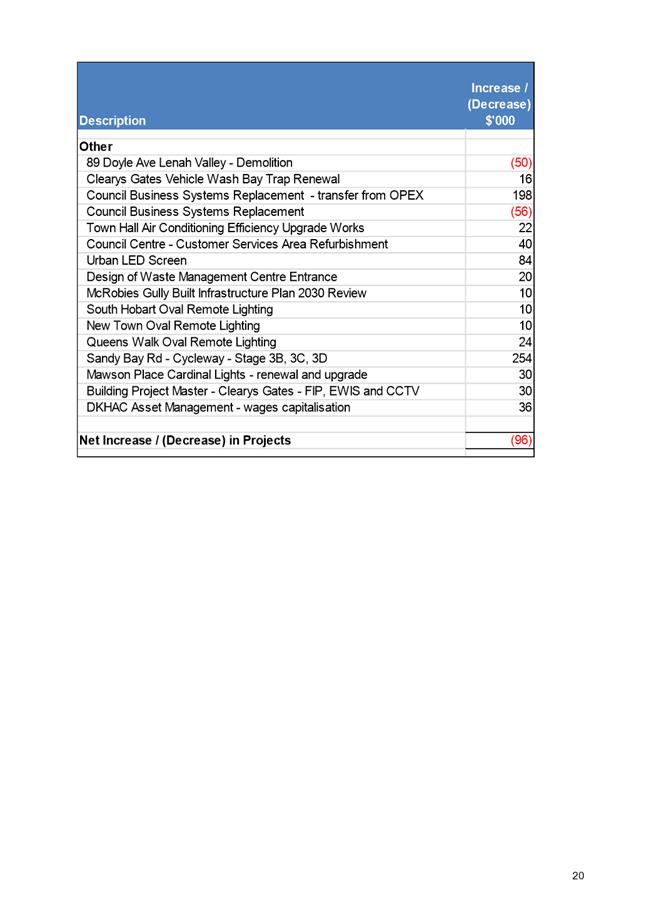

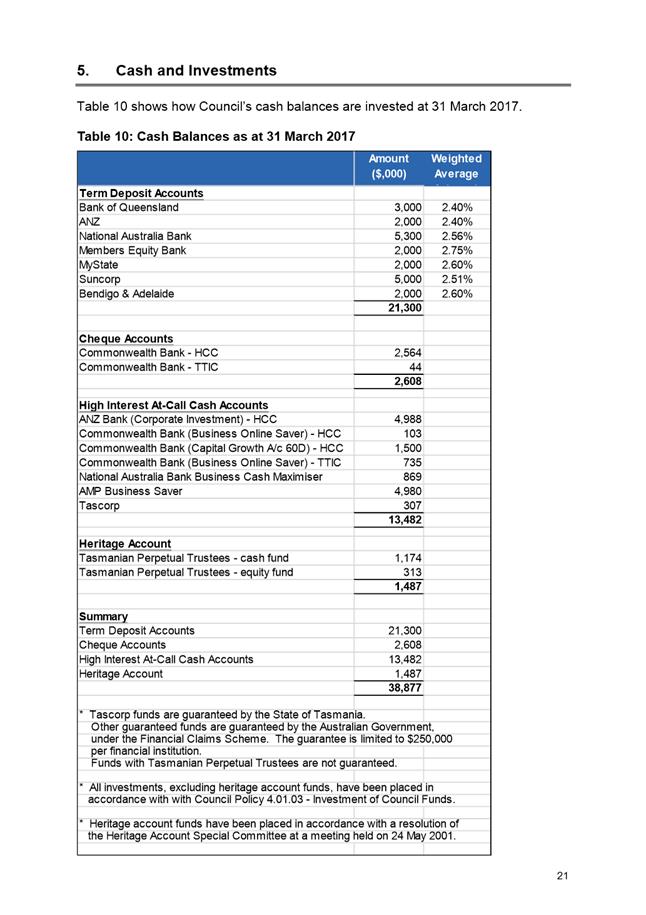

6.3 Financial Report as at 31 March 2017

File Ref: F17/45199; 21-1-1

Report of the Budget and Reporting Manager and the Director Financial Services of 11 May 2017 and attachment.

Delegation: Council

|

Item No. 6.3 |

Agenda (Open Portion) Finance Committee Meeting |

Page 32 |

|

|

16/5/2017 |

|

REPORT TITLE: Financial Report as at 31 March 2017

REPORT PROVIDED BY: Budget and Reporting Manager

Director Financial Services

1. Report Purpose and Community Benefit

1.1. The purpose of this report is to present Council’s Financial Report for the period ending 31 March 2017, and to seek approval for changes to the 2016-2017 Estimates (budget).

2. Report Summary

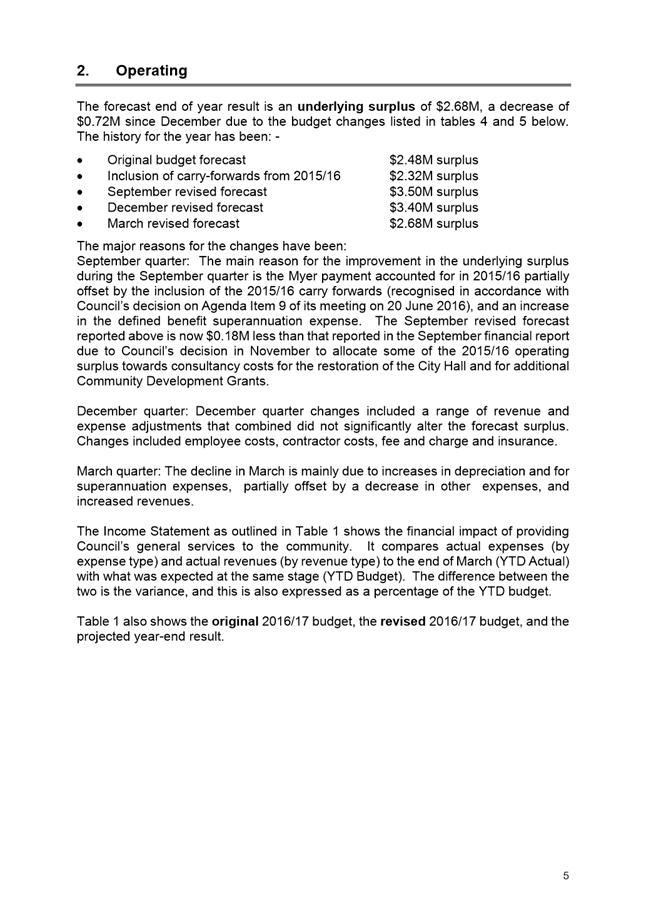

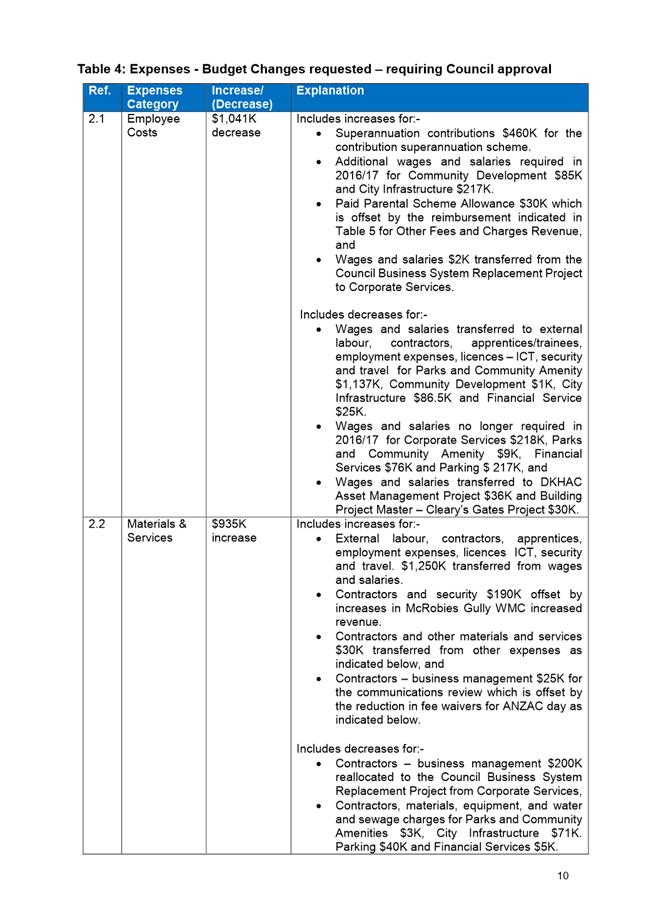

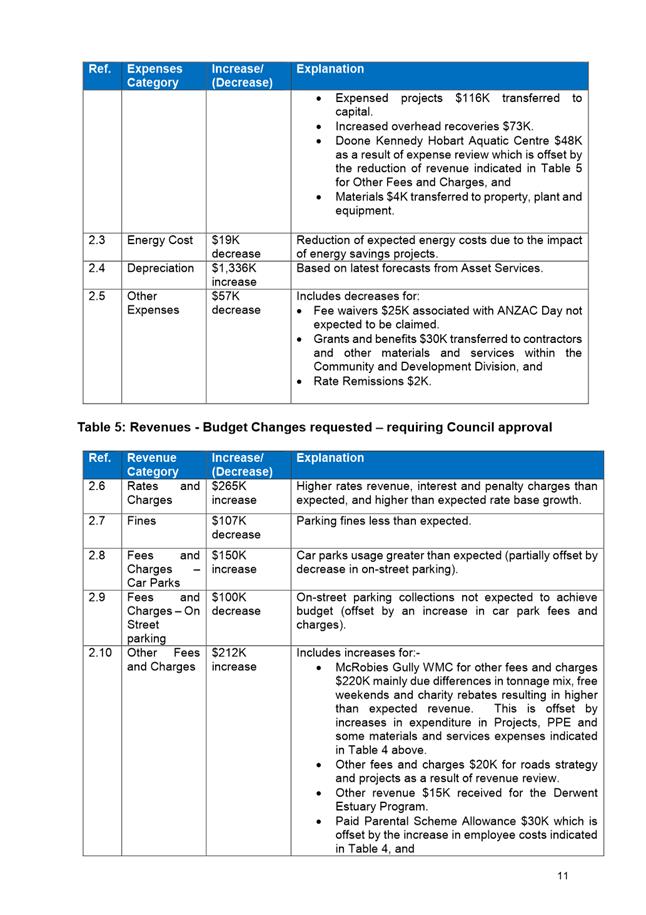

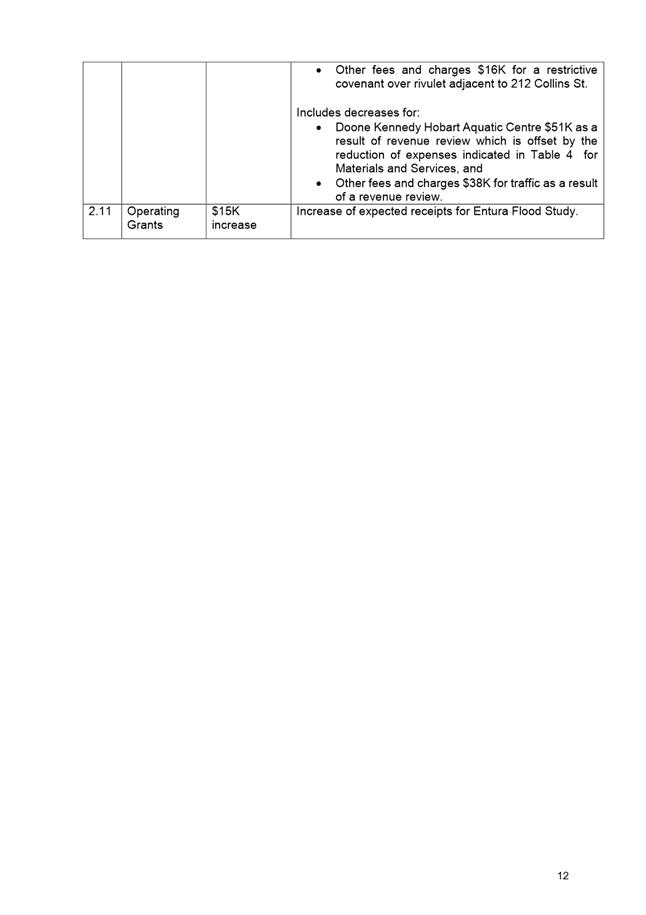

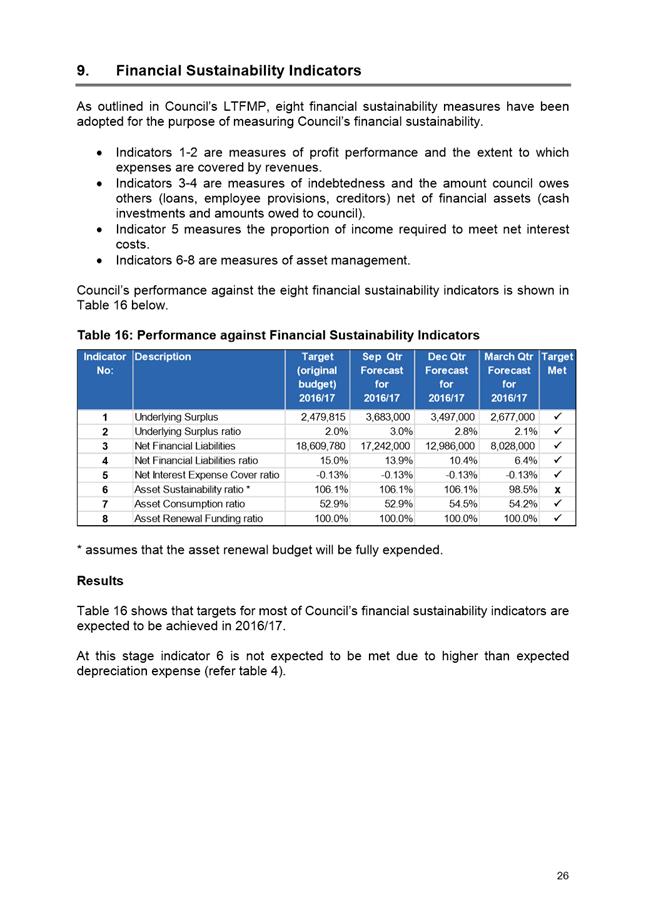

2.1. The Financial Report for the period ending 31 March 2017 is presented for consideration. It shows that expenses are currently unfavourable and revenues are marginally favourable when compared to budget, and forecasts the following financial outcomes for 2016/2017:

· An underlying surplus of $2.68M;

· A closing cash balance of around $30M; and

· The achievement of targets set for most of the Council’s eight financial sustainability indicators.

2.2. The Council remains in a strong, sustainable financial position.

|

That the Council approve the changes to the 2016/2017 Estimates listed in tables 4, 5, 7 and 9 of Attachment A, noting that the financial impacts of which are to decrease the underlying surplus by $0.72M, and to increase the cash balance by $0.91M. |

4. Background

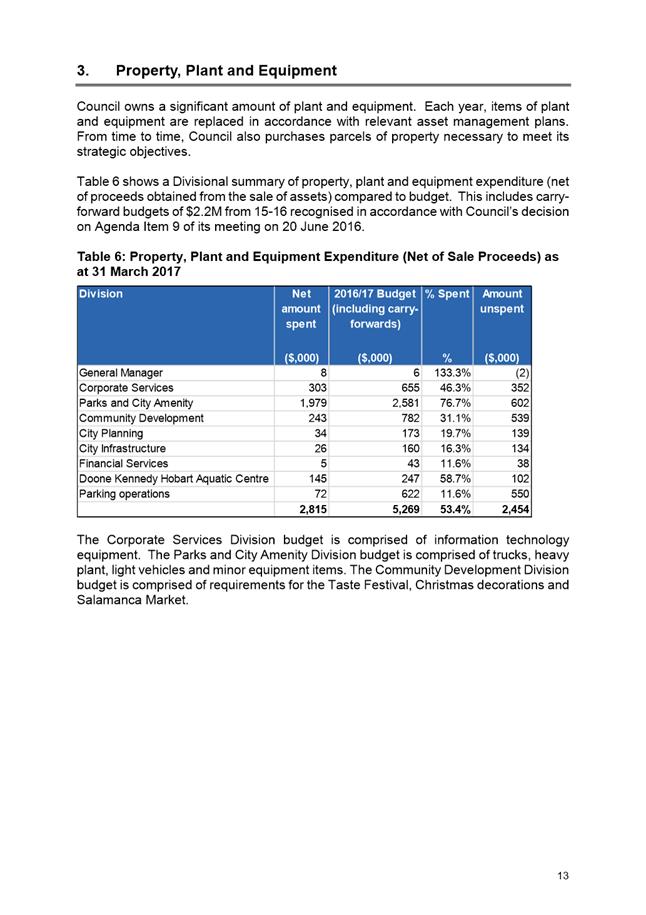

4.1. The Financial Report as at 31 March 2017 is provided at Attachment A. The Financial Report provides details of:

· The Council’s financial position as at 31 March 2017;

· The result of operations for the first nine months of the 2016-2017 financial year;

· Forecasts for 30 June 2017; and

· Progress towards the achievement of the Council’s financial sustainability outcomes.

4.2. In accordance with the Council’s decision on item 9 at its meeting on 20 June 2016, the Council approved the carry-forward of unspent operating grants which resulted in the forecast underlying surplus for 2016-2017 reducing by $0.16M, from $2.48M to $2.32M.

4.3. Council approved further changes to the Estimates as part of the financial report for the period ending 30 September 2016 which resulted in the forecast underlying surplus for 2016-2017 improving by $1.18M, from $2.32M to $3.50M.

4.4. Council approved further changes to the Estimates as part of the financial report for the period ending 31 December 2016 which resulted in the forecast underlying surplus for 2016-2017 remaining unchanged at $3.40M.

5. Proposal and Implementation

5.1. The Financial Report seeks to have the 2016-2017 estimates (budget) amended to take account of expected differences from budget at 30 June 2017 (permanent variances).

5.2. It is proposed that the Council approve changes to the 2016-2017 Estimates as set out in tables 4, 5, 7 and 9 of Attachment A.

6. Strategic Planning and Policy Considerations

Goal 5 – Governance is applicable in considering this report, particularly

Strategic 5.1 objective:

“The organisation is relevant to the community and provides good governance and transparent decision-making”.

7. Financial Implications

7.1. Funding Source Impact on Current Year Operating Result

7.1.1. The proposed changes to the Estimates will result in net expenditure decreasing (and the forecast cash balance increasing) by $0.91M.

7.1.2. The increase in the forecast cash balance results from a number of factors, the main one being the decrease in net operating expenditure.

7.1.3. The final cash balance may differ from the current forecast for the following reasons:

· Current budget variances which are assumed to be timing variances (and therefore forecasts have not been amended) may prove to be permanent variances;

· Further variances could arise during the remainder of the year; and

· Capital expenditure could be higher or lower than forecast.

7.2. Impact on Current Year Operating Result

7.2.1. The impact of the proposed changes to the Estimates is to decrease the forecast underlying surplus by $0.72M (from $3.40M to $2.68M).

7.2.2. Whilst an underlying surplus of $2.68M is currently forecast for 2016-2017, expenses are currently unfavourable when compared to budget, and revenues are only marginally favourable. If this position continues, the final result will vary from the current forecast.

7.2.3. The final operating result may differ from the current forecast for the following reasons:

· Current budget variances which are assumed to be timing variances (and therefore forecasts have not been amended) may prove to be permanent variances; and

· Further variances could arise during the remainder of the year.

7.3. Impact on Future Years’ Financial Result

7.3.1. The impact on future years’ underlying results is difficult to estimate reliably because some changes may be ongoing, whilst others may not.

7.4. Asset Related Implications

7.4.1. No significant asset related implications are anticipated.

7.5. Financial Sustainability Indicators

7.5.1. Targets set for seven of the Council’s eight financial sustainability indicators are expected to be achieved in 2016-2017. The target for the Asset Sustainability ratio is not expected to be achieved due to higher than expected depreciation expense.

8. Legal, Risk and Legislative Considerations

8.1. Not Applicable.

9. Delegation

9.1. This matter is delegated to the Council.

As signatory to this report, I certify that, pursuant to Section 55(1) of the Local Government Act 1993, I hold no interest, as referred to in Section 49 of the Local Government Act 1993, in matters contained in this report.

|

Karelyn Stephens Budget and Reporting Manager |

David Spinks Director Financial Services |

Date: 11 May 2017

File Reference: F17/45199; 21-1-1

Attachment a: Financial

Report Ending March 2017 ⇩ ![]()

|

Agenda (Open Portion) Finance Committee Meeting |

Page 62 |

|

|

|

16/5/2017 |

|

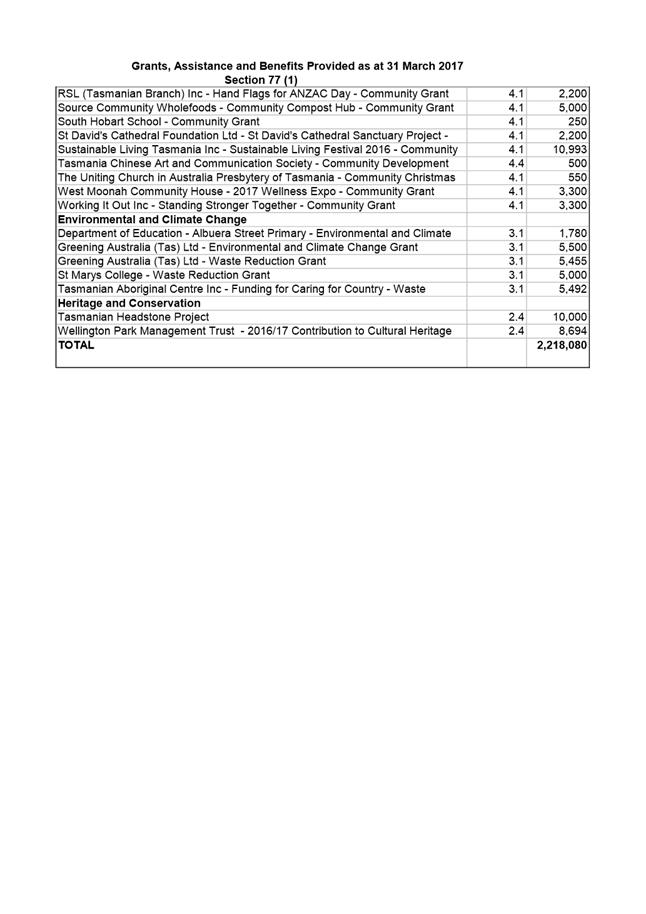

6.4 Grants and Benefits Listing as at 31 March 2017

File Ref: F17/40124; 25-2-1

Report of the Group Manager Rates and Procurement and the Director Financial Services of 11 May 2017 and attachments.

Delegation: Committee

|

Item No. 6.4 |

Agenda (Open Portion) Finance Committee Meeting |

Page 64 |

|

|

16/5/2017 |

|

REPORT TITLE: Grants and Benefits Listing as at 31 March 2017

REPORT PROVIDED BY: Group Manager Rates and Procurement

Director Financial Services

1. Report Purpose and Community Benefit

1.1. The purpose of this report is to provide a listing of the grants and benefits provided by the Council for the period 1 July 2016 to 31 March 2017 as requested by the then Parks and Customer Services Committee.

2. Report Summary

2.1. At its meeting on 12 February 2015, the then Parks and Customer Services Committee requested that a quarterly report be provided for the information of the then Finance and Corporate Services Committee outlining all grants and benefits provided by Council Committees and Council.

2.2. A report is attached being for the period 1 July 2016 to 31 March 2017.

2.3. It is proposed that the Committee note the listing of grants and benefits provided for the period 1 July 2016 to 31 March 2017 and that these are required, pursuant to Section 77 of the Local Government Act 1993 (LG Act), to be included in the annual report of Council.

|

That the Finance Committee receive and note the information contained in the report titled “Grants and Benefits Listing as at 31 March 2017”.

|

4. Background

4.1. At its meeting on 12 February 2015, the then Parks and Customer Services Committee resolved that:

4.1.1. A quarterly report be provided for the information of the [then] Finance and Corporate Services Committee outlining all grants and benefits approved by Council Committees and Council.

4.2. At its meeting on 19 May 2015, the Finance Committee resolved that:

4.2.1. Details of all grants and benefits provided under Section 77 of the Local Government Act 1993 be listed on the City of Hobart’s website.

4.3. A report outlining the grants and benefits provided for the period 1 July 2016 to 31 March 2017 is attached – refer Attachment A.

4.4. Pursuant to Section 77 of the LG Act, the details of any grant made or benefit provided will be included in the annual report of the Council.

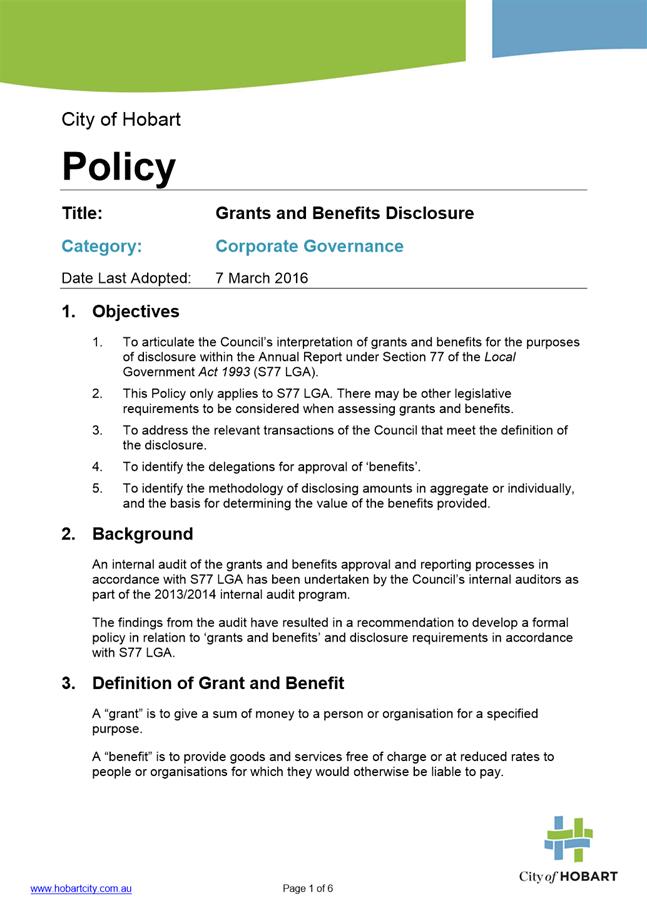

4.5. The listing of grants and benefits marked as Attachment A, has been prepared in accordance with the Council policy titled Grants and Benefits Disclosure – refer Attachment B.

5. Proposal and Implementation

5.1. It is proposed that the Committee note the grants and benefits listing as at 31 March 2017.

5.2. It is also proposed that the Committee note that the grants and benefits listed are required to be included in the annual report of the Council and will be listed on the City of Hobart’s website.

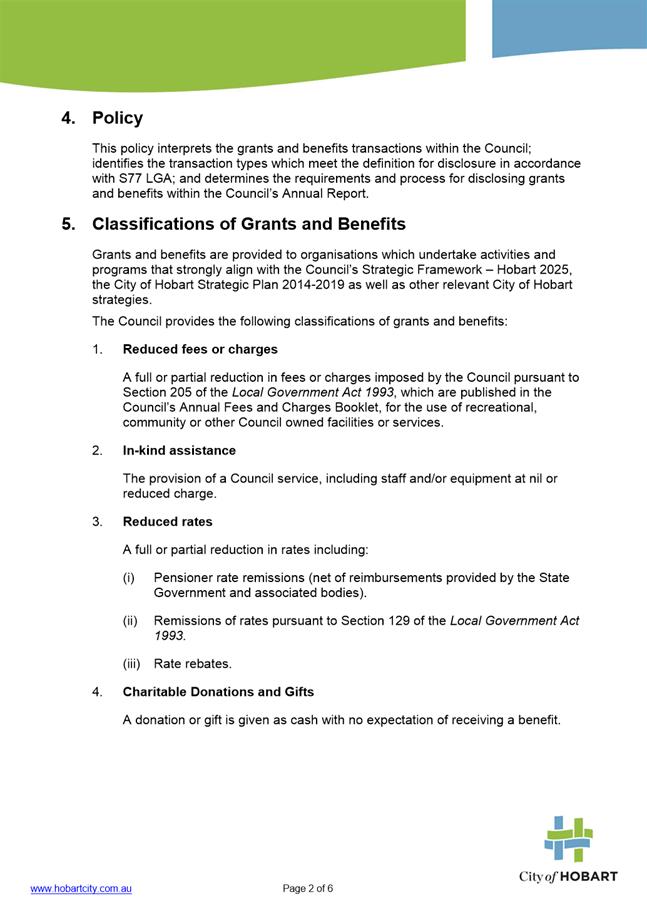

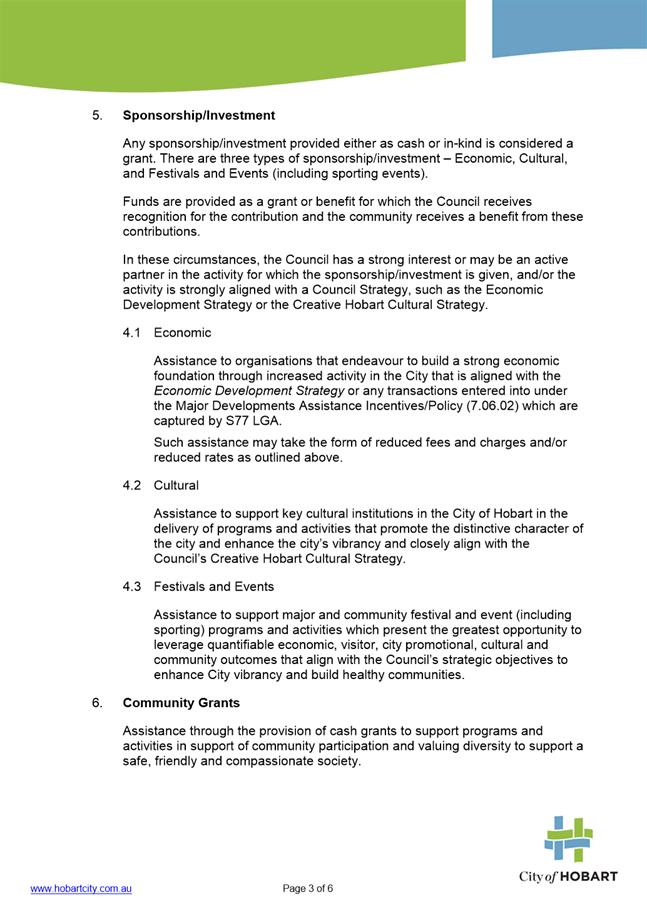

6. Strategic Planning and Policy Considerations

6.1. Grants and benefits are provided to organisations which undertake activities and programs that strongly align with the Council’s Strategic Framework – Hobart 2025, the City of Hobart Capital City Strategic Plan 2015-2025 as well as other relevant City of Hobart strategies.

6.2. The linkage between the City’s grants and benefits provided and the City of Hobart Capital City Strategic Plan 2015-2025 is referenced in Attachment A.

7. Financial Implications

7.1. Funding Source and Impact on Current Year Operating Result

7.1.1. All grants and benefits provided as at 31 March 2017 were funded from the 2016/17 budget estimates.

8. Legal, Risk and Legislative Considerations

8.1. The Council provides grants and benefits within the requirements of Section 77 of the LG Act as follows:

Grants and benefits

(1) A council may make a grant or provide a pecuniary benefit or a non-pecuniary benefit that is not a legal entitlement to any person, other than a councillor, for any purpose it considers appropriate.

(1A) A benefit provided under

subsection (1) may include –

(a) in-kind assistance; and

(b) fully or partially reduced fees, rates or charges;

and

(c) remission of rates or charges under Part 9 (rates

and charges)

(2) The details of any grant made or benefit provided are to be included in the annual report of the Council.

8.2. Section 72 of the LG Act requires the Council to produce an Annual Report with Section 77 of the LG Act providing an additional requirement where individual particulars of each grant or benefit given by the Council must be recorded in the Annual Report.

8.3. Section 207 of the LG Act provides for the remitting of all or part of any fee or charge paid or payable.

8.4. Section 129 of the LG Act provides for the remitting of rates.

9. Delegation

9.1. This report is provided to the Finance Committee for information.

As signatory to this report, I certify that, pursuant to Section 55(1) of the Local Government Act 1993, I hold no interest, as referred to in Section 49 of the Local Government Act 1993, in matters contained in this report.

|

Lara MacDonell Group Manager Rates and Procurement |

David Spinks Director Financial Services |

Date: 11 May 2017

File Reference: F17/40124; 25-2-1

Attachment a: Grants

and Benefits Listing as at 31 March 2017 ⇩ ![]()

Attachment

b: Council

Policy Grants and Benefits Disclosure ⇩ ![]()

|

Agenda (Open Portion) Finance Committee Meeting |

Page 76 |

|

|

|

16/5/2017 |

|

6.5 Write-Off of Debts - Further Information

File Ref: F17/37543

Memorandum of the Manager Finance of 11 May 2017.

Delegation: Committee

|

Item No. 6.5 |

Agenda (Open Portion) Finance Committee Meeting |

Page 78 |

|

|

16/5/2017 |

|

Memorandum: Finance Committee

Write-Off of Debts - Further Information

Management submitted a report for information to the Finance Committee meeting on 21 March 2017 detailing customer debts that had been deemed non-recoverable and written off in accordance with section 76(2) of the Local Government Act 1993 under the General Manager’s delegation.

At the Finance Committee meeting there was a request for further information regarding the ability of Council to recover the debts.

Council policy regarding sundry debts is contained within the policy ‘Collection and Reporting of Outstanding Sundry Debts’. This policy provides that Council’s standard invoice term is 30 days for payment from the invoice date (there are some exceptions to this) and that overdue debts may be provided with a statement, a final notice and referral to Council’s debt collection agency, at the discretion of the Director Financial Services.

The Local Government Act 1993 contains requirements in relation to the writing off of bad debts. Section 76 provides:

(1) A council may write off any debts owed to the council –

(a) if there are no reasonable prospects of recovering the debt; or

(b) if the costs of recovery are likely to equal or exceed the amount to be recovered.

(2) A council must not write off a debt unless the general manager has certified –

(a) that reasonable attempts have been made to recover the debt; or

(b) that the costs of recovery are likely to equal or exceed the amount to be recovered.

Management apply a standard process for recovery of debts that reach a certain age past their due dates. Both the prospect of recovery and the size of the overdue debt determines how far through the process management progresses the debt ie: some debts reach a point where it is more costly to continue pursuing recovery of the debts than the amount to be recovered. That process and the associated external cost is detailed below:

|

Debt Age |

Action |

|

30 days old |

Debtor is sent a statement |

|

60 days old |

Debtor is sent a final notice if the debt is greater than $500 - Final Notice gives the debtor 10 days in which to pay their debts - If no payment, a minimum of 3 attempts are made to contact the debtor and applicable staff from the Division from which the debt originates are advised of the pending lodgement of the debt with the collection service - Debt is lodged with collection agency - Collection agency pursues debtor - If no success with collection agency, agency will advise the likelihood of recovery and recommend any legal action - If legal action is proposed, the cost of a Claim is $300 per debt. To proceed to Judgment/Warrant, costs an additional $400.00. To proceed to lodge a caveat over property which Council does not currently do, costs $650.

Where the debt is less than $500, it is referred to the originating Division for follow up on the basis Divisions have the relationship with the debtor. - Divisions attempt to contact debtor and seek payment of debt - If no success, the debt is lodged with the collection agency.

|

|

90 days and more old |

These debts will be with the collection agency.

If advised by the collection agency that the debt is not recoverable the following occurs: - Debts under $5,000 are referred to the General Manager for approval to write off under delegation. - Debts over $5,000 are referred to Finance Committee for approval to write off. Debts over $10,000 require Council approval to write off. |

The result of this process has seen very low rates of write off relative to revenue invoiced:

|

Year |

Revenue invoiced * |

Write Off |

% Write Off |

|

2013/2014 |

$33,110,000 |

$16,311.68 |

0.05% |

|

2014/2015 |

$32,169,000 |

$4,882.09 |

0.02% |

|

2015/2016 |

$34,742,000 |

$2,527.72 |

0.01% |

|

2016/2017 (Feb) |

$24,427,000 |

$6,363.61 |

0.03% |

* Excludes rates revenue, grant revenue, dividends, interest and rental revenue

|

That the information contained in the memorandum of the Manager Finance dated 11 May 2017 titled “Write-Off of Debts – Further Information” be received and noted.

|

As signatory to this report, I certify that, pursuant to Section 55(1) of the Local Government Act 1993, I hold no interest, as referred to in Section 49 of the Local Government Act 1993, in matters contained in this report.

|

Fiona Dixon Manager Finance |

|

Date: 11 May 2017

File Reference: F17/37543

|

Item No. 6.6 |

Agenda (Open Portion) Finance Committee Meeting |

Page 80 |

|

|

16/5/2017 |

|

6.6 2017/2018 Fees and Charges - Financial Services

File Ref: F17/40136; P16/33

Report of the Group Manager Rates and Procurement and the Director Financial Services of 11 May 2017 and attachment.

Delegation: Council

|

Item No. 6.6 |

Agenda (Open Portion) Finance Committee Meeting |

Page 82 |

|

|

16/5/2017 |

|

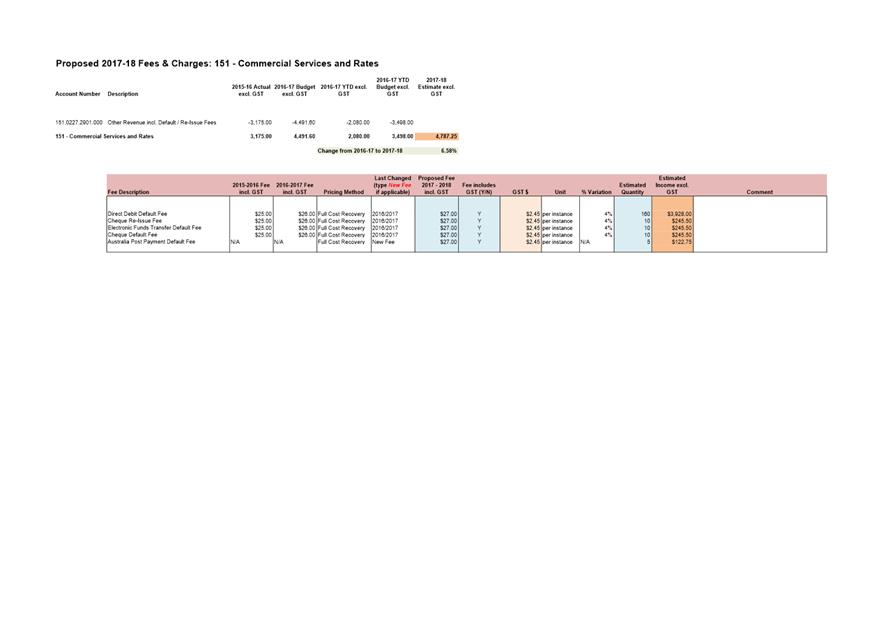

REPORT TITLE: 2017/2018 Fees and Charges - Financial Services

REPORT PROVIDED BY: Group Manager Rates and Procurement

Director Financial Services

1. Report Purpose and Community Benefit

1.1. The purpose of this report is to:

1.1.1. Present the proposed fees and charges for Council’s financial services for the 2017/2018 financial year, and

1.1.2. Seek approval for a new Council fee proposed for the 2017/2018 financial year.

1.2. Fees and charges are reviewed each year as part of the Council’s annual budget process.

2. Report Summary

2.1. A review of Council’s financial services fees and charges has been undertaken and a rounded 2.5% price increase for each is proposed for 2017/2018.

2.2. A new Council fee is proposed for 2017/2018, being for payment default when making payments at Australia Post.

2.3. It is recommended that the attached schedule of fees and charges is adopted for 2017/2018.

|

That the attached schedule of fees and charges for financial services be adopted for the 2017/2018 financial year.

|

4. Background

4.1. At its meeting on 14 May 2012 Council introduced three new fees, being a direct debit default fee, a cheque re-issue fee and an electronic funds transfer (EFT) default fee.

4.2. The direct debit default fee is charged to a customer where there are insufficient cleared funds in the nominated account when the agreed direct debit payments are to be drawn.

4.3. The cheque re-issue fee is charged when a customer requests Council to re-issue a cheque where the original may have been lost or misplaced. However, the fee is not charged when a cheque is re-issued as a result of a Council error.

4.4. The EFT default fee is charged when an EFT transaction is unsuccessful because the incorrect bank account information was supplied and the EFT is resent by Council as a result.

4.5. At its meeting on 25 May 2015 Council introduced a new fee for the 2015/2016 financial year, being a cheque default fee.

4.6. The cheque default fee is charged when a customer pays by cheque but the cheque is dishonoured by the financial institution e.g. ‘bounced cheque’.

4.7. Similar fees and charges are imposed by councils both in Tasmania and interstate.

4.8. A pricing review of the financial services fees has been undertaken. A schedule showing the proposed fees for 2017/2018 is attached – refer Attachment A.

5. Proposal and Implementation

5.1. It is proposed that the following new fee be introduced at Council for the 2017/2018 financial year.

5.1.1. Australia Post payment default fee.

5.2. The new fee is included in the attached schedule.

5.3. The Australia Post payment default fee is proposed to be charged to a customer who pays at Australia post but the payment defaults. This will usually be because the customer pays by cheque but the cheque is dishonoured by the financial institution.

5.4. It is proposed that the pricing level for the new fee be $27 per instance inclusive of GST, consistent with the pricing level of the other financial service fees and charges. The price reflects the $25 cost charged to Council by Australia Post and a small amount to cover the administrative costs to Council in rectifying the default.

5.5. It is proposed that the attached schedule of fees and charges be adopted for the 2017/2018 financial year.

5.6. The proposed pricing level for each fee includes a 2.5% increase (rounded upwards to the nearest dollar), from 2016/2017 levels, to reflect annual increases in administrative costs and is inclusive of GST.

5.7. The proposed direct debit default fee of $27 includes the transactional banking fee imposed on Council by its financial institution, being $2.50 per instance, and an amount to recover the administrative costs to Council in rectifying this default.

5.8. The proposed cheque re-issue fee of $27 includes the transactional banking fee imposed by Council by its financial institution, being $10 per instance, and an amount to recover the administrative costs to Council in re-issuing a cheque.

5.9. The proposed EFT default fee of $27 includes the transactional banking fee imposed by Council by its financial institution, being $2.50 per instance, and an amount to recover the administrative costs to Council in resending the EFT.

5.10. The proposed cheque default fee of $27 is priced consistently with the other financial service fees and charges. The price also reflects the amount to cover the administrative costs to Council in rectifying the default.

5.11. Fees and charges for 2017/2018 will become effective as at 1 July 2017.

5.12. Pursuant to section 206 of the Local Government Act 1993, the fees will be included in Council’s fees and charges booklet, which is made available to the community from Council’s website and the Customer Service Centre.

6. Strategic Planning and Policy Considerations

6.1. There are no direct strategic planning implications arising from this report.

6.2. The annual review of fees and charges has been undertaken in accordance with Council’s Pricing Policy and Guidelines.

7. Financial Implications

7.1. Funding Source and Impact on Current Year Operating Result

7.1.1. Not applicable.

7.2. Impact on Future Years’ Financial Result

7.2.1. It is difficult to determine the income that will be generated to Council from these fees as they are applied when a payment default has occurred.

7.2.2. Based upon the number of instances where the fees have been applied to date this financial year, it is envisaged that approximately $4,787 will be generated in income from these fees in 2017/2018.

7.3. Asset Related Implications

7.3.1. Not applicable.

8. Legal, Risk and Legislative Considerations

8.1. Pursuant to section 205 of the Local Government Act 1993 (Tas), Council has the following powers:

(1) In addition to any other power to impose fees and charges but subject to subsection (2), a council may impose fees and charges in respect of any one or all of the following matters:

(a) the use of any property or facility owned, controlled, managed or maintained by the council;

(b) services supplied at a person's request;

(c) carrying out work at a person's request;

(d) providing information or materials, or providing copies of, or extracts from, records of the council;

(e) any application to the council;

(f) any licence, permit, registration or authorization granted by the council;

(g) any other prescribed matter.

(2) A council may not impose a fee or charge in respect of a matter if –

(a) a fee or charge is prescribed in respect of that matter; or

(b) this or any other Act provides that a fee or charge is not payable in respect of that matter.

(3) Any fee or charge under subsection (1) need not be fixed by reference to the cost to the council.

8.2. Pursuant to section 206 of the LG Act, council is to keep a list of all fees and charged and make the list available for public inspection during ordinary hours of business.

9. Delegation

9.1. This matter is delegated to the Council.

As signatory to this report, I certify that, pursuant to Section 55(1) of the Local Government Act 1993, I hold no interest, as referred to in Section 49 of the Local Government Act 1993, in matters contained in this report.

|

Lara MacDonell Group Manager Rates and Procurement |

David Spinks Director Financial Services |

Date: 11 May 2017

File Reference: F17/40136; P16/33

Attachment a: Fees

and Charges 2017/2018 Financial Services ⇩ ![]()

|

Agenda (Open Portion) Finance Committee Meeting |

Page 87 |

|

|

|

16/5/2017 |

|

6.7 2017/2018 Fees and Charges - Parking Operations

File Ref: F17/43280

Report of the Group Manager Parking Operations and the Director Financial Services of 11 May 2017 and attachments.

Delegation: Council

|

Item No. 6.7 |

Agenda (Open Portion) Finance Committee Meeting |

Page 89 |

|

|

16/5/2017 |

|

REPORT TITLE: 2017/2018 Fees and Charges - Parking Operations

REPORT PROVIDED BY: Group Manager Parking Operations

Director Financial Services

1. Report Purpose and Community Benefit

1.1. The purpose of this report is to present the proposed fees and charges applicable to the Financial Services Division – Parking Enforcement and Off-Street Parking for the 2017/2018 financial year.

1.2. Fees and charges are reviewed each year as part of the Council’s annual budget process.

2. Report Summary

2.1. A review of Council’s Parking Operations fees and charges has been undertaken and a total increase of 4.98% for all functions within the Parking Operations area is proposed for 2017/2018.

2.2. It is recommended that the attached schedule of fees and charges are adopted for 2017/2018.

.

|

That the schedule of fees and charges for the 2017/2018 financial year, as referenced below and attached to the report, be adopted for the 2017/2018 financial year; 1. Parking Enforcement; 2. Off-Street Parking Long Term; 3. Off-Street Parking Short Term; 4. Off-Street Parking Short Term Motor Bikes; 5. Meters, Voucher Machines and Meter Removal. |

4. Background

4.1. The fees and charges for the 2017/2018 financial year have been assessed including methods and timing of payment. Where possible fees and charges are to be paid up-front with additional costs being charged on a cost recovery basis.

4.2. A summary of the proposed fees and charges follows:

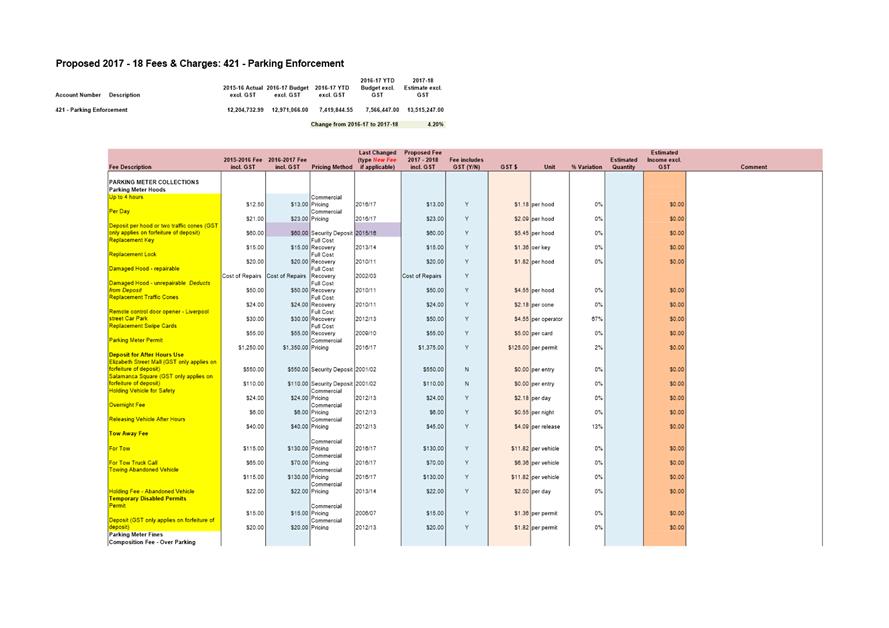

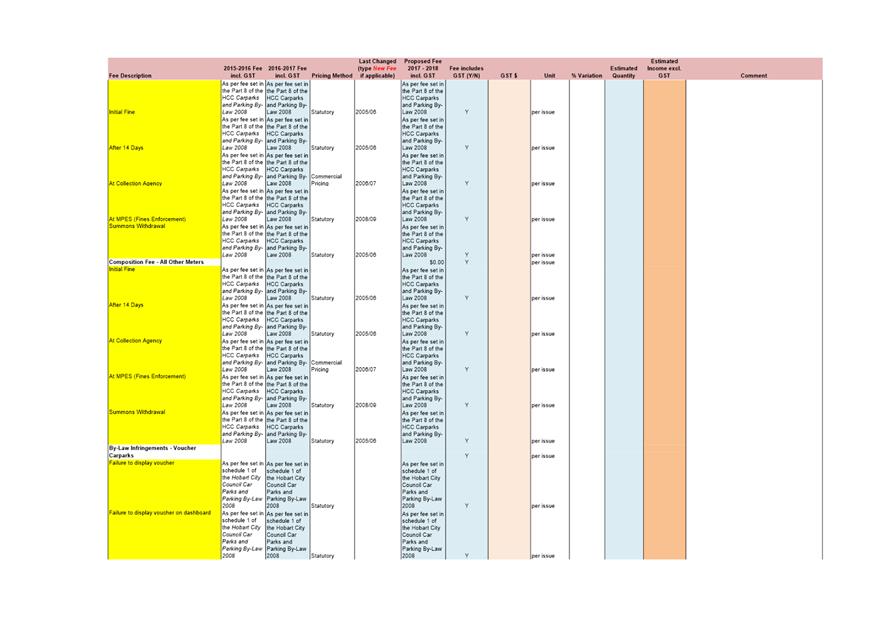

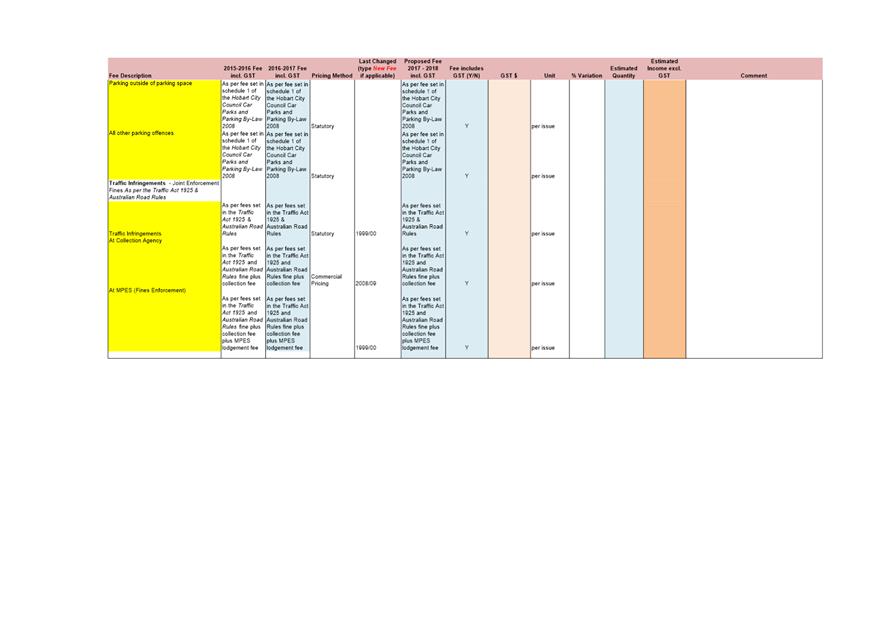

Parking Enforcement

4.2.1. A small fee increase has been applied to parking metered space permit fees. Remote control door openers – Liverpool Street Car Park and Releasing Vehicles after hours have both increased to reflect full cost recovery.

4.2.2. Parking meter fines are aligned to the penalty unit amounts set by State Treasury. Penalty unit fees increased at the beginning of the 2015/2016 and 2016/2017 financial years resulting in an increase in all parking meter fine amounts. The State Government will again increase the penalty unit amount as from the 1 July 2017. As a result parking meter fines will increase by an average of $0.50 per fine. The additional income expected from this increase is estimated at $70K. This amount has been included in the 2017/2018 budget.

4.2.3. Traffic infringement penalties are set by the State Government. Major changes were made to traffic infringement penalty amounts in the 2013/2014 financial year. No changes will be made to the penalties by the State Government in the 2017/2018 financial year.

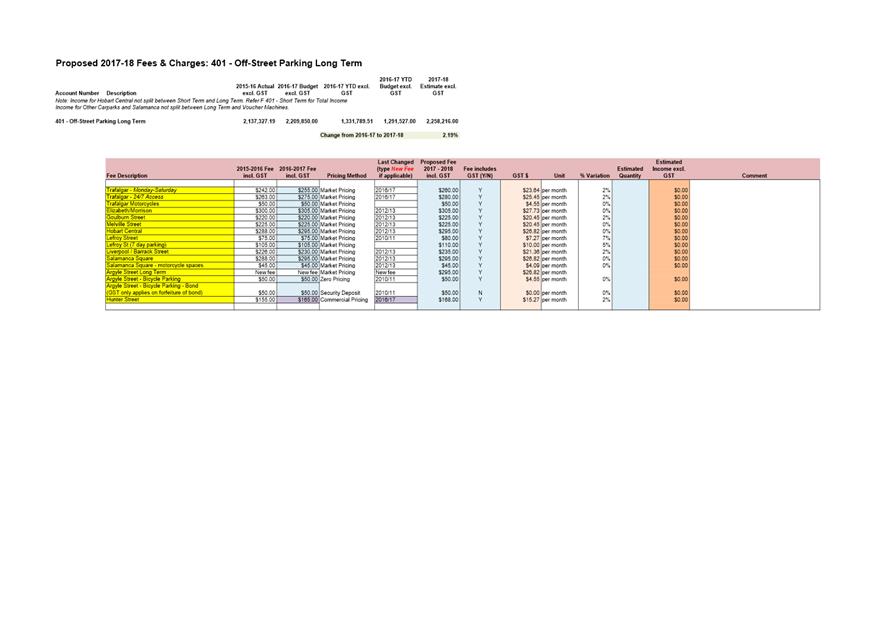

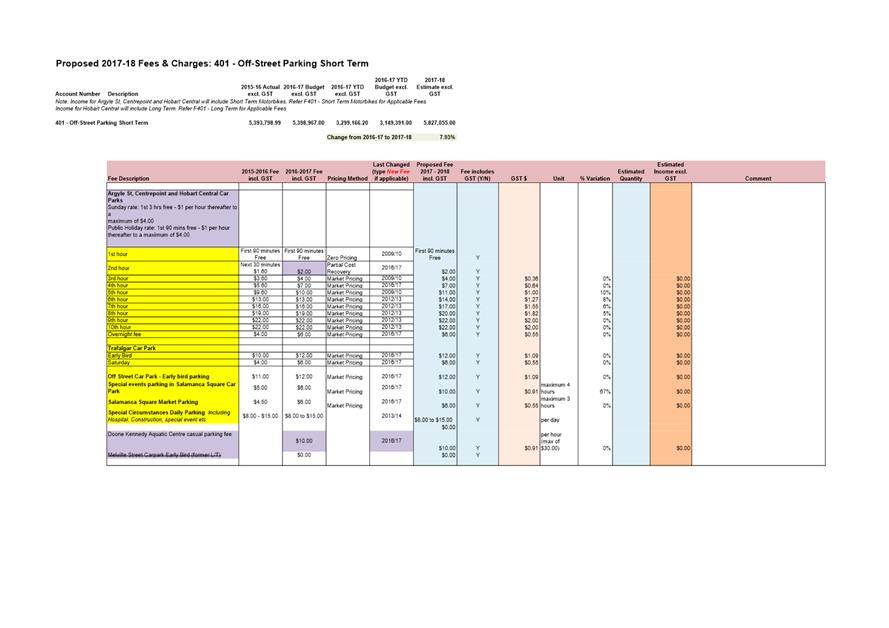

Off-Street Parking, Short and Long Term

4.2.4. Long-term car park fees have been increased in Trafalgar Car Park, Goulburn Street, Lefroy Street and Liverpool/Barrack Street. All remaining long term car parks have not been increased due to vacancies existing in these car parks, and/or no waiting lists. Permit parking for UTAS and Henry Jones IXL Hotel on Hunter Street has increased in line with parking meter rates in that area.

4.2.5. A new fee for long-term parking has been introduced for Argyle Street Car Park of $295.

4.2.6. A $1.00 increase is proposed the 5 hour, 6 hour, 7 hour and 8 hour parking fee for all multi storey car parks. This acts as a further deterrent for vehicle turnarounds and encourages the take up of the proposed long-turn parking noted at 4.2.4.

4.2.7. Early bird rates in Hobart Central, Centrepoint and Trafalgar car parks remain unchanged at $12.00 per day. Early bird fees are reviewed regularly, particularly as changes to on street parking fees, monthly permit fees and fees charged in privately owned car parks have an effect on the overall affordability of parking and the choices customers make. It is important that early bird parking rates are commensurate to other parking rates so as to not encourage exclusive use of early birds as the cheaper or preferred option at the expense of monthly permit parking and matches the rate charged in the privately owned Montpelier Retreat Car Park.

4.2.8. Special event parking rate in Salamanca Square Car Park is proposed to increase from $6.00 to $10.00 for four hours parking. The current rate is no higher than non-special event parking. The change allows for an additional hour parking.

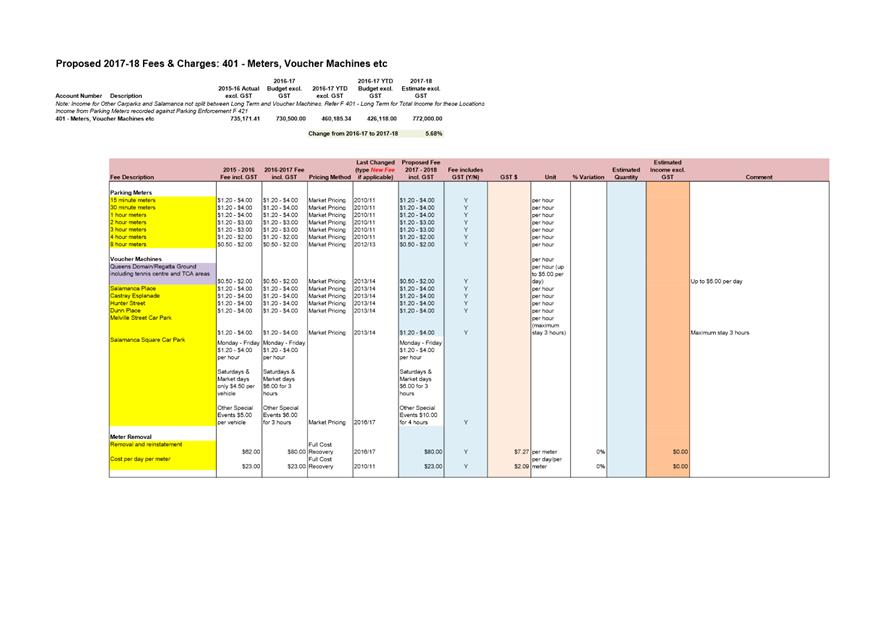

Metres, Voucher Machines

4.2.9. Parking meter fees for Councils 360 multi-bay meters and voucher machines have been reviewed resulting in slight increases to some of the fees In total the parking fees for 280 meters and voucher machines will be increased. These increases will be within the range of fees already reflected in the fees and charges schedule and are in line with actions contained in the Parking Strategy 2013 – 2017 (Actions 1,10 & 27).

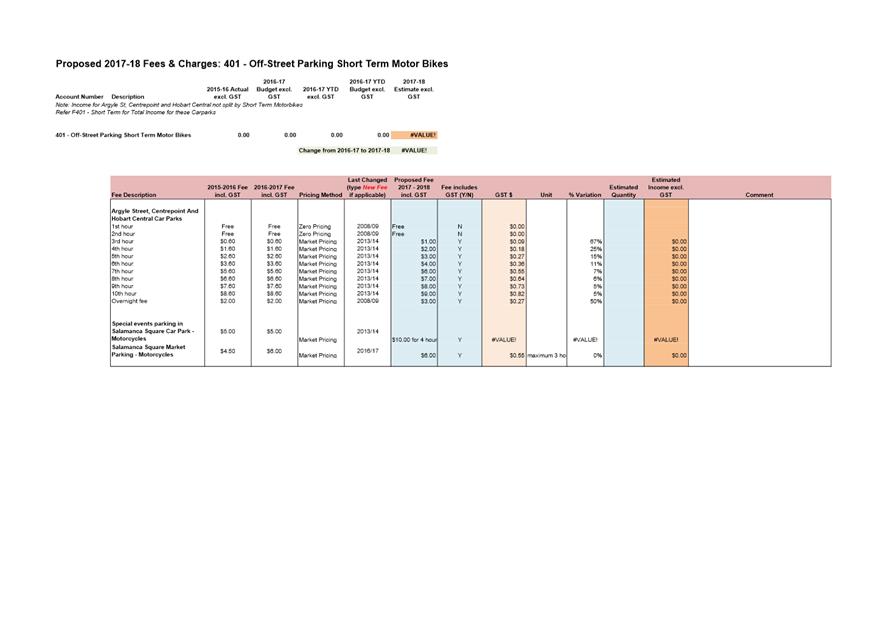

Off-Street Parking Short Term Motor Bikes

4.2.10. A 40 cent increase is proposed across all multi storey car parks for short term motor bike parking.

4.2.11. Currently the first 2 hours are free with the next hour being 60 cents and increasing in increments of $1.00 for every following hour. The proposal is for the 60 cents to increase to $1.00 with increments of $1.00 for every additional hour.

5. Proposal and Implementation

5.1. It is recommended that the attached schedules of fees and charges be adopted for the 2017/2018 financial year.

5.2. Fees and charges for 2017/2018 will become effective as at 1 July 2017.

5.3. Pursuant to section 206 of the Local Government Act 1993, the fees will be included in Council’s fees and charges booklet, which is made available to the community from Council’s website and the Customer Service Centre.

6. Strategic Planning and Policy Considerations

6.1. There are no direct strategic planning implications arising from this report.

6.2. The annual review of fees and charges has been undertaken in accordance with Council’s Pricing Policy and Guidelines.

7. Financial Implications

7.1. Funding Source and Impact on Current Year Operating Result

7.1.1. Not applicable.

7.2. Impact on Future Years’ Financial Result

7.2.1. The review of the fees and charges for Parking Operations has been undertaken and increases for the 2017/2018 financial year are expected to be:

|

FUNCTION AREA |

2016-17 BUDGET |

2017-18 ESTIMATE |

INCREASE / (DECREASE) |

|

|

Parking Enforcement (includes fine and meter collections) |

12,971,066.00 |

13,515,247.00 |

544,181.00 |

4.20% |

|

Off-Street Parking Short Term |

5,398,967.00 |

5,827,055.00 |

428,088.00 |

7.93% |

|

Off-Street Parking Long Term |

2,209,850.00 |

2,258,216.00 |

48,366.00 |

2.19% |

|

Meters, Voucher Machines etc (Dunn Place, Condell Place and Queens Domain car parks) |

730,500.00 |

772,000.00 |

41,500.00 |

5.68% |

7.3. Asset Related Implications

7.3.1. Not applicable.

8. Legal, Risk and Legislative Considerations

8.1. Pursuant to section 205 of the Local Government Act 1993, Council may impose fees and charges for various services.

8.2. Pursuant to section 206 of the LG Act, council is to keep a list of all fees and charged and make the list available for public inspection during ordinary hours of business.

9. Delegation

9.1. This matter is delegated to the Council.

As signatory to this report, I certify that, pursuant to Section 55(1) of the Local Government Act 1993, I hold no interest, as referred to in Section 49 of the Local Government Act 1993, in matters contained in this report.

|

Matthew Tyrrell Group Manager Parking Operations |

David Spinks Director Financial Services |

Date: 11 May 2017

File Reference: F17/43280

Attachment a: Parking

Enforcement ⇩ ![]()

Attachment

b: Off-Street

Parking Long Term ⇩ ![]()

Attachment

c: Off-Street

Parking Short Term ⇩ ![]()

Attachment

d: Off-Street

Parking Short Term - Motor Bikes ⇩ ![]()

Attachment

e: Meter,

Vouchers Machines and Meter Removal ⇩ ![]()

|

Agenda (Open Portion) Finance Committee Meeting |

Page 101 |

|

|

|

16/5/2017 |

|

A report indicating the status of current decisions is attached for the information of Aldermen.

REcommendation

That the information be received and noted.

Delegation: Committee

|

|

Agenda (Open Portion) Finance Committee Meeting |

Page 110 |

|

|

16/5/2017 |

|

Section 29 of the Local Government (Meeting Procedures) Regulations 2015.

File Ref: 13-1-10

An Alderman may ask a question without notice of the Chairman, another Alderman, the General Manager or the General Manager’s representative, in line with the following procedures:

1. The Chairman will refuse to accept a question without notice if it does not relate to the Terms of Reference of the Council committee at which it is asked.

2. In putting a question without notice, an Alderman must not:

(i) offer an argument or opinion; or

(ii) draw any inferences or make any imputations – except so far as may be necessary to explain the question.

3. The Chairman must not permit any debate of a question without notice or its answer.

4. The Chairman, Aldermen, General Manager or General Manager’s representative who is asked a question may decline to answer the question, if in the opinion of the respondent it is considered inappropriate due to its being unclear, insulting or improper.

5. The Chairman may require a question to be put in writing.

6. Where a question without notice is asked and answered at a meeting, both the question and the response will be recorded in the minutes of that meeting.

7. Where a response is not able to be provided at the meeting, the question will be taken on notice and

(i) the minutes of the meeting at which the question is asked will record the question and the fact that it has been taken on notice.

(ii) a written response will be provided to all Aldermen, at the appropriate time.

(iii) upon the answer to the question being circulated to Aldermen, both the question and the answer will be listed on the agenda for the next available ordinary meeting of the committee at which it was asked, where it will be listed for noting purposes only.

|

|

Agenda (Open Portion) Finance Committee Meeting |

Page 111 |

|

|

16/5/2017 |

|