City

of hobart

AGENDA

Finance Committee Meeting

Open Portion

Tuesday, 11 April 2017

at 5.00 pm

Lady Osborne Room, Town Hall

City

of hobart

AGENDA

Finance Committee Meeting

Open Portion

Tuesday, 11 April 2017

at 5.00 pm

Lady Osborne Room, Town Hall

THE MISSION

Our mission is to ensure good governance of our capital City.

THE VALUES

The Council is:

|

about people |

We value people – our community, our customers and colleagues. |

|

professional |

We take pride in our work. |

|

enterprising |

We look for ways to create value. |

|

responsive |

We’re accessible and focused on service. |

|

inclusive |

We respect diversity in people and ideas. |

|

making a difference |

We recognise that everything we do shapes Hobart’s future. |

|

|

Agenda (Open Portion) Finance Committee Meeting |

Page 3 |

|

|

11/4/2017 |

|

Business listed on the agenda is to be conducted in the order in which it is set out, unless the committee by simple majority determines otherwise.

APOLOGIES AND LEAVE OF ABSENCE

1. Co-Option of a Committee Member in the event of a vacancy

3. Consideration of Supplementary Items

4. Indications of Pecuniary and Conflicts of Interest

6.2 Investment of Council Funds - South Hobart and Foothills Community Bank

6.3 Remissions of Rates and Charges Granted

6.4 Request for Extension of Lease - Telstra Telecommunication Tower - Sandown Park, Sandy Bay

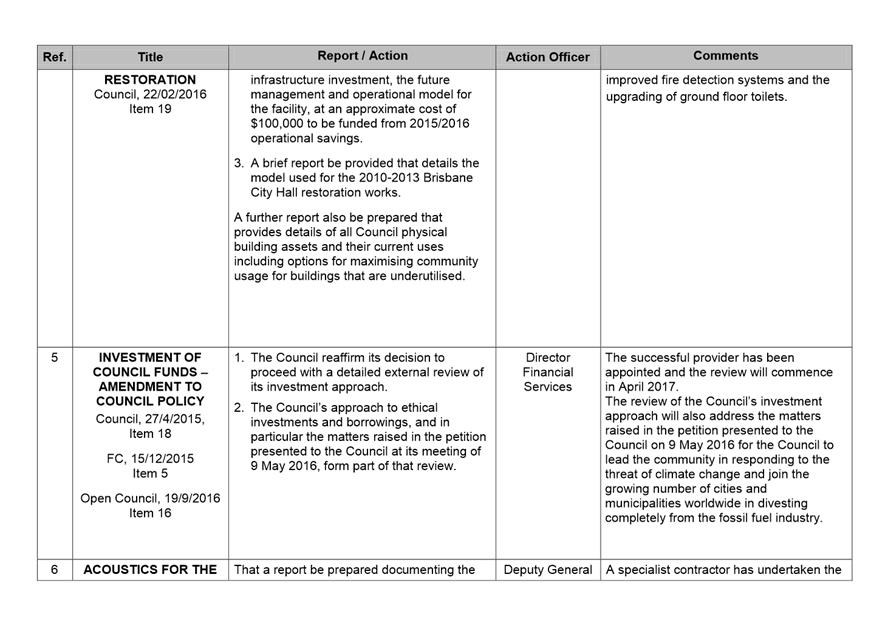

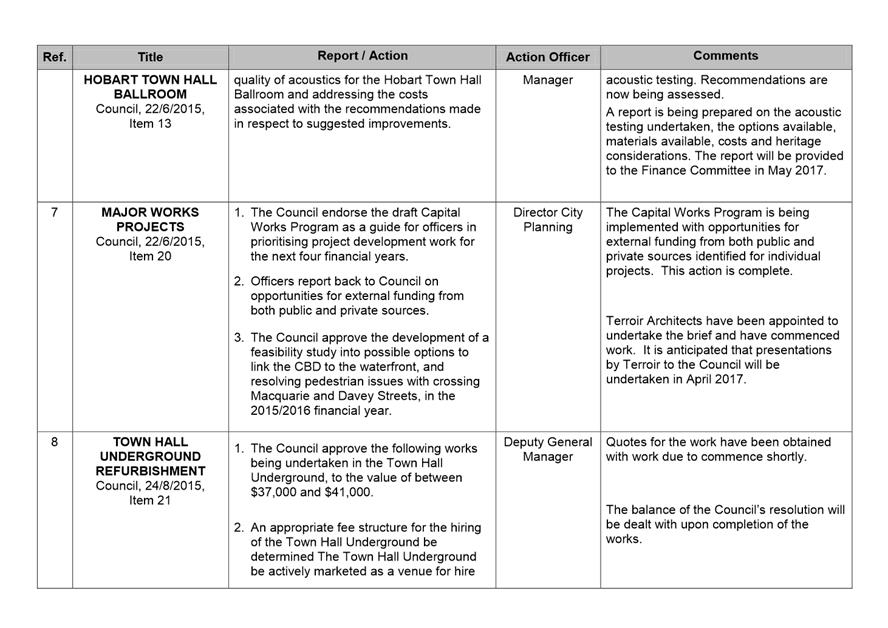

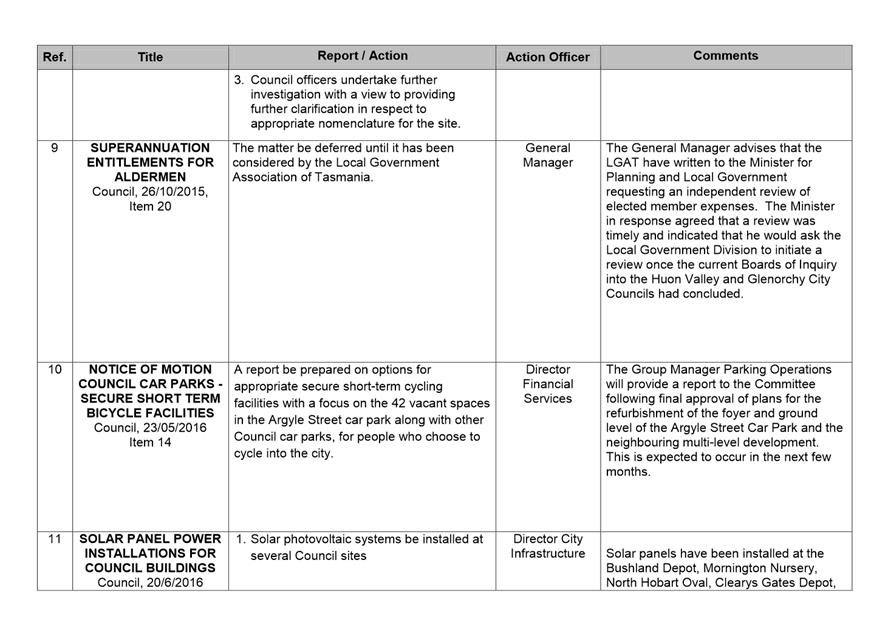

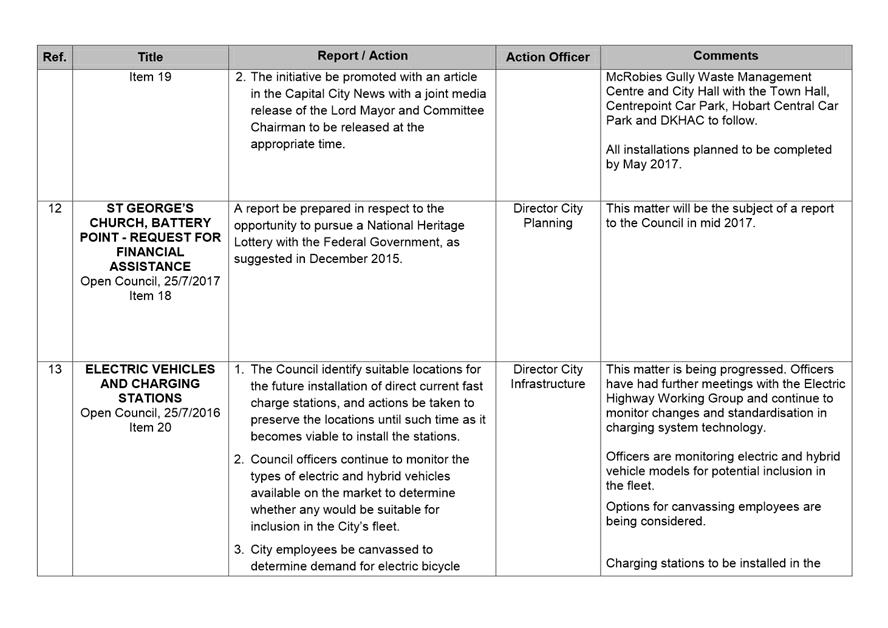

7 Committee Action Status Report

7.1 Committee Actions - Status Report

8. Responses to Questions Without Notice

8.1 Parking Compliance Issues - 54 King Street, Sandy Bay

10. Closed Portion Of The Meeting

|

|

Agenda (Open Portion) Finance Committee Meeting |

Page 4 |

|

|

11/4/2017 |

|

Finance Committee Meeting (Open Portion) held Tuesday, 11 April 2017 at 5.00 pm in the Lady Osborne Room, Town Hall.

|

COMMITTEE MEMBERS Thomas (Chairman) Deputy Lord Mayor Christie Zucco Ruzicka Sexton

ALDERMEN Lord Mayor Hickey Briscoe Burnet Cocker Reynolds Denison Harvey |

Apologies: Nil.

Leave of Absence: Alderman E R Ruzicka.

|

|

The minutes of the Open Portion of the Finance Committee meeting held on Tuesday, 21 March 2017, are submitted for confirming as an accurate record.

|

Ref: Part 2, Regulation 8(6) of the Local Government (Meeting Procedures) Regulations 2015.

|

That the Committee resolve to deal with any supplementary items not appearing on the agenda, as reported by the General Manager.

|

Ref: Part 2, Regulation 8(7) of the Local Government (Meeting Procedures) Regulations 2015.

Aldermen are requested to indicate where they may have any pecuniary or conflict of interest in respect to any matter appearing on the agenda, or any supplementary item to the agenda, which the committee has resolved to deal with.

Regulation 15 of the Local Government (Meeting Procedures) Regulations 2015.

A committee may close a part of a meeting to the public where a matter to be discussed falls within 15(2) of the above regulations.

In the event that the committee transfer an item to the closed portion, the reasons for doing so should be stated.

Are there any items which should be transferred from this agenda to the closed portion of the agenda, or from the closed to the open portion of the agenda?

|

Agenda (Open Portion) Finance Committee Meeting |

Page 6 |

|

|

|

11/4/2017 |

|

File Ref: F17/32407

Report of the Manager Finance and the Director Financial Services of 6 April 2017 and attachments.

Delegation: Council

|

Item No. 6.1 |

Agenda (Open Portion) Finance Committee Meeting |

Page 7 |

|

|

11/4/2017 |

|

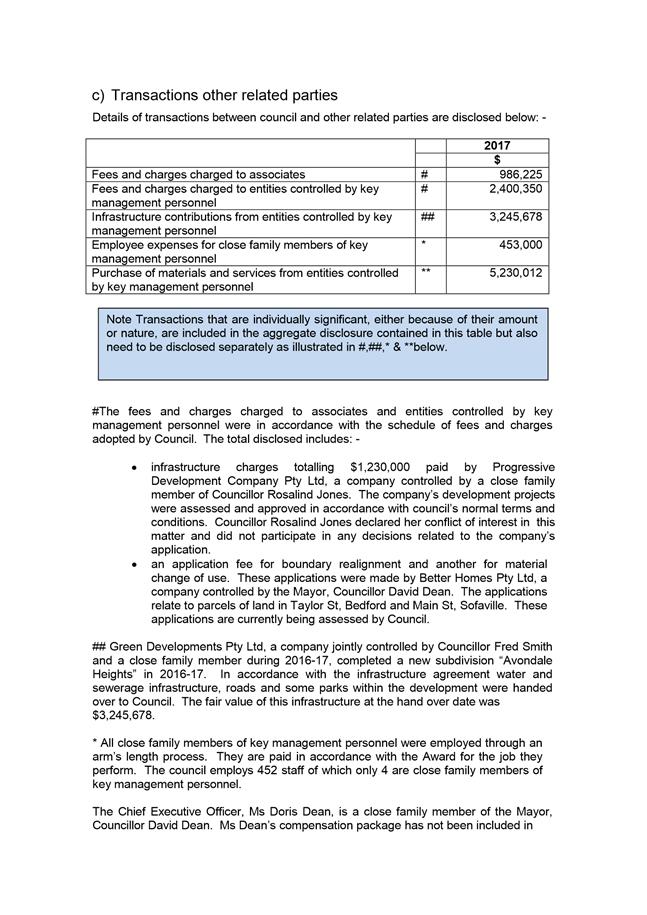

REPORT TITLE: Related Party Disclosures

REPORT PROVIDED BY: Manager Finance

Director Financial Services

1. Report Purpose and Community Benefit

1.1. The purpose of this report is to inform the Council about the requirements of an Accounting Standard which will apply to the Council for the first time in 2016-2017, and will continue to apply in future years.

1.2. The title of the Accounting Standard is AASB 124 Related Party Disclosures.

2. Report Summary

2.1. Accounting Standard AASB 124 Related Party Disclosures will apply to the Council for the first time in 2016-2017, and will continue to apply in future years.

2.2. AASB 124 will require Council’s annual financial statements to contain disclosures about Council’s related parties and related party transactions. Council’s related parties will include Aldermen and senior employees.

2.3. A Council policy is necessary to outline what is expected of Aldermen and Council staff in relation to AASB 124. Specifically, the policy outlines the disclosure requirements under AASB 124 of Key Management Personnel (KMP), which includes Aldermen. It also outlines the procedures Council will follow to collect, store, manage and report on related party relationships, transactions and commitments.

2.4. The draft policy has been forwarded to the Risk and Audit Panel out of session for comment and feedback. The Panel will formalise their response at its next meeting, however, feedback from the two Panel members who responded indicates their satisfaction with what is proposed. No changes were requested.

|

That the Council adopt the draft policy titled ‘Related Party Disclosures’, marked as Attachment A to the report.

|

4. Background

4.1. AASB 124 has applied to private sector entities for many years. Until now, the not-for-profit sector (which includes Local Government) has been afforded an exemption from the requirements of the Standard. This exemption has been removed with effect from the 2016-2017 financial year.

4.2. Council’s financial statements for 2016-2017 (and beyond) will therefore need to comply with AASB 124. This will require the Council’s financial statements to contain certain disclosures about its related parties. Failure to comply would result in the Auditor-General issuing a qualified audit report in respect of the Council’s financial statements.

4.3. The purpose of AASB 124 is to ensure that an entity’s financial statements contain the disclosures necessary to draw attention to the possibility that its financial position and performance may have been affected by the existence of related parties and by transactions and outstanding balances, including commitments, with such parties.

4.4. Council’s related parties are likely to include Aldermen, the General Manager, Directors, their close family members and any entities that they control or jointly control.

5. Proposal and Implementation

5.1. The following steps are necessary to comply with AASB 124: -

5.1.1. Establish a system to identify and record related parties and related party relationships;

5.1.2. Identify ordinary citizen transactions (OCTs);

5.1.3. Establish a system to identify and record related party transactions and related party transaction terms and conditions;

5.1.4. Assess materiality of the related party transactions that have been captured; and

5.1.5. Make disclosure.

5.2. It is proposed that Council adopt a policy which addresses each of the above steps. A draft policy is included at Attachment A.

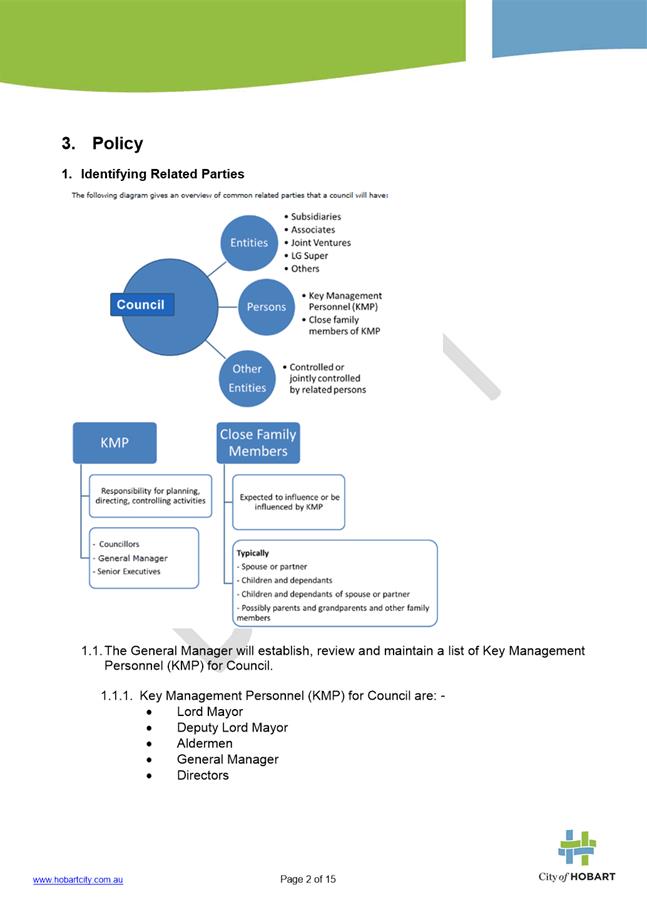

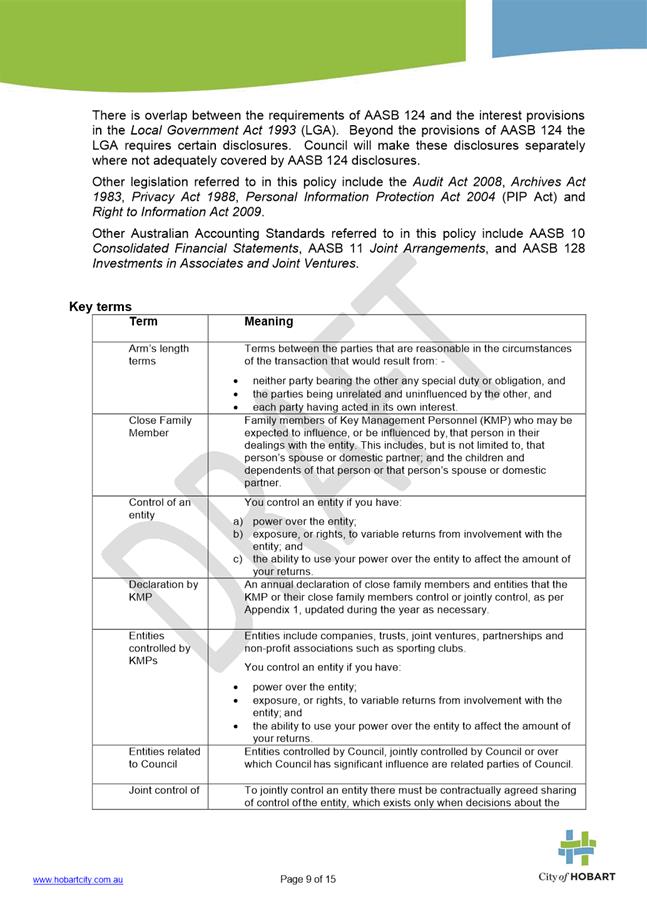

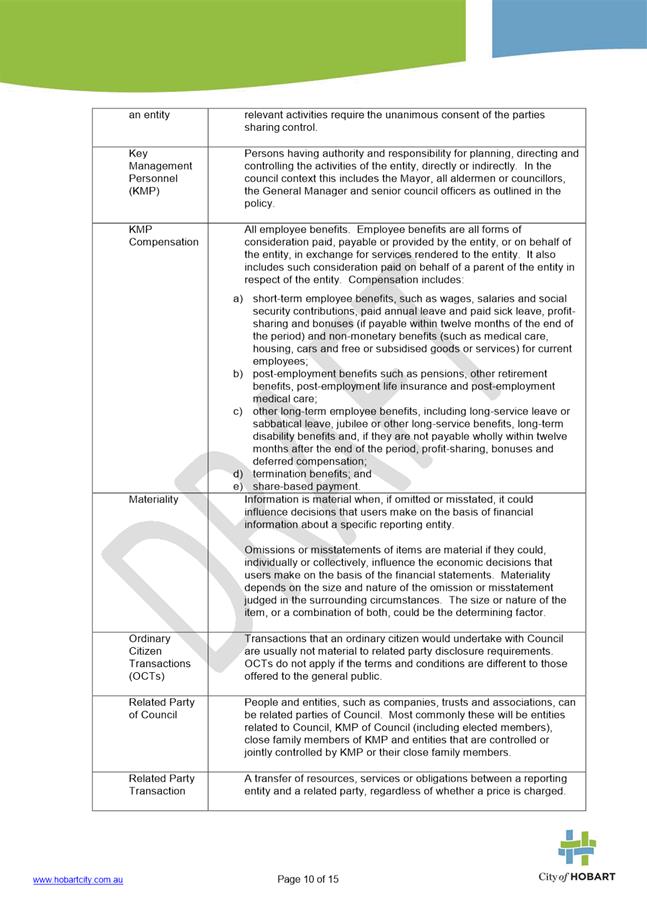

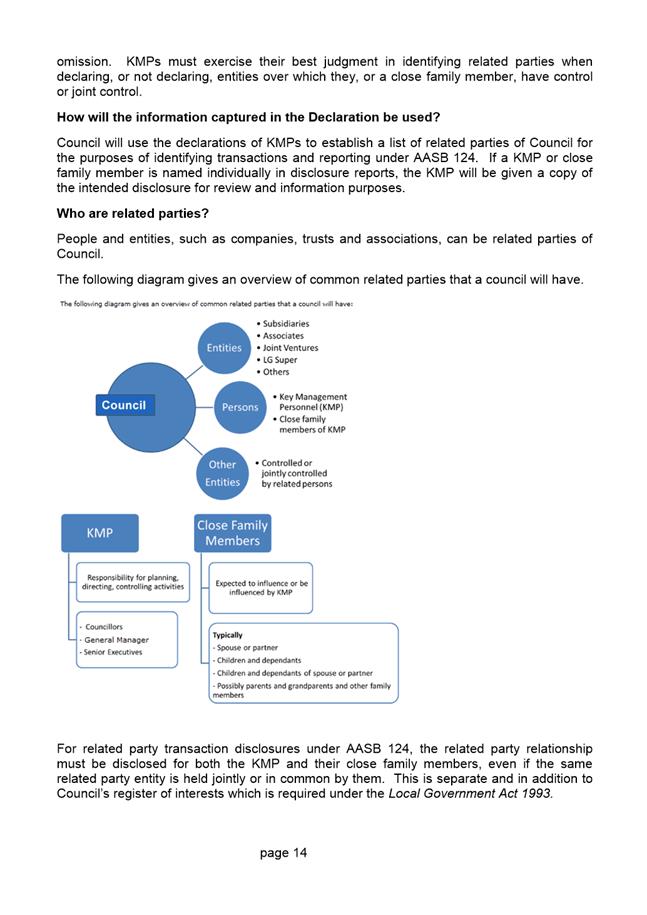

Who and what are related parties of Council?

5.3. People and entities (companies, trusts, associations, etc.) can be related parties of a Council.

5.4. The most common related parties of a Council will be: -

5.4.1. Entities related to Council;

5.4.2. Key Management Personnel (KMP) of Council;

5.4.3. Close family members of KMP; and

5.4.4. Entities that are controlled or jointly controlled by KMP or their close family members.

What entities are related to Council?

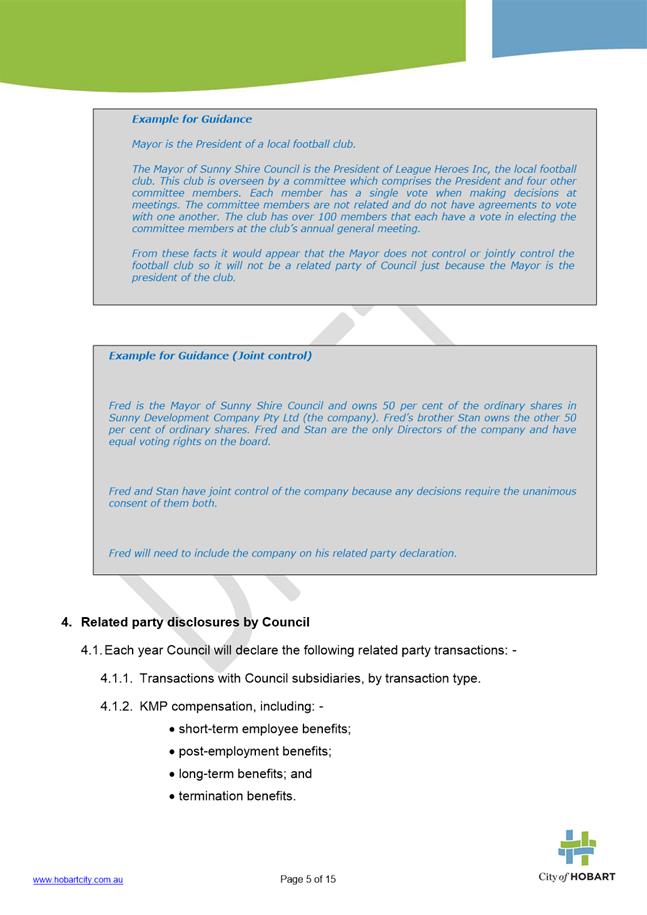

5.5. Entities controlled by Council, jointly controlled by Council, or over which Council has “significant influence” are related parties of Council.

5.6. The Council will need to identify transactions with these entities and may need to make extra disclosure about them in Council’s financial statements.

5.7. Guidance on assessing control, joint control and significant influence is contained in Accounting Standards.

5.8. Based on this guidance, it would appear that the Council does not control or jointly control any other entities.

5.9. Does the Council have significant influence over any other entities? The guidance defines significant influence as “the power to participate in the financial and operating policy decisions of an investee, but is not control or joint control of those policies”.

5.10. The guidance goes on to suggest that if an entity holds 20% or more of the voting power of an investee, it is presumed that the entity has significant influence, unless it can be clearly demonstrated that this is not the case.

5.11. Conversely, if an entity holds less than 20% of the voting power of an investee, it is presumed that the entity does not have significant influence, unless such influence can be clearly demonstrated.

5.12. Based on this guidance, TasWater is unlikely to be a related entity of Council because Council’s voting power in TasWater is only around 10%.

5.13. All superannuation schemes to which Council makes contributions on behalf of its employees (e.g. Tasplan) are related entities of Council regardless of control, joint control or significant influence.

Who are Council’s Key Management Personnel?

5.14. Key Management Personnel (KMP) are defined as “those persons having authority and responsibility for planning, directing and controlling the activities of the entity, directly or indirectly”.

5.15. Judgement needs to be exercised in deciding which individuals meet the above definition of KMP.

5.16. It is likely that all of the following will be KMP: -

5.16.1. Lord Mayor;

5.16.2. Deputy Lord Mayor;

5.16.3. Aldermen;

5.16.4. General Manager; and

5.16.5. Directors.

Who are close family members of Council’s KMP?

5.17. Close family members are defined as “family members who may be expected to influence, or be influenced by, the KMP in their dealings with Council”.

5.18. Close family members will include: -

5.18.1. Your spouse/domestic partner;

5.18.2. Your children;

5.18.3. Your dependants;

5.18.4. Children of your spouse/domestic partner; and

5.18.5. Dependants of your spouse/domestic partner.

5.19. Close family members could also include the following if they could be expected to influence, or be influenced by, the KMP in their dealings with Council: -

5.19.1. Your brothers and sisters;

5.19.2. Your aunts, uncles and cousins;

5.19.3. Your parents and grandparents;

5.19.4. Your nieces and nephews; and

5.19.5. Any other member of your family.

5.20. Friends of KMP are not close family members.

What is an entity controlled or jointly controlled by KMP or their close family members?

5.21. Entities include companies, trusts, incorporated and unincorporated associations such as clubs and charities, joint ventures and partnerships.

5.22. You control an entity if you have: -

5.22.1. Power over the entity;

5.22.2. Exposure, or rights, to variable returns from involvement with the entity; and

5.22.3. The ability to use your power over the entity to affect the amount of your returns.

5.23. To jointly control an entity there must be contractually agreed sharing of control of the entity, which exists only when decisions about the relevant activities require the unanimous consent of the parties sharing control.

5.24. In some cases it will be obvious whether control or joint control exists. In other cases control or joint control will be less clear, and judgement will be required.

How will related parties and related party relationships be identified and recorded?

5.25. The draft policy (refer Attachment A) proposes the following : -

5.25.1. The General Manager will establish, review and maintain a list of KMP for the Council;

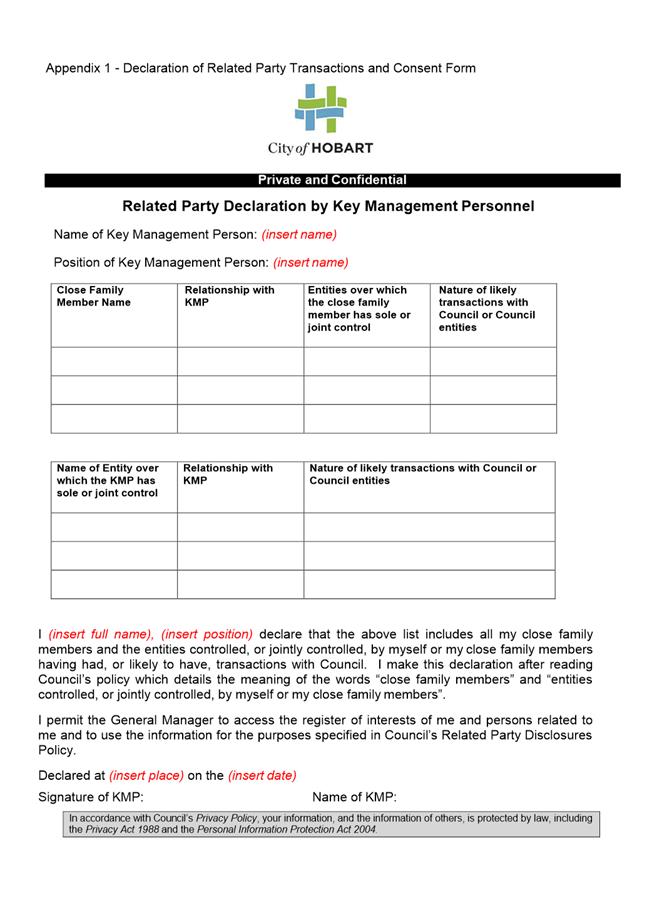

5.25.2. Each KMP will complete an annual declaration which details that person’s close family members, and entities (if any) which are controlled or jointly controlled by that KMP or their close family members, and which are likely to have transactions with the Council. An example of the format of this annual declaration is contained in Appendix 1;

5.25.3. Annual declarations will be provided by 1 July each year covering the forthcoming financial year, together with an updated declaration for the previous financial year;

5.25.4. KMPs will be responsible for updating their declarations should they become aware of a change, error or omission; and

5.25.5. Declarations made by KMP will be used to establish a list of related parties for the purpose of identifying transactions and reporting in accordance with AASB 124.

Ordinary Citizen Transactions (OCTs)

5.26. Related party transactions which occur during the course of delivering its public service objectives and which occur on terms no different to those that apply to the general public are termed ordinary citizen transactions (OCTs).

5.27. Council may determine that OCTs are not material transactions because of their nature and exclude them from being recorded as a related party transaction.

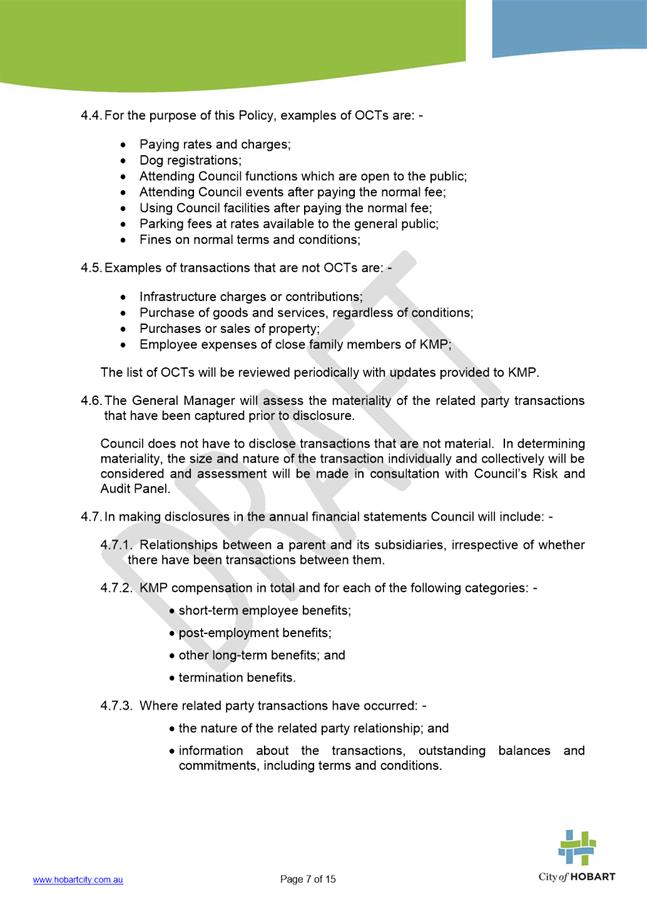

5.28. The draft policy (refer Attachment A) proposes that the following transactions be recognised as OCTs: -

5.28.1. Paying rates and charges;

5.28.2. Dog registrations;

5.28.3. Attending Council functions which are open to the public;

5.28.4. Attending Council events after paying the normal fee;

5.28.5. Using Council facilities after paying the normal fee;

5.28.6. Parking fees at rates available to the general public;

5.28.7. Fines on normal terms and conditions.

5.29. However, if any of the above transactions were to occur on terms and conditions that are different to those offered to the general public, the transaction may become material.

5.30. The draft policy (refer Attachment A) proposes that the following transactions not be recognised as OCTs: -

5.30.1. Infrastructure charges or contributions;

5.30.2. Purchase of goods and services, regardless of conditions;

5.30.3. Purchases or sales of property;

5.30.4. Employee expenses of close family members of KMP;

Establishing a system to identify and record related party transactions (and terms and conditions)

5.31. It is proposed that a ‘Register of Related Party Transactions’ be established to capture and record information for each existing or potential related party transaction (including ordinary citizen transactions assessed as being material in nature).

5.32. The ‘Register of Related Party Transactions’ would detail the following for each related party transaction: -

5.32.1. Description of the related party transaction;

5.32.2. Name of the related party;

5.32.3. Nature of the related party’s relationship with Council;

5.32.4. Whether the notified related party transaction is existing or potential;

5.32.5. References to any relevant documentation.

5.33. It may be possible to identify related party transactions with a special code in Council’s accounting system. Transactions which do not pass through Council’s accounting system would need to be captured separately.

Assessing materiality of related party transactions

5.34. Prior to preparing disclosures for Council’s financial statements, related party transactions should be assessed for materiality. Transactions that are not considered material do not need to be disclosed.

5.35. Assessing materiality requires judgement and should be done in consultation with Council’s Risk and Audit Panel and Council’s external auditor (the Auditor-General). Accounting standards provide some guidance on assessing materiality.

5.36. When assessing materiality, Council needs to consider both the size and nature of transactions, individually and collectively.

Disclosing related party transactions

5.37. Council will need to make the following disclosures in its annual financial statements: -

5.37.1. Key Management Personnel compensation in total and for each of the following categories: -

5.37.1.1. Short-term employee benefits;

5.37.1.2. Post-employment benefits;

5.37.1.3. Other long-term benefits;

5.37.1.4. Termination benefits.

5.37.2. Where related party transactions have occurred: -

5.37.2.1. The nature of the related party relationship;

5.37.2.2. Information about the transactions, outstanding balances and commitments, including terms and conditions;

5.37.3. Separate disclosure for each of the following categories of related parties: -

5.37.3.1. Key management personnel;

5.37.3.2. Other related parties.

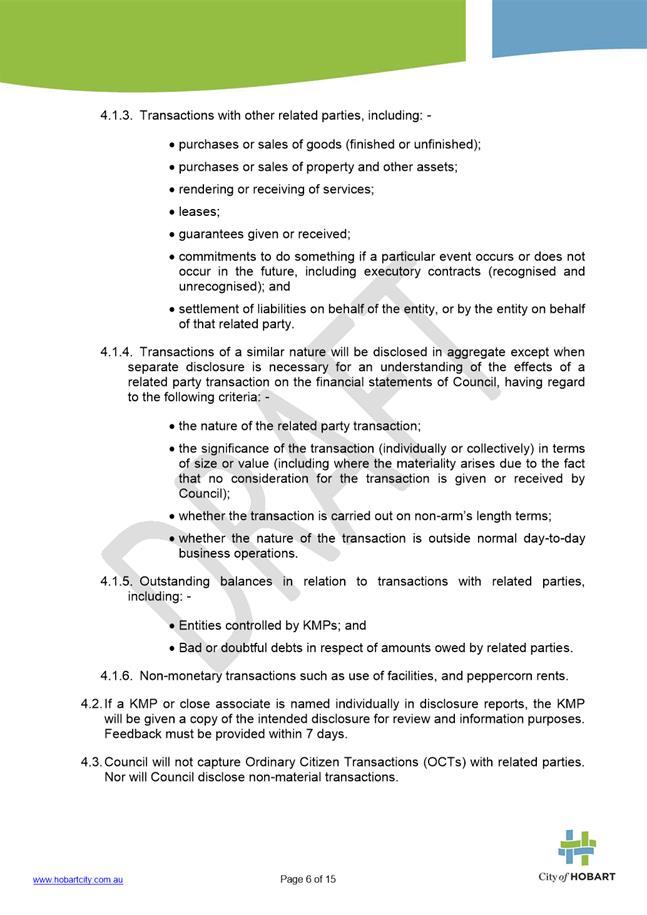

5.37.4. Disclosure of the following types of transactions: -

5.37.4.1. Purchases or sales of goods;

5.37.4.2. Purchases or sales of property and other assets;

5.37.4.3. Rendering or receiving of services;

5.37.4.4. Leases;

5.37.4.5. Guarantees given or received;

5.37.4.6. Commitments;

5.37.4.7. Loans and settlements of liabilities;

5.37.4.8. Expense recognised during the period in respect of bad debts;

5.37.4.9. Provision for doubtful debts relating to outstanding balances.

5.38. Transactions of a similar nature will be disclosed in aggregate except when separate disclosure is necessary for an understanding of the effects of a related party transaction on Council’s financial statements having regard to the following criteria: -

5.38.1. The nature of the related party transaction;

5.38.2. The significance of the transaction (individually or collectively) in terms of size or value (including where the materiality arises due to the fact that no consideration for the transaction is given or received by Council);

5.38.3. Whether the transaction is carried-out on non-arm’s length terms;

5.38.4. Whether the nature of the transaction is outside normal day-to-day business operations.

5.39. If a KMP or a close associate (a close family member, or an entity controlled or jointly controlled by the KMP or a close family member) is named individually in disclosure reports, the KMP will be given a copy of the intended disclosure for review and information purposes. The KMP will be given an opportunity to provide feedback on the intended disclosure.

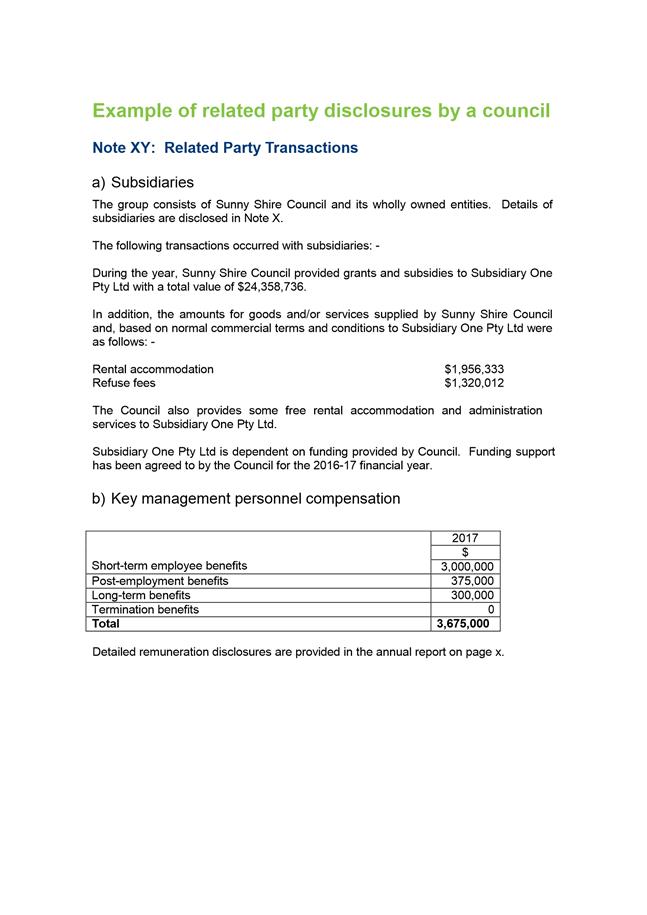

5.40. Attachment B contains an example of how the above disclosures might look for a particular council.

5.41. It may be possible to incorporate the disclosures required by Section 72 of the LGA (remuneration of senior employees and statement of allowances and expenses paid to elected members) into the related party disclosures in the annual financial statements because these are contained within Council’s Annual Report.

6. Strategic Planning and Policy Considerations

6.1. Adoption of the proposed policy will support the Council’s goal to provide good governance, and to be more open and transparent in its decision-making.

7. Financial Implications

7.1. Funding Source and Impact on Current Year Operating Result

7.1.1. Nil

7.2. Impact on Future Years’ Financial Result

7.2.1. Nil

7.3. Asset Related Implications

7.3.1. Nil

8. Legal, Risk and Legislative Considerations

8.1. The Local Government Act 1993 and the Audit Act 2008 require all local governments in Tasmania to produce annual financial statements which comply with Australian Accounting Standards.

8.2. The Auditor-General has no power to exempt local governments from complying with AASB 124 or any other Accounting Standard.

8.3. The required disclosures may prompt further public scrutiny of Aldermanic allowances and benefits. However, it must be noted that this information will be combined with information about senior employee remuneration, because financial statement disclosures are required for ‘Key Management Personnel’, not for Aldermen separately.

9. Delegation

9.1. This matter is delegated to the Council.

As signatory to this report, I certify that, pursuant to Section 55(1) of the Local Government Act 1993, I hold no interest, as referred to in Section 49 of the Local Government Act 1993, in matters contained in this report.

|

Peter Jenkins Manager Finance |

David Spinks Director Financial Services |

Date: 6 April 2017

File Reference: F17/32407

Attachment a: Draft

Policy - Related Party Disclosures ⇩ ![]()

Attachment

b: Example

Disclosure ⇩ ![]()

|

Agenda (Open Portion) Finance Committee Meeting |

Page 34 |

|

|

|

11/4/2017 |

|

6.2 Investment of Council Funds - South Hobart and Foothills Community Bank

File Ref: F17/33556

Report of the Director Financial Services of 6 April 2017 and attachments.

Delegation: Council

|

Item No. 6.2 |

Agenda (Open Portion) Finance Committee Meeting |

Page 35 |

|

|

11/4/2017 |

|

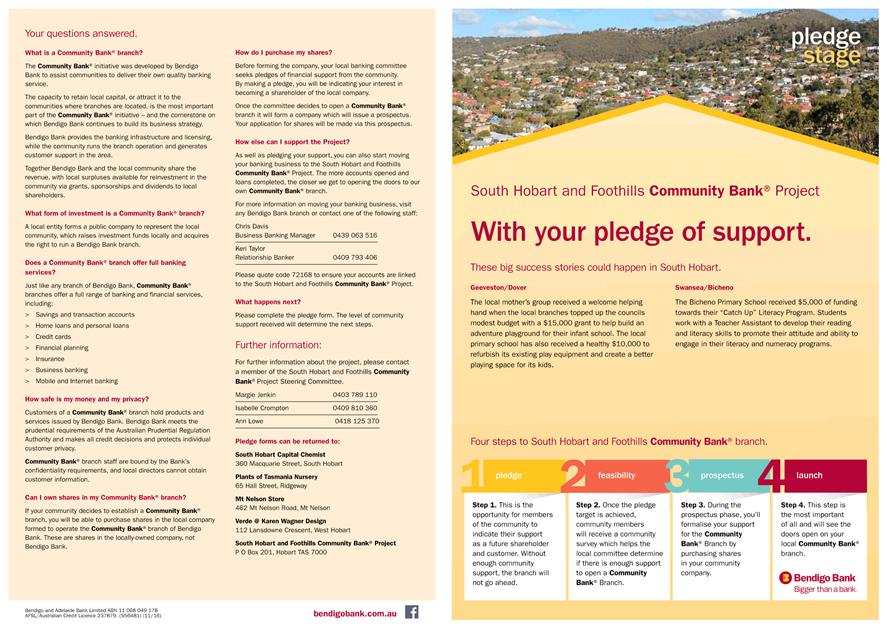

REPORT TITLE: Investment of Council Funds - South Hobart and Foothills Community Bank

REPORT PROVIDED BY: Director Financial Services

1. Report Purpose and Community Benefit

1.1. This report provides an update on the South Hobart and Foothills Community Bank and provides Council with the opportunity to reconsider whether it wishes to pledge to purchase shares or provide some type of support to the proposal.

2. Report Summary

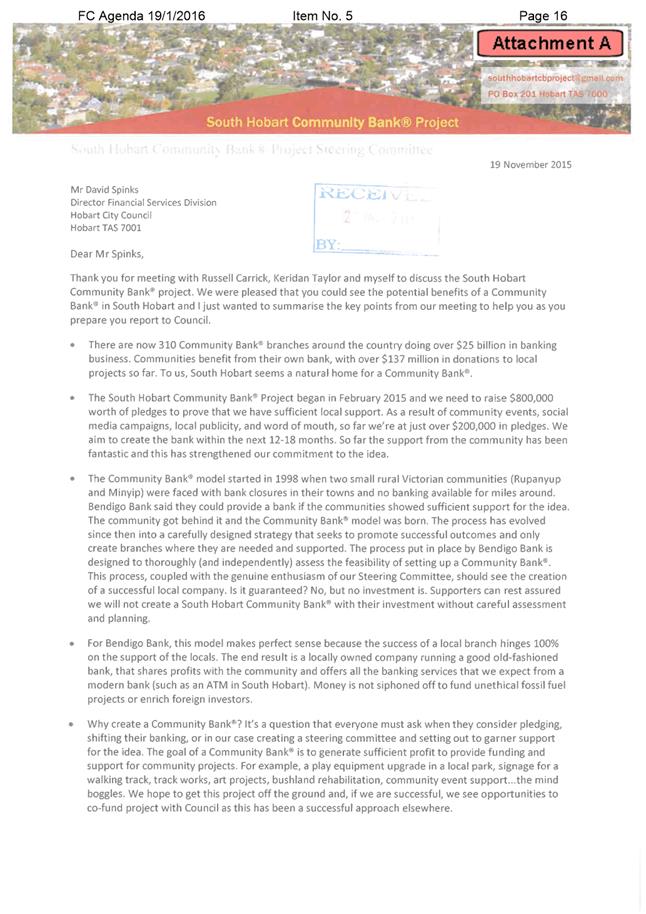

2.1. The Steering Committee for the South Hobart and Foothills Community Bank (SHFCB) has requested Council reconsider showing its support for the Community Bank® project.

2.2. The Council first considered the project in January 2016.

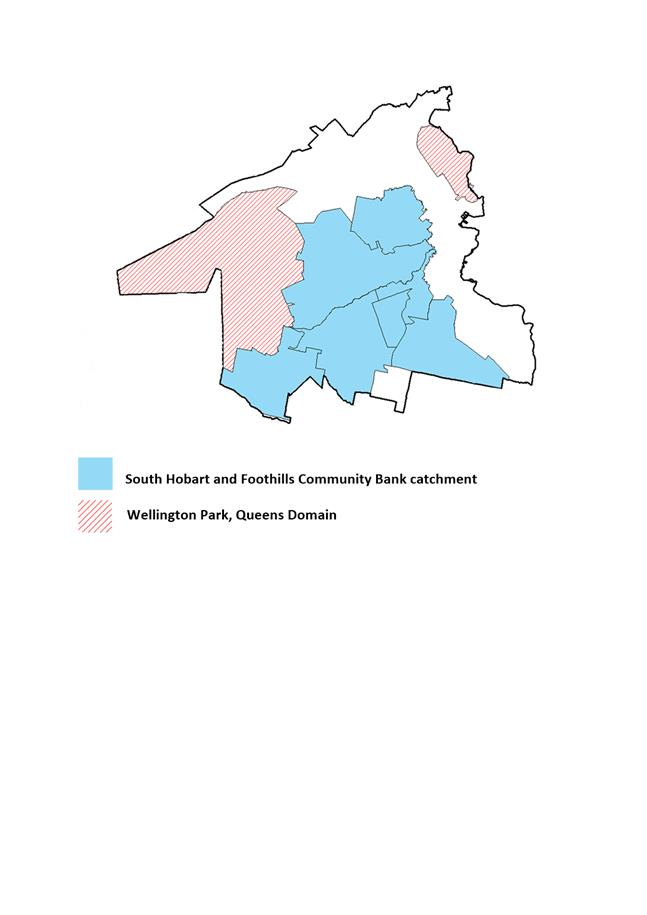

2.3. Since that time, the Steering Committee has expanded the catchment area to now include six suburbs in addition to South Hobart representing over three quarters of the populated area of the City of Hobart.

2.4. The project was previously known as the South Hobart Community Bank, but is now termed the South Hobart and Foothills Community Bank. Over the past 12 months the Steering Committee has been actively engaging within the expanded community base and increased its pledges.

2.5. There is no obligation for Council to provide support. In the event it resolves to do so, this can be shown in a number of ways. These include pledging to purchase shares in the company, providing funding to complete an independent feasibility study, linking current Council investments with Bendigo Bank to the SHFCB, or perhaps even in kind assistance of some type.

|

That the Council consider whether it wishes to provide support to the South Hobart and Foothills Community Bank® and if so, in what form that support will take.

|

4. Background

4.1. At the meeting of 19 January 2016 the Finance Committee considered a report (Attachment A) on this proposal. This current report does not reproduce all information from that January 2016 report, and accordingly, the two should be read in conjunction. Committee resolved the following:

4.1.1. The Council pledges to purchase $50,000 worth of shares in the South Hobart Community Bank® and authorises the General Manager to complete and submit the pledge form as shown at Attachment B.

4.1.2. Current and future cash investments with the Bendigo Bank be linked to the South Hobart Community Bank branch.

4.1.3. The City of Hobart’s support for the South Hobart Community Bank be acknowledged in relevant South Hobart Community Bank promotional and marketing material as appropriate.

4.2. The recommendation was lost at Council on 25 January 2016.

4.3. Since that time the Steering Committee has expanded the catchment area which now incorporates the suburbs of South Hobart, Sandy Bay, West Hobart, Dynnyrne, Fern Tree, Ridgeway, Mount Nelson and Tolmans Hill. Representatives from the expanded catchment areas also have a place on the Steering Committee.

4.4. The project, now known as the South Hobart and Foothills Community Bank, incorporates over three quarters of the populated area of the City of Hobart municipal area (see attached map).

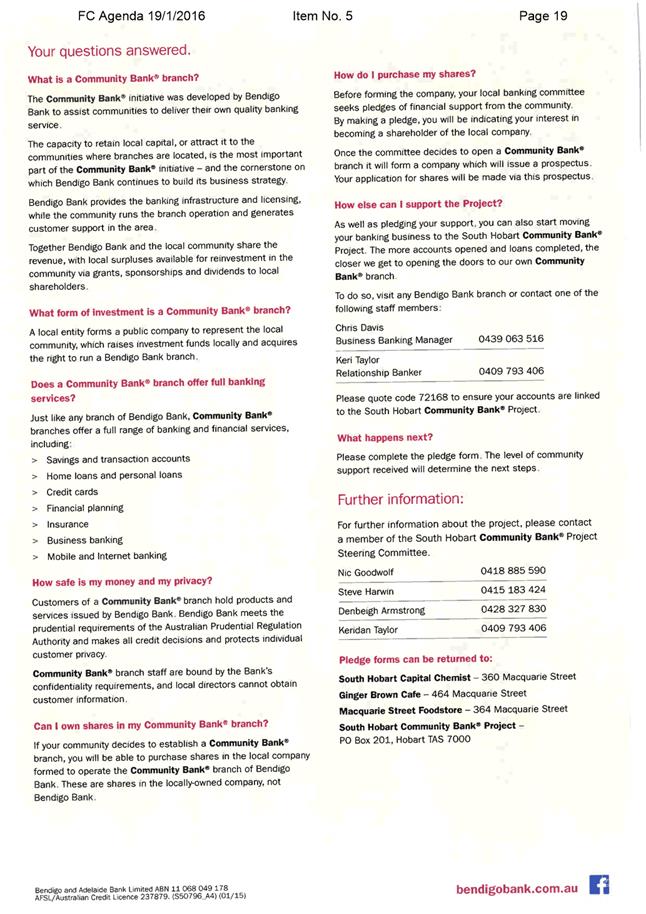

4.5. Bendigo Bank developed the Community Bank® model in 1998 and at the end of 2015/16 there were 313 Community Bank® branches located in rural and metropolitan areas.

4.6. Community Bank® local branches are locally owned companies which shares profits with the community while offering all services expected of a modern bank.

4.7. The Community Bank® model allows for the revenue to be shared equally between the locally owned company and Bendigo Bank, the locally owned company’s profits are then returned to the local community with 80% returned in grants and sponsorship and 20% returned to shareholders in the form of dividends.

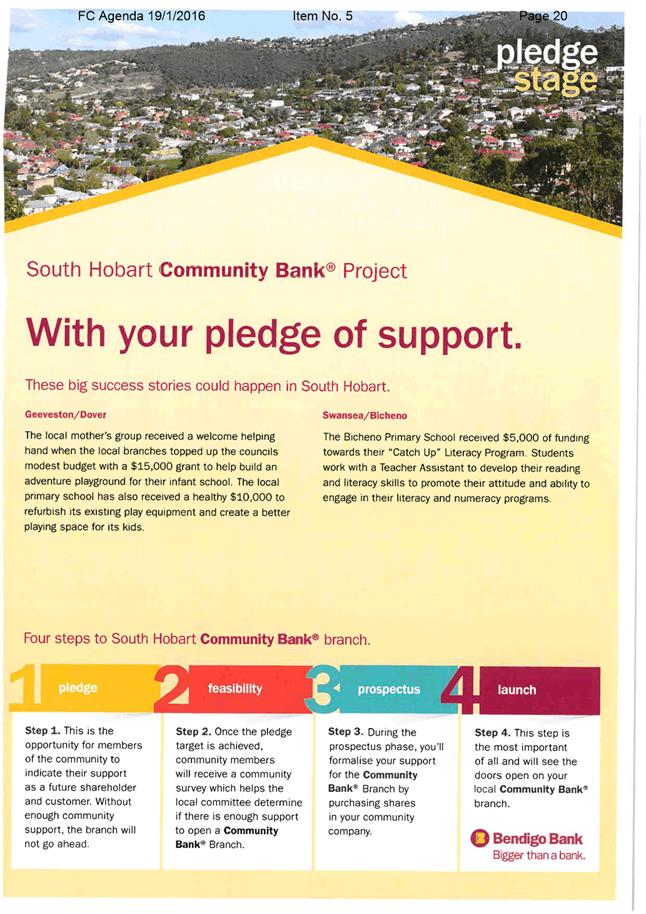

4.8. There are currently 12 Community Bank® branches successfully operating in Tasmania. In total, over $1.7 million has been given back to community groups, organisations, enterprises, sporting clubs and individuals in Tasmania since the first Community Bank® opened 14 years ago.

4.9. The expanded catchment of the SHFCB area will provide wider community benefit through investment in community projects and payment of dividends to shareholders.

4.10. Since the report of January 2016, the Steering Committee has been actively engaging in these neighbourhoods, through advertising in local newsletters, letterboxing, a street presence and attending community meetings.

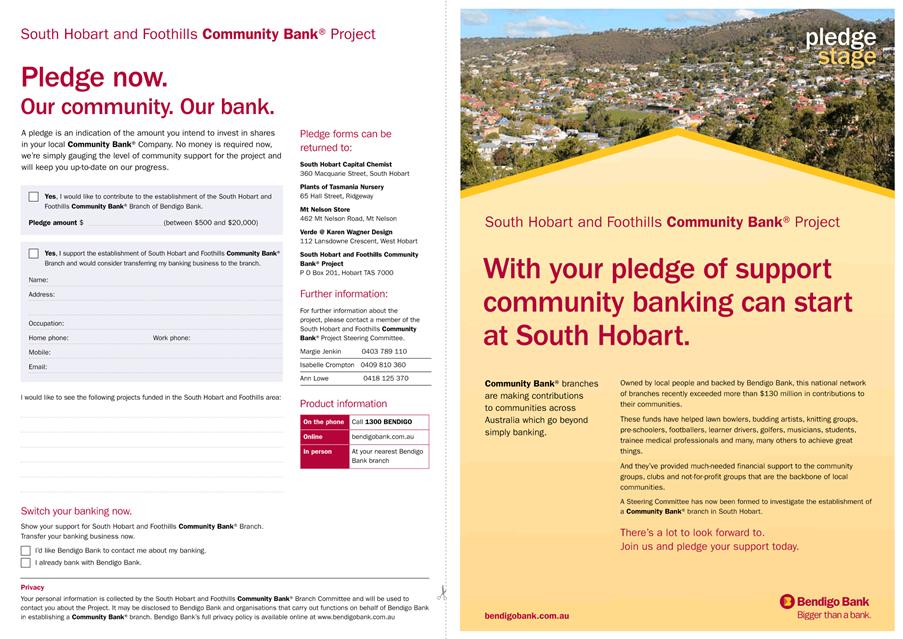

4.11. In January 2016 it was reported that $200,000 in pledges had been received from 80 people. Officers are advised that to date the SHFCB has increased its pledges to approximately $338,500 from 154 people, showing growing community support for the project.

4.12. The Steering Committee have reported they are on track to raise a further $400,000 in pledges by June 2017.

4.13. Support to the project can also be shown by community members moving their banking business to the Bendigo Bank and linking their accounts to the SHFCB project. The target is to have $10 million business on the books notionally attributed to the SHFCB project before the proposed branch would open. To date $5.5 million business on the books has been notionally attributed to the project.

4.14. Bendigo Bank has indicated that the start up cost for a Community Bank branch in South Hobart could be in the order of $800,000, although this is not a definitive figure. However, it would be hoped that pledge amounts would ultimately reach this figure, or close to.

4.15. The Steering Committee also report a noticeable change within the community for a preference to investment and banking with non fossil fuel institutions making a Bendigo Bank Community Bank a preferred option. It is reported that currently 8% of the South Hobart community bank with Bendigo Bank.

5. Proposal and Implementation

5.1. It is proposed that the Council consider whether it wishes to show support to the SHFCB proposal, and if so, in what form that support takes.

5.2. It is worth reminding that the process is still in its early stages. The Bendigo Bank has a robust framework which it follows before entering into a franchise agreement for a community bank. As noted above, the pledge target of $800,000 (or close to), and the business on the books target of $10M (or close to) need to be reached before proceeding. Following this there is a feasibility survey process, a business case process and finally a capital raising process requiring the issuing of an ASIC approved share prospectus.

5.3. Support could be provided in a number of ways. These include the following.

5.4. Purchasing shares in the company to be formed. The Steering Committee has requested that Council consider pledging to purchase $30,000 to $50,000 worth of shares in the SHFCB.

5.4.1. It should be noted that by making a pledge Council is not making a financial commitment at this time. As noted above, there is a process to be followed that could take several years. A further report would be prepared for the Council’s consideration upon the issuing of a prospectus, should the proposal reach that stage.

5.5. Funding the feasibility survey. The Steering Committee has also requested the Council consider providing funding for the independent feasibility study. It is estimated the cost of this be around $10,000 to $12,000.

5.5.1. A feasibility study is not undertaken until Bendigo Bank are satisfied with the level of community support demonstrated through pledges and business support.

5.6. Linking current Council investments with Bendigo Bank to the SHFCB. This action would count towards the $10M business on the books target. Council currently has term deposit funds with Bendigo Bank.

6. Strategic Planning and Policy Considerations

6.1. Investment in the SHFCB is consistent with the Council’s Strategic Objectives in the Capital City Strategic Plan 2015-2025:

Strategic Objecting 1.1: Partnerships with Government, the education sector and business create city growth.

6.2. The investment is also consistent with the Policy on Investment of Council Funds in that the Bendigo Bank does not invest in the fossil fuel industry.

7. Financial Implications

7.1. Funding Source and Impact on Current Year Operating Result

7.1.1. Not applicable.

7.2. Impact on Future Years’ Financial Result

7.2.1. Should Council approve the proposal to fund the independent feasibility study for the SHFCB the cost is estimated to be between $10,000 and $12,000.

7.2.2. There is no cost to the Council in pledging to purchase shares. A future report would be provided for Council endorsement should the SHFCB proceed and pledges are called in.

7.3. Asset Related Implications

7.3.1. Not applicable.

8. Legal, Risk and Legislative Considerations

8.1. There are a number of risk that may affect the Council investment in the SHFCB. These are explained at length in Section 6 of Attachment A and include;

8.1.1. Insufficient revenue;

8.1.2. Changes to economic conditions;

8.1.3. Increased competition;

8.1.4. Sale of shares;

8.1.5. Withdrawal of pledges.

8.2. The Bendigo Bank has a robust framework which it follows to mitigate any risk of failure before entering into a franchise agreement for a Community Bank.

8.3. As with all investments in shares there is no guarantee that the Council or other shareholders will receive dividends. However the motivation for most shareholders in the Community Bank® is to invest in a community enterprise which provides a service and deliver funding for community projects.

9. Social and Customer Considerations

9.1. Shareholders and account holders in local Community Banks® are attracted to them because they are owned by and operated by local people with the profits being reinvested back into the community. They allow the local community to become involved in decisions about investments in community projects from the Community Bank® and can encourage higher rates of participation in community related events and projects. To date Community Banks® have donated over $137M to local projects.

9.2. Should it decide to invest in the SHFCB the Council’s investment could be seen as a demonstration of support for the project rather than a financial investment.

10. Community and Stakeholder Engagement

10.1. The SHFCB steering committee was established in February 2015 and is currently seeking pledges of support. Officers are advised that to date the SHFCB has received $338,500 worth of pledges from 154 people and residents.

10.2. The Steering Committee has been actively engaging through advertising in local newsletters, letterboxing, a street presence and attending community meetings.

11. Delegation

11.1. This matter is delegated to the Council.

As signatory to this report, I certify that, pursuant to Section 55(1) of the Local Government Act 1993, I hold no interest, as referred to in Section 49 of the Local Government Act 1993, in matters contained in this report.

|

David Spinks Director Financial Services |

|

Date: 6 April 2017

File Reference: F17/33556

Attachment a: Report

of January 2016 ⇩ ![]()

Attachment

b: Catchment

Boundaries ⇩ ![]()

Attachment

c: SHFCB

Pledge Form ⇩ ![]()

|

Item No. 6.3 |

Agenda (Open Portion) Finance Committee Meeting |

Page 60 |

|

|

11/4/2017 |

|

6.3 Remissions of Rates and Charges Granted

File Ref: F17/31822; 22-2-2

Memorandum of the Group Manager Rates and Procurement and the Director Financial Services of 6 April 2017.

Delegation: Committee

|

Item No. 6.3 |

Agenda (Open Portion) Finance Committee Meeting |

Page 61 |

|

|

11/4/2017 |

|

Memorandum: Finance Committee

Remissions of Rates and Charges Granted

At its meeting on 26 April 2016, the Council resolved that pursuant to Section 22 of the Local Government Act 1993 (LG Act), the Council delegate its authority to grant a remission of all or part of any rates paid or payable by a ratepayer under Section 129 of the LG Act, to the General Manager, up to a limit of $2,000 per application.

The Council also resolved that a six-monthly report be provided for the information of the Finance Committee, detailing any remission of rates and charges granted under the General Manager’s delegation.

At its meeting on 18 October 2016, the Finance Committee received and noted a report detailing the remissions of rates and charges granted under the General Manager’s delegation for the period 26 April 2016 to 30 September 2016.

The six-monthly report for the period 1 October 2016 to 31 March 2017 shows that no remissions of rates and charges were granted under the General Manager’s delegation during the period.

|

That the information contained in

the memorandum of the Group Manager Rates and Procurement and the Director

Financial Services of 6 April 2017 titled “Remissions of Rates and

Charges Granted” be received and noted. |

As signatory to this report, I certify that, pursuant to Section 55(1) of the Local Government Act 1993, I hold no interest, as referred to in Section 49 of the Local Government Act 1993, in matters contained in this report.

|

Lara MacDonell Group Manager Rates and Procurement |

David Spinks Director Financial Services |

Date: 6 April 2017

File Reference: F17/31822; 22-2-2

|

Item No. 6.4 |

Agenda (Open Portion) Finance Committee Meeting |

Page 62 |

|

|

11/4/2017 |

|

6.4 Request for Extension of Lease - Telstra Telecommunication Tower - Sandown Park, Sandy Bay

File Ref: F17/34497; 5601657

Report of the Program Leader Recreation and Projects, the Manager Parks and Recreation and the Director Parks and City Amenity of 6 April 2017 and attachment.

This matter was also considered at the Parks and Recreation Committee meeting of 6 April 2017.

Delegation: Council

|

Item No. 6.4 |

Agenda (Open Portion) Finance Committee Meeting |

Page 63 |

|

|

11/4/2017 |

|

REPORT TITLE: Request for Extension of Lease - Telstra Telecommunication Tower - Sandown Park, Sandy Bay

REPORT PROVIDED BY: Program Leader Recreation and Projects

Manager Parks and Recreation

Director Parks and City Amenity

1. Report Purpose and Community Benefit

1.1. The purpose of the report is to consider a request from Telstra for a new lease over the site of its telecommunication tower and infrastructure located at Sandown Park in Sandy Bay.

1.2. Council considered this matter on 19 December 2016 and recommended that:

1. The City initiate community consultation, pursuant to Section 178 of the Local Government Act 1993, in response to a request from Telstra for a new lease over the site of its telecommunication tower and infrastructure located at Sandown Park, Sandy Bay.

2. Upon conclusion of the community engagement process, a further report be provided on the merit and terms of a proposed new lease for the site.

2. Report Summary

2.1. The Council considered a report in December 2016 discussing a request from Telstra for a new lease agreement over the existing tower at Sandown Park.

2.2. The Council provided approval for consultation to be undertaken as per the requirements of the Local Government Act 1993.

2.3. The consultation was completed in March 2017, where two submissions were received from nearby residents concerning the proposal to provide a new lease.

2.4. The report recommends the approval of a new lease to Telstra for a ten (10) year period, with two (2) further five (5) year terms.

|

That: 1. The Council approve a new lease to Telstra for the site of the telecommunications tower located at Sandown Park, Sandy Bay for a ten (10) year period with two (2) further five (5) year options. 2. The addition of any further infrastructure relating to the tower be considered by the Council at the time of application. 3. The General Manager be authorised to negotiate the terms of the new lease agreement. 4. Pursuant to Section 178 of the Local Government Act 1993, notice be provided of the Council’s decision, in writing and within 7 days of the decision, to those parties that lodged an objection including rights of appeal under the Act. |

4. Background

4.1. Telstra has made a request to extend their lease over the site of the tower at Sandown Park for a further ten (10) year period and have also requested two (2) further five (5) year options. A plan of the proposed lease area (Attachment A).

4.2. Council considered this matter on 19 December 2016 and recommended that:

1 The City initiate community consultation, pursuant to Section 178 of the Local Government Act 1993, in response to a request from Telstra for a new lease over the site of its telecommunication tower and infrastructure located at Sandown Park, Sandy Bay marked as Attachment A to item 6.3 of the Open Parks and Recreation Committee agenda of 8 December 2016.

2 Upon conclusion of the community engagement process, a further report be provided on the merit and terms of a proposed new lease for the site

4.3. Following this resolution, community engagement was initiated in March 2017 for a period of 3 weeks concluding on 20 March 2017.

4.4. It should be noted that the Council met all requirements for consultation under the Local Government Act and in addition sent letters to a number of residents.

4.5. Residents were advised of the proposal by:

4.5.1. Letters were sent to 71 nearby property owners.

4.5.2. Notices were placed in prominent locations on site.

4.5.3. Advertising in The Mercury newspaper.

4.6. At the conclusion of the consultation period two (2) submissions were received, these are summarised in the table below.

|

Response |

Comments |

|

1 – Nearby Resident |

Against the proposal on two grounds: 1) Nutgrove is a very popular area during weekends and public holidays. It is one of the most visited public spaces yet the existence of the Telstra Pole is ugly and ruins the ambiance and pleasure that visitors to the area seek. 2) The existence of low frequency electromagnetic energy may at this stage show no harm to humans but is concerned that the low exposure will be increased through more towers and modern devices, the accumulated affect may be harmful in the future. Suggested other sites be considered including Alexandra Battery (due to its elevation a lower tower could be considered), or the sand hills between Prossers and the Sailing Club. |

|

2- Nearby Resident |

Against the proposal Preference would be that the Council does not support the new lease as it would be better relocated away from residences due to the visual aspects and due to EMR (electromagnetic radiation). Second preference would be for the lease to be renewed but with restrictions on other companies adding further infrastructure to the pole. Is aware of the proposal from Optus/Vodafone to also add infrastructure to the pole. |

4.7. It is noted that both responses relate to the same issues around the visual impact of the pole, and the possible health effects through electromagnetic radiation (EMR).

4.8. The visual impact of the pole is a subjective view depending on the individual, whilst the pole is noticeable on site (it stands at 20m above the ground level) it is of similar height to the lighting towers on nearby Sandown Park (18 metres) and is obscured from some perspectives by large trees in the area.

4.9. EMR was the predominant concern from the community when the pole was first installed. The pole at the time of installation and at the current time meets the Australian Radiation Protection and Nuclear Safety Agency (ARPANSA) radiofrequency standard – the compliance with this standard is a requirement of the Australian Communications and Media Authority (ACMA) prior to installing a new tower, or upgrading any existing tower.

4.10. Most recent advice on EMR suggests that there is no scientific evidence regarding possible adverse health effects from base stations or antennas, this advice is supported by both the ARPANSA and the World Health Organisation.

4.11. It is noted one of the respondents suggest two alternative locations for relocation of the tower.

4.11.1. Alexandra Battery is not considered a suitable alternative to the current location. The writer raises concern of the current pole being within 100m of residences, however it is likely that a pole at this location would be closer to residences and would have more within 100m than the current site. There would also be likely heritage implications with any work on this site.

4.11.2. The suggestion of locating the pole to the sand hills between Prossers Restaurant and the Sandy Bay Sailing Club is also considered unviable. Whilst this location would move the infrastructure further away from residents, the infrastructure would require significant excavation to find a suitable base and due to erosion issues in the area this would not be a suitable option. It is also unlikely to be viable from an economic perspective from Telstra for this to occur.

4.12. If the lease was not to continue, and the pole was to be removed it would leave a significant gap in Telstra services in the area, which would create areas with unreliable reception or black spots where no reception was available.

4.13. It is known that Optus/Vodafone are planning to make a request to Telstra to add some additional antennas to the pole as well as some cabinets at the rear of the existing pavilion. Whilst the addition of antennas will be subject to an agreement between Telstra and Optus/Vodafone, the Council will need to consider a request for lease for the location of the cabinets. Any lease will also be subject to the consultation requirements under Section 178 of the Local Government Act. As such the extension of the lease could be approved; however any additional infrastructure would need the Council consideration.

5. Proposal and Implementation

5.1. It is proposed that the Council approve a new lease to Telstra for the site of the telecommunications tower located at Sandown Park for a ten (10) year period with two (2) further five (5) year options.

5.2. It is proposed that the addition of any further infrastructure relating to the pole be considered by the Council at the time of application, noting that ‘low impact’ facilities can be added to existing infrastructure without planning approvals or landowner consent.

5.3. Pursuant to Section 178 of the Local Government Act 1993, notice be provided of the Council’s decision, in writing and within 7 days of the decision, to those parties that lodged an objection including rights of appeal under the Act.

6. Strategic Planning and Policy Considerations

6.1. The proposal is line with

the Capital City Strategic Plan 2015-2025, Strategic Objective 2.3:

City and regional planning ensures quality design, meets community needs and

maintains residential amenity.

7. Financial Implications

7.1. Funding Source and Impact on Current Year Operating Result

7.1.1. A valuation of the leased area has been completed and an annual rental of $6,600 exc GST has been recommended for the site.

7.1.2. Should a lease be approved this will result in an additional $6,600 exc income per annum.

7.2. Impact on Future Years’ Financial Result

7.2.1. The lease rental will increase by CPI each year.

7.3. Asset Related Implications

7.3.1. There are no asset related items – all assets within the lease area will be the responsibility of Telstra.

8. Legal, Risk and Legislative Considerations

8.1. A new lease agreement will be developed by the City’s Legal Services Officer.

8.2. Section 178 of the Local

Government Act 1993 outlines the process the Council must abide when

seeking to dispose (including lease) Public Land.

Should the Council resolve to lease the portion of land, notice will be

provided, in writing and within 7 days of the decision, to those that lodges an

objection including their rights of appeal.

9. Environmental Considerations

9.1. There has been much debate about the potential health effects of electromagnetic radiation from towers such as the one which is the subject of this application. Advice from Telstra is that the current facility complies with the relevant Standard and there is no substantiated evidence of negative health effects.

10. Social and Customer Considerations

10.1. It is considered that the proposed extension of the lease will generate community interest. However it does need to be noted that if this pole and associated infrastructure were to be removed it would reduce the capacity for the provision of a high quality telecommunications service usage that meets customer requirements and may result in additional “black spots” or mobile telephone reception being non existent.

11. Community and Stakeholder Engagement

11.1. As noted earlier in the report the Council has exceeded its obligations under the Local Government Act.

12. Delegation

12.1. This matter is delegated to the Council.

As signatory to this report, I certify that, pursuant to Section 55(1) of the Local Government Act 1993, I hold no interest, as referred to in Section 49 of the Local Government Act 1993, in matters contained in this report.

|

Shannon Avery Program Leader Recreation and Projects |

Simon Harrison Manager Parks and Recreation |

|

Glenn Doyle Director Parks and City Amenity |

|

Date: 6 April 2017

File Reference: F17/34497; 5601657

Attachment a: Site

Plan - Lease Area ⇩ ![]()

|

Agenda (Open Portion) Finance Committee Meeting |

Page 70 |

|

|

|

11/4/2017 |

|

A report indicating the status of current decisions is attached for the information of Aldermen.

REcommendation

That the information be received and noted.

Delegation: Committee

|

Agenda (Open Portion) Finance Committee Meeting |

Page 79 |

|

|

|

11/4/2017 |

|

Regulation 29(3) Local Government

(Meeting Procedures) Regulations 2015.

File Ref: 13-1-10

The General Manager reports:-

“In accordance with the procedures approved in respect to Questions Without Notice, the following responses to questions taken on notice are provided to the Committee for information.

The Committee is reminded that in accordance with Regulation 29(3) of the Local Government (Meeting Procedures) Regulations 2015, the Chairman is not to allow discussion or debate on either the question or the response.”

8.1 Parking Compliance Issues - 54 King Street, Sandy Bay

File Ref: F17/15341

Memorandum of the Group Manager Parking Operations of 6 April 2017.

Delegation: Committee

|

That the information be received and noted.

|

|

Item No. 8.1 |

Agenda (Open Portion) Finance Committee Meeting |

Page 80 |

|

|

11/4/2017 |

|

Memorandum: Lord Mayor

Deputy Lord Mayor

Aldermen

Response to Question Without Notice

Parking Compliance Issues - 54 King Street, Sandy Bay

|

Meeting: City Planning Committee

|

Meeting date: 14 February 2017

|

|

Raised by: Alderman Burnet |

|

Question:

Can compliance with on-street parking requirements near 54 King Street, Sandy Bay be investigated?

Response:

The parking area immediately outside of number 54 King Street, which is the northern side of the street, is controlled by permissive parking signage, with a time limit of 30 minutes. The 30 minute parking zone extends from Sandy Bay Road through to Grosvenor Street.

The opposite side of King Street (southern side) is all a no parking zone, which also extends through to Grosvenor Street. Following Grosvenor both sides of King Street become a 2 hour residents excepted zones.

King Street is included in the designated patrol area for Councils Parking Officers. In the past 3 months, 4 infringements have been issued in the 30 minute zones and a further 29 in the 2 hour zones. Parking Operations relies on public complaints in order to strategically deploy our patrols so as to concentrate on specific problem areas.

As a result of this request the frequency of patrols in King Street, particularly between Sandy Bay Road and Grosvenor Street have been increased.

As signatory to this report, I certify that, pursuant to Section 55(1) of the Local Government Act 1993, I hold no interest, as referred to in Section 49 of the Local Government Act 1993, in matters contained in this report.

|

Matthew Tyrrell Group Manager Parking Operations |

|

Date: 6 April 2017

File Reference: F17/15341

|

|

Agenda (Open Portion) Finance Committee Meeting |

Page 82 |

|

|

11/4/2017 |

|

Section 29 of the Local Government (Meeting Procedures) Regulations 2015.

File Ref: 13-1-10

An Alderman may ask a question without notice of the Chairman, another Alderman, the General Manager or the General Manager’s representative, in line with the following procedures:

1. The Chairman will refuse to accept a question without notice if it does not relate to the Terms of Reference of the Council committee at which it is asked.

2. In putting a question without notice, an Alderman must not:

(i) offer an argument or opinion; or

(ii) draw any inferences or make any imputations – except so far as may be necessary to explain the question.

3. The Chairman must not permit any debate of a question without notice or its answer.

4. The Chairman, Aldermen, General Manager or General Manager’s representative who is asked a question may decline to answer the question, if in the opinion of the respondent it is considered inappropriate due to its being unclear, insulting or improper.

5. The Chairman may require a question to be put in writing.

6. Where a question without notice is asked and answered at a meeting, both the question and the response will be recorded in the minutes of that meeting.

7. Where a response is not able to be provided at the meeting, the question will be taken on notice and

(i) the minutes of the meeting at which the question is asked will record the question and the fact that it has been taken on notice.

(ii) a written response will be provided to all Aldermen, at the appropriate time.

(iii) upon the answer to the question being circulated to Aldermen, both the question and the answer will be listed on the agenda for the next available ordinary meeting of the committee at which it was asked, where it will be listed for noting purposes only.

|

|

Agenda (Open Portion) Finance Committee Meeting |

Page 83 |

|

|

11/4/2017 |

|