City

of hobart

AGENDA

Finance Committee Meeting

Open Portion

Tuesday, 13 December 2016

at 5:00 pm

Lady Osborne Room, Town Hall

City

of hobart

AGENDA

Finance Committee Meeting

Open Portion

Tuesday, 13 December 2016

at 5:00 pm

Lady Osborne Room, Town Hall

THE MISSION

Our mission is to ensure good governance of our capital City.

THE VALUES

The Council is:

|

about people |

We value people – our community, our customers and colleagues. |

|

professional |

We take pride in our work. |

|

enterprising |

We look for ways to create value. |

|

responsive |

We’re accessible and focused on service. |

|

inclusive |

We respect diversity in people and ideas. |

|

making a difference |

We recognise that everything we do shapes Hobart’s future. |

|

|

Agenda (Open Portion) Finance Committee Meeting |

Page 3 |

|

|

13/12/2016 |

|

Business listed on the agenda is to be conducted in the order in which it is set out, unless the committee by simple majority determines otherwise.

APOLOGIES AND LEAVE OF ABSENCE

1. Co-Option of a Committee Member in the event of a vacancy

3. Consideration of Supplementary Items

4. Indications of Pecuniary and Conflicts of Interest.

6.1 Remissions and General Assistance Available to Ratepayers

6.2 Annual Review of Loan and Investment Portfolios - November 2016

6.3 Outstanding Long Term Parking Debts as at 30 November 2016

7 Committee Action Status Report

7.1 Committee Actions - Status Report

8. Responses to Questions Without Notice

8.1 State Government Support Funding for the Taste of Tasmania

10. Closed Portion Of The Meeting

|

|

Agenda (Open Portion) Finance Committee Meeting |

Page 5 |

|

|

13/12/2016 |

|

Finance Committee Meeting (Open Portion) held Tuesday, 13 December 2016 at 5:00 pm in the Lady Osborne Room, Town Hall.

|

COMMITTEE MEMBERS Thomas (Chairman) Deputy Lord Mayor Christie Zucco Ruzicka Sexton

APOLOGIES:

LEAVE OF ABSENCE: Nil.

|

ALDERMEN Lord Mayor Hickey Briscoe Burnet Cocker Reynolds Denison Harvey |

|

The minutes of the Open Portion of the Finance Committee meeting held on Tuesday, 15 November 2016, are submitted for confirming as an accurate record.

|

Ref: Part 2, Regulation 8(6) of the Local Government (Meeting Procedures) Regulations 2015.

|

That the Committee resolve to deal with any supplementary items not appearing on the agenda, as reported by the General Manager.

|

Ref: Part 2, Regulation 8(7) of the Local Government (Meeting Procedures) Regulations 2015.

Aldermen are requested to indicate where they may have any pecuniary or conflict of interest in respect to any matter appearing on the agenda, or any supplementary item to the agenda, which the committee has resolved to deal with.

Regulation 15 of the Local Government (Meeting Procedures) Regulations 2015.

A committee may close a part of a meeting to the public where a matter to be discussed falls within 15(2) of the above regulations.

In the event that the committee transfer an item to the closed portion, the reasons for doing so should be stated.

Are there any items which should be transferred from this agenda to the closed portion of the agenda, or from the closed to the open portion of the agenda?

|

Agenda (Open Portion) Finance Committee Meeting |

Page 6 |

|

|

|

13/12/2016 |

|

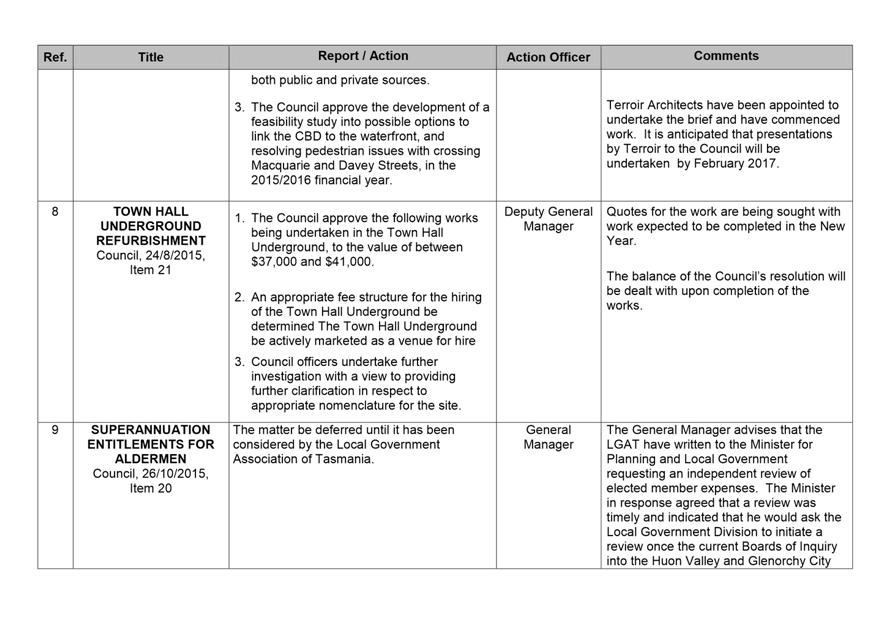

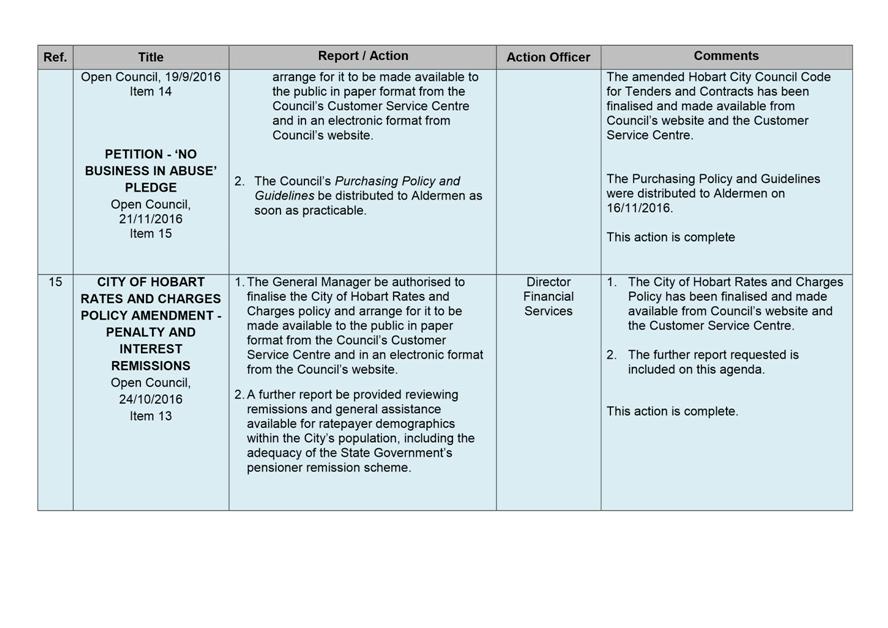

6.1 Remissions and General Assistance Available to Ratepayers

File Ref: F16/125850; 22-2-1

Report of the Group Manager Rates and Procurement and the Director Financial Services of 6 December 2016 and attachments.

Delegation: Council

|

Item No. 6.1 |

Agenda (Open Portion) Finance Committee Meeting |

Page 8 |

|

|

13/12/2016 |

|

REPORT TITLE: Remissions and General Assistance Available to Ratepayers

REPORT PROVIDED BY: Group Manager Rates and Procurement

Director Financial Services

1. Report Purpose and Community Benefit

1.1. The purpose of this report is to provide information reviewing the remissions and general assistance available for ratepayer demographics within the City’s population, including the adequacy of the State Government’s pensioner remission scheme as requested by Council at its meeting on 24 October 2016.

1.2. Knowledge of assistance available to the City’s ratepayers provides broad community benefit.

2. Report Summary

2.1. At its meeting on 24 October 2016 the Council resolved that a report be provided reviewing remissions and general assistance available for ratepayer demographics within the City’s population, including the adequacy of the State Government’s pensioner remission scheme.

2.2. The Council currently provides a range of assistance to ratepayers in need of assistance or support, including payment arrangements, rate postponements, rates exemptions and rate remissions.

2.3. The State Government provides a pensioner rates remission scheme to eligible pensioners under the Local Government (Rates and Charges Remissions) Act 1991. It also provides over 90 concessions and discounts to Tasmanians in need of assistance and support.

2.4. This report reviews the different types of assistance and support available to all ratepayers in the Hobart municipal area.

|

That: 1. The Council write to the State Government seeking a review of the adequacy of the defined maximum annual rate remissions provided under the Local Government (Rates and Charges Remissions) Act 1991.

|

4. Background

4.1. At its meeting on 24 October 2016 Council resolved the following:

4.1.1. The Council adopt the City of Hobart Rates and Charges policy marked as Attachment A to item 6.2 of the Open Finance Committee agenda of 18 October 2016.

4.1.2. The General Manager be authorised to finalise the City of Hobart Rates and Charges policy and arrange for it to be made available to the public in paper format from the Council’s Customer Service Centre and in an electronic format from the Council’s website.

4.1.3. A further report be provided reviewing remissions and general assistance available for ratepayer demographics within the City’s population, including the adequacy of the State Government’s pensioner remission scheme.

4.2. The City of Hobart Rates and Charges Policy has been finalised and made available from Council’s website and in print from the Customer Service Centre. This report addresses the Council resolution at Section 4.1.3 above.

4.3. The Council currently provides a range of assistance to any / all ratepayers (ratepayer demographics) in need of assistance or support, including payment arrangements, rate postponements, rates exemptions and rate remissions. These are described in detail below and can be summarised as follows:

|

Concession Type |

Eligibility Criteria |

Concession |

Ratepayer Demographic |

|

Hardship Payment Arrangement |

Any ratepayer in financial hardship |

Temporary reduced payments or payments spread over longer time periods |

All |

|

Rate Postponement |

Outlined in Council Policy – Attach A |

50% annual rates postponed for the lifetime of the applicant or until sale of property takes place. Interest rate of 5% payable on principle only. |

Pensioners |

|

General Rate exemption |

Outlined in section 87 of LG Act – Attach B |

100% rebate of General Rate |

Prescribed land types |

|

Fire Service Rate exemption |

Outlined in section 78 of Fire Services Act 1979 - Attach D |

100% rebate of Fire Service Rate |

Prescribed property types |

|

Remission of Storm water Removal Service Rate |

Property does not receive a storm water service from Council |

100% remission of Storm water Service Rate |

500 properties in rural / remote areas |

|

Remission of Waste Management Service Charge |

Property does not receive a standard garbage collection service from Council |

100% remission of Waste Management Service Charge and Landfill Rehabilitation Service Charge |

1000 properties – mainly vacant land |

|

Natural Gas Rebate |

For natural gas appliances purchased as a part of a household connecting to the natural gas network |

$250 per annum |

All |

|

Native Vegetation Rebate |

Discounted rates for private properties where areas of native vegetation with significant biodiversity values are formally and voluntarily protected |

$6.04 per hectare with a minimum rebate of $60.40 per property, maximum rebate of $604 per property |

All |

|

State Government Pensioner Remission |

Determined by Department of Treasury and Finance |

30% off annual rates capped at $292 if also a TasWater customer or $430 if not (2016/17 figures) 20% off Fire Service Rate (provided by State Fire Commission, no cap) |

Pensioners |

|

Council Pensioner Remission |

Pensioners eligible for the State Government pensioner remission above plus self funded retirees |

10%. By policy decision, the state government maximum and Council remission are linked and together, capped at $302. Effectively, pensioners receive $10 from Council. |

Pensioners (including self funded retirees) |

Hardship Payment Arrangements

4.4. Under Council Policy Collection of Rates Arrears, in response to approaches by ratepayers who have difficulty in meeting scheduled payments, suitable arrangement for payments are considered and entered into.

4.5. Council’s Rates Officers work with ratepayers to manage arrears, particularly in times of financial hardship.

4.6. Rates Officers are also aware of general assistance available from the State Government to help Tasmanians with the cost of living.

Rate Postponements

4.7. Pursuant to Section 125 of the Local Government Act 1993 (LG Act) a ratepayer may apply to the council for a postponement of payment of rates on the ground of hardship.

4.8. Section 126 of the LG Act states that the conditions of postponement are as follows:

4.8.1. (1) A council may grant a postponement of the payment of rates for a specified period if satisfied that such payment would cause hardship.

4.8.2. (2) A council may grant a postponement of payment of rates –

4.8.2.1. (a) on the condition that the ratepayer pay interest on the amount of rates postponed at a rate fixed by the council; and

4.8.2.2. (b) on any other condition the council determines.

4.8.3. (3) Interest fixed under subsection (2)(a) is not to exceed the prescribed percentage as calculated in section 128(2).

4.9. The Council has adopted a policy on Rate Postponements – refer Attachment A.

4.10. Council’s policy on rate postponements has traditionally been linked to older Australians who qualify for the pensioner remission on specified conditions and on the condition that:

4.10.1. (i) The amount to be postponed in any year to be the amount requested by the applicant but not exceeding 50% of the amount payable in that year.

4.10.2. (ii) The period of postponement to be for the lifetime of the applicant or, should the property be sold during the applicant’s lifetime, until the sale takes place, whereupon the amount will be due and payable.

4.10.3. (iii) An interest rate of 5% shall be payable on the amount subject to postponement, and be payable on the same terms as the amount deferred, namely death or sale of the property, and interest be charged on the principle only.

4.11. Postponed rates as at 30 June 2016 totalled $90,653.

Rate Exemptions

4.12. Section 87 of the LG Act sets out the exemptions from [effectively] General Rates – refer Attachment B.

4.13. The exemptions within S87 of the LG Act are generally read as being limited to circumstances where there is a public benefit, rather than circumstances where there is purely a commercial or private benefit.

4.14. In April 2015 the Council approved a new policy, Rates Exemption – Charitable Purposes, that outlines the Council’s approach to assessing whether land falls within the charitable exemption of Section 87(1)(d) of the LG Act – refer Attachment C.

4.15. Section 78 of the Fire Services Act 1979 permits the exemption of the Fire Service Rate in certain circumstances – refer Attachment D. It should be noted that the City of Hobart collects the Fire Service Rate on behalf of the Tasmanian Government and passes it onto the Tasmania Fire Service.

Rate Remissions

4.16. Rate remissions are generally provided for under Section 129 of the LG Act, which states that:

(1) A ratepayer may apply to the council for remission of all or part of any rates paid or payable by the ratepayer or any penalty imposed or interest charged under section 128.

(2) An application is to be –

(a) made in writing; and

(b) lodged with the general manager.

(3) A council, by absolute majority, may grant a remission of all or part of any rates, penalty or interest paid or payable by the ratepayer.

(4) A council, by absolute majority, may grant a remission of any rates, penalty or interest paid or payable by a class of ratepayers.

(5) The general manager is to keep a record of the details of any remission granted under this section.

4.17. The Council has delegated to the General Manager the power to consider rate remission requests up to $2,000. Rate remission requests over $2,000 are considered by the Council.

4.18. The Council currently provides the following rate remissions to eligible ratepayers:

4.18.1. Remission of the Storm water Removal Service Rate and/or Waste Management Service Charge under Council Policy Rate Remissions – Service Rates/Charges, which states that pursuant to Section 129 of the LG Act, a property shall only receive a remission of the storm water and/or waste management service charge in the event that:

4.18.1.1. The property does not receive and is not capable of receiving a standard garbage collection service or a storm water service from the Council whatsoever; and

4.18.1.2. Even if the property were capable of receiving such a service, any request to Council for such a service would be denied.

4.18.2. 500 properties currently receive the storm water removal service rate remission and approximately 1000 properties receive a waste management service charge remission, which includes vacant land and council owned properties.

4.18.3. E. Kalis Properties Pty Ltd receives a remission of rates under a Development Assistance Deed for the redevelopment of the former Myer site.

4.18.4. Sultan Holdings Pty Ltd receives a remission of rates under a Development Agreement for the Argyle Street Carpark Redevelopment project.

4.18.5. Natural gas rebate. Forty properties received a $250 rebate in 2015/2016, which was deducted from the rates levied on the property.

4.18.6. Rate rebate for native vegetation protection. Council offers rates rebates for landowners who voluntarily protect native vegetation with significant conservation values. The annual rates rebate is $6.04 per hectare with a minimum rebate of $60.40 per property and a maximum rebate of $604 per property. A small number of properties currently receive this rebate.

Rate Remission Policies

4.19. The LG Act is silent on the grounds for a remission of rates or the grounds for a decision by the Council to grant a remission. Rate remission requests are considered on a case by case basis, by examining the relevant facts of the matter and making decisions pursuant to the City of Hobart Rates and Charges Policy.

4.20. Most Tasmanian Councils do not have a separate policy regarding S129 of the LG Act, rather councils include a policy statement in their general rates and charges policy that ratepayers can apply for a rates remission under Section 129 of the LG Act and how to do so, as prescribed under that part. This is the City of Hobart’s approach.

4.21. The Launceston City Council (LCC) is an exception. LCC has adopted a policy position to explain its approach to rating exemptions and remissions for charitable organisations – refer Attachment E.

State Government Pensioner Rate Remission Scheme

4.22. Pensioners eligible for assistance under the Local Government (Rates and Charges Remission) Act 1991 may receive a rates remission. Eligibility of a pensioner remission and eligibility criteria is determined by the State Government – Department of Treasury and Finance.

4.23. In order to be eligible for the pensioner remission the applicant must be liable to pay the rates on the property that they occupy as their principal place of residence as at 1 July of the financial year to which the rates relate.

4.24. Pursuant to Section 120 of the LG Act, the owner is taken to be liable for the rates of a property. Ownership is normally determined by reference to the title of the property to which the rates relate. In the example of an independent living unit resident, they would not be the owner of the independent unit and hence not liable for the rates of the property.

4.25. However, under Section 120(2) of the LG Act, the occupier of the land may, with the written consent of the owner, decide to accept liability for the payment of the rates. In these cases, the occupier must provide a copy of the written agreement to notify the council’s General Manager in accordance with Section 120(3) of the LG Act.

4.26. A pensioner remission is available to pensioners who hold one of three types of cards issued by either Centrelink of Department of Veterans Affairs:

4.26.1. Pensioner Concession Card – issued by Centrelink and Department of Veterans Affairs

4.26.2. Centrelink Health Care Card

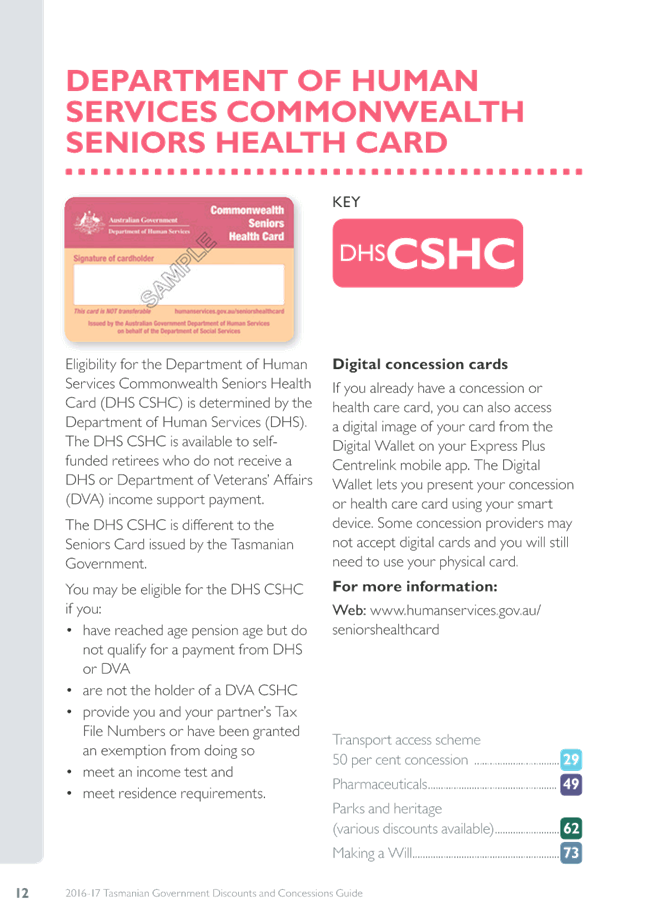

4.26.3. Repatriation Health Card – i.e. ‘Gold Card’ endorsed Total or Permanent Injury (TPI) or War Widow/Widower DVA.

4.27. An Australian Government Seniors Health Card does not qualify the holder for a rates remission.

4.28. Eligible pensioners are entitled to:

4.28.1. A 30% remission of their rates up to a maximum limit. For 2016/2017 this was $292 for those pensioners also a customer of TasWater and $430 for pensioners not a customer of TasWater. This is reimbursed to Council by the State Government.

4.28.2. A 20% remission off the Fire Service Rate pursuant to section 95 of the Fire Service Act 1979. There are no maximum limits. This is reimbursed to Council by the State Fire Commission.

4.29. There is a limit of one remission per year per pensioner household. A pensioner who is a multiple property holder is not entitled, to receive more than one remission per year.

4.30. The State Government allow retrospective claims for the prior year to be paid to eligible pensioners.

Council pensioner remission policy

4.31. Council currently funds a 10% remission to all pensioners including holders of the Seniors Health Card who don’t qualify for the State Government pensioner remission. The Council remission, by policy decision, is linked to the state government maximum such that the two remissions combined, are capped at $302. The state government maximum of $292 cuts in at quite a low AAV value meaning all eligible ratepayers receive the maximum. Accordingly, all receive a $10 remission from Council.

4.32. Approximately 12.5% of all ratepayers in the Hobart municipal area receive a pensioner rates remission at a cost of $1.1M per annum funded by the State Government.

4.33. 13.3% of all ratepayers in the Hobart municipal area receive the Council $10 rates remission, which includes self funded retirees not otherwise eligible for the State Government pensioner rates remission, at a cost of $31,830 to the Council as at 30 June 2016.

General Assistance

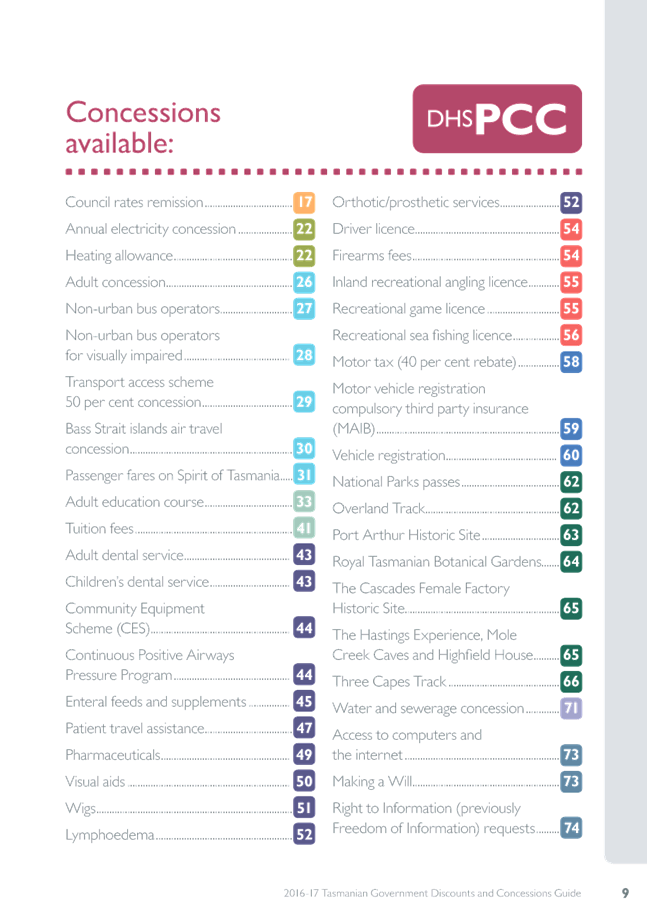

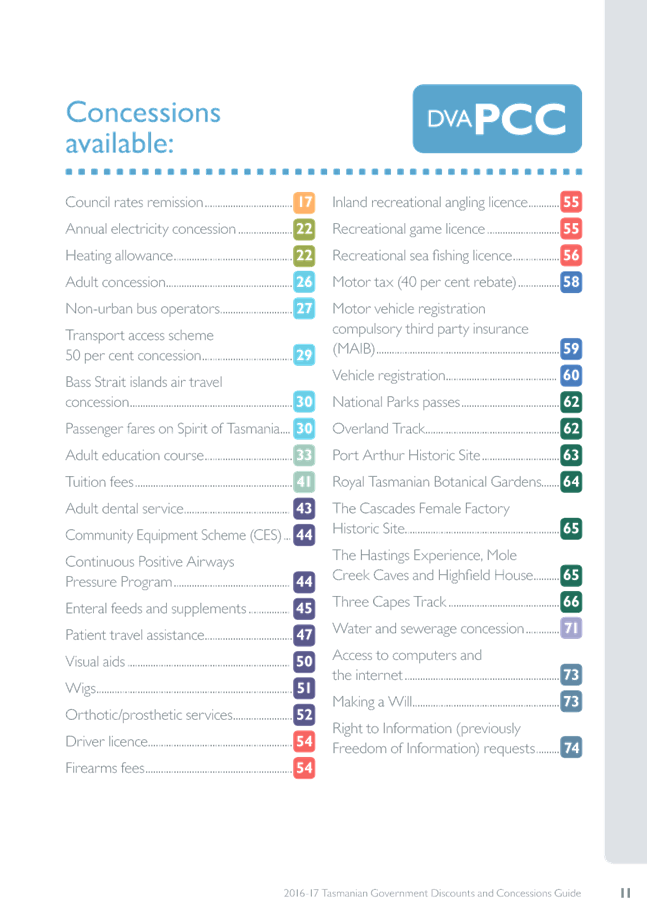

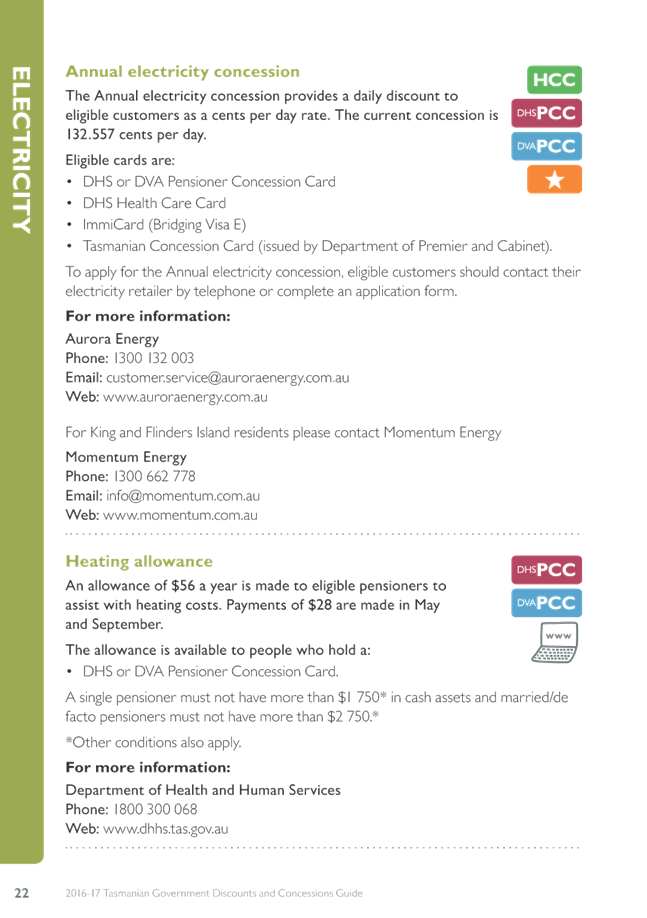

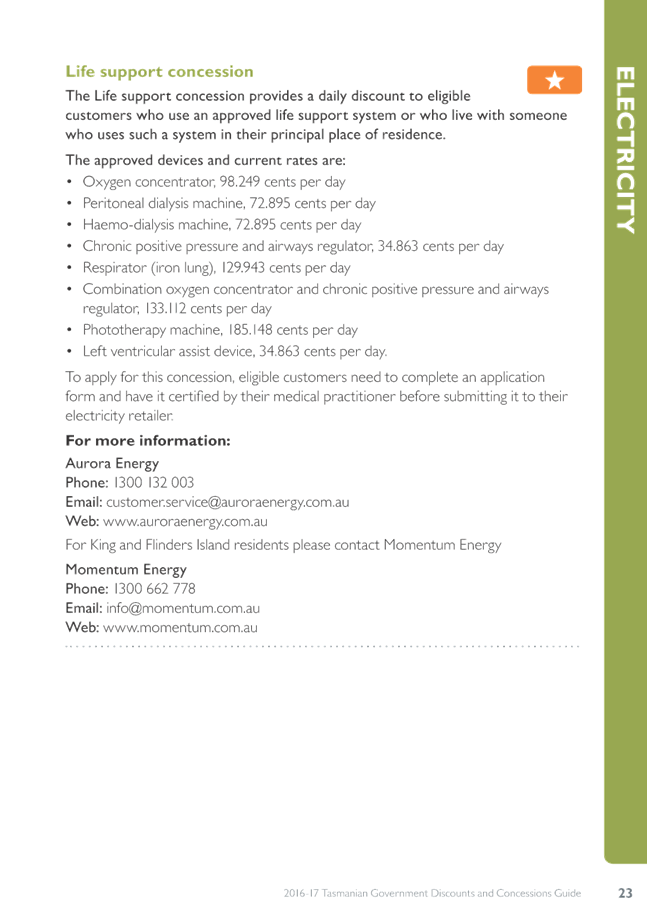

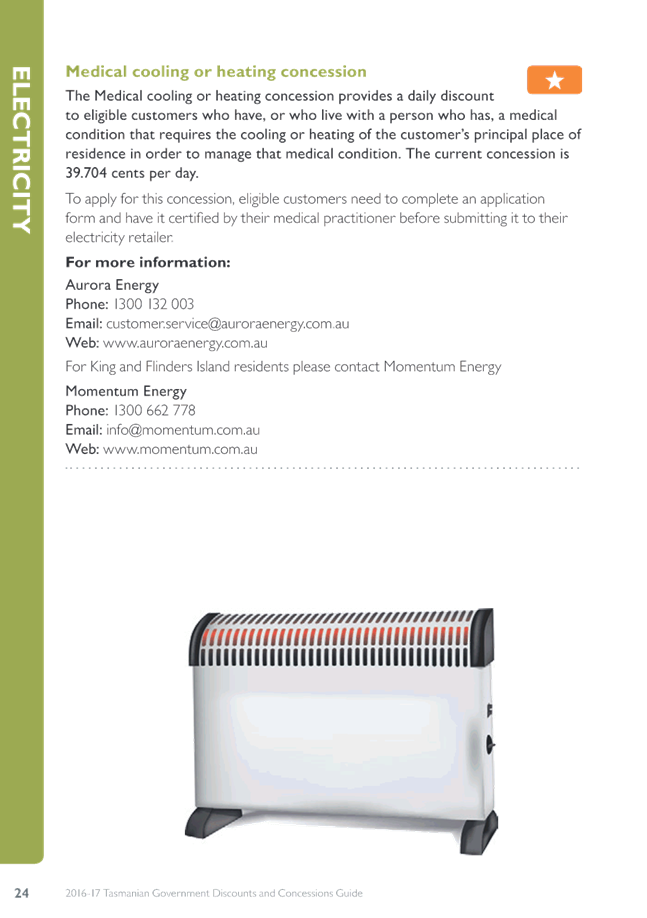

4.34. The Tasmanian Government offers a wide range of discounts and concessions to eligible Tasmanians on a wide range of services such as housing, transport, electricity, water and sewerage, heating, education, event attendance, entries to national parks and health services to assist those experiencing hardship and in need of support in the community.

4.35. The State Government produce a Guide detailing over 90 concessions available to eligible persons in Tasmania. The 2016-17 Tasmanian Government Discounts and Concession Guide is attached – refer Attachment F.

Adequacy of the Pensioner Remission

4.36. It is difficult to determine the adequacy of the State Government pensioner remission scheme. Taking the approach of comparing the assistance provided by other councils to that provided by the City of Hobart is also difficult because the legislative environment in which councils in other states / territories and outside of Australia vary to that of Tasmania. Councils’ funding models also vary with some councils relying more heavily on rates, rather than grants, than others.

4.37. In 2016-2017 it will cost the State Government $16.736M to fund the pensioner rates remission scheme. The State Government’s Forward Estimates show this increasing to $17.166M in 2017-18, $17,607M in 2018-19 and $18.060M in 2019-20.

4.38. Funding constraints and a need for concessions to other groups are likely reasons the pensioner remission scheme is capped at a maximum remission as outlined in section 4.40 below.

4.39. However, it should be noted that the maximum remission is indexed annually to ensure that rate relief increase in line with inflation.

4.40. The 30% remission is capped at either $292 or $430 for 2016/17 varying depending whether you are a customer of TasWater or not. Most of the City’s pensioners are a customer of TasWater. All of the City’s eligible pensioners receive the maximum capped remission. The 20% remission of the Fire Service Rate isn’t capped and all eligible pensioners receive the 20% remission off the Fire Service Rate.

4.41. For an average residential ratepayer (with an AAV of $20,441 and an annual rates bill of $2,218.50) who is also a customer of TasWater the pensioner rates remission equals $354.74 off the annual rates bill, which includes the $10 council concession.

4.42. As noted above, the state government maximum of $292 cuts in at quite a low AAV value meaning all eligible ratepayers receive the maximum of $292. Accordingly, all receive a $10 remission from Council.

4.43. Rates are a form of tax as outlined in Section 86A(1) of the LG Act, which states that:

4.44. In …. making decisions concerning the making of rates, Council has taken into account the following pursuant to section 86A(1) of the LG Act:

4.44.1. (a) rates constitute taxation for the purposes of local government, rather than a fee for a service; and

4.44.2. (b) the value of rateable land is an indicator of the capacity of the ratepayer in respect of that land to pay rates.

4.45. Council rates are based on property values and are therefore a property tax. Generally the Act expects that the higher the value of the property the higher the rates to be paid.

4.46. The LG Act therefore contemplates that the amount of rates you pay will be determined by the value of your property. It is therefore arguable that rates, being a tax system, could be used, as an example, to provide welfare support to individual owners or groups of owners. Particularly in the context that any support provided to an individual owner or group of owners is paid for by every other ratepayer in the form of increased rates. Albeit the effect will vary dependent upon the quantum of rate remission provided.

4.47. Therefore, providing rate remissions on the grounds of financial hardship may not lead to a desirable outcome for the City and the City has other means to provide support to ratepayers who find themselves in financial hardship.

4.48. There is, however, a community benefit in providing assistance through rating relief to certain organisations where a benefit to the community can be established. Usually, these types of organisations are covered by rate exemption provisions under Section 87 of the LG Act.

5. Proposal and Implementation

5.1. It is proposed that the Committee note the remissions and general assistance available to ratepayers within the Hobart municipal area.

5.2. Given the difficulty of assessing the adequacy of the State Government pensioner remission scheme, it is proposed that Council write to the State Government seeking a review of the adequacy of the defined maximum annual rate remissions provided under the Local Government (Rates and Charges Remissions) Act 1991. It is noted that the amount is indexed each year to keep in line with inflation.

5.3. Council may also wish to review its pensioner remission policy given all eligible pensioners only receive $10 from Council. There would be financial implications of this – refer Section 7.

6. Strategic Planning and Policy Considerations

6.1. This report relates to Council’s Rates and Charges Policies, including:

6.1.1. Collection of Rates Arrears.

6.1.2. Rates Exemption – Charitable Purposes.

6.1.3. Rate Postponements.

6.1.4. Rate Remissions – Services Rates-Charges.

6.1.5. Rates Remissions.

6.2. This report also relates to the City of Hobart Rates and Charges Policy, which outlines Council’s policy position on rate rebates, rate remissions and payments as outlined in Section 4 above.

7. Financial Implications

7.1. Funding Source and Impact on Current Year Operating Result

7.1.1. There are no financial implications arising from this report as this report has been provided for information purposes and rates have already been levied for 2016/2017.

7.1.2. However, rate remissions granted in 2016/2017 would be unfunded and would decrease Council’s budgeted operating surplus for 2016/2017.

7.2. Impact on Future Years’ Financial Result

7.2.1. Any increase in the pensioner concession provided by Council would need to be funded from budget estimates in the year provided and future years if Council resolved to do so.

7.2.2. There would be no impact on future years’ financial result from any increase in rate remissions as Council will simply set the budget for the amount of rates it needs to raise (in other words, there would be an offsetting increase in rates to fund any additional remission provided). However, granting a remission to some ratepayers means that other ratepayers will need to pay more in rates, effectively subsidising the remission, albeit the effect will be minor for individual ratepayers.

7.3. Asset Related Implications

7.3.1. Not applicable.

7.4. It should be noted that the City’s rates arrears are, by industry standards, very low. As at 30 June 2016 gross rates outstanding expressed as a percentage of annual rate revenue was 1.20%, the lowest figure since 30 June 2010 (which was the lowest figure for at least 20 years). The 2015/16 state average was 4.5% (source: draft Auditor-General report to Parliament).

8. Legal, Risk and Legislative Considerations

8.1. These have been considered elsewhere in the report.

9. Delegation

9.1. This matter is delegated to the Council.

As signatory to this report, I certify that, pursuant to Section 55(1) of the Local Government Act 1993, I hold no interest, as referred to in Section 49 of the Local Government Act 1993, in matters contained in this report.

|

Lara MacDonell Group Manager Rates and Procurement |

David Spinks Director Financial Services |

Date: 6 December 2016

File Reference: F16/125850; 22-2-1

Attachment a: Council

Policy Rate Postponements ⇩ ![]()

Attachment

b: Section

87 - Local Government Act 1993 ⇩ ![]()

Attachment

c: Council

Policy Rates Exemption - Charitable Purposes ⇩ ![]()

Attachment

d: Section

78 - Fire Service Act 1979 ⇩ ![]()

Attachment

e: Launceston

City Council Policy Rate Remissions and Rebates ⇩ ![]()

Attachment

f: Tasmanian

Government Concessions Guide 2016-17 ⇩ ![]()

|

Agenda (Open Portion) Finance Committee Meeting - 13/12/2016 |

Page 21 ATTACHMENT b |

LOCAL GOVERNMENT ACT 1993 - SECT 87

87. Exemption from rates

(1) All land is rateable except that the following are exempt from general and separate rates, averaged area rates, and any rate collected under section 88 or 97:

(a) land owned and occupied exclusively by the Commonwealth;

(b) land held or owned by the Crown that –

(i) is a national park, within the meaning of the Nature Conservation Act 2002; or

(ii) is a conservation area, within the meaning of the Nature Conservation Act 2002; or

(iii) is a nature recreation area, within the meaning of the Nature Conservation Act 2002; or

(iv) is a nature reserve, within the meaning of the Nature Conservation Act 2002; or

(v) is a regional reserve, within the meaning of the Nature Conservation Act 2002; or

(vi) is a State reserve, within the meaning of the Nature Conservation Act 2002; or

(vii) is a game reserve, within the meaning of the Nature Conservation Act 2002; or

(viii) . . . . . . . .

(ix) is a public reserve, within the meaning of the Crown Lands Act 1976; or

(x) is a public park used for recreational purposes and for which free public access is normally provided; or

(xi) is a road, within the meaning of the Roads and Jetties Act 1935; or

(xii) is a way, within the meaning of the Local Government (Highways) Act 1982; or

(xiii) is a marine facility, within the meaning of the Marine and Safety Authority Act 1997; or

(xiv) supports a running line and siding within the meaning of the Rail Safety National Law (Tasmania) Act 2012;

(c) land owned by the Hydro-Electric Corporation or land owned by a subsidiary, within the meaning of the Government Business Enterprises Act 1995, of the Hydro-Electric Corporation on which assets or operations relating to electricity infrastructure, within the meaning of the Hydro-Electric Corporation Act 1995, other than wind-power developments, are located;

(d) land or part of land owned and occupied exclusively for charitable purposes;

(da) Aboriginal land, within the meaning of the Aboriginal Lands Act 1995, which is used principally for Aboriginal cultural purposes;

(e) land or part of land owned and occupied exclusively by a council.

(2) The owner of any land referred to in subsection (1) may agree to pay general or separate rates or an averaged area rate.

(3) Land occupied by a joint authority or single authority to which Part 3A applies is not exempt from rates or averaged area rates.

(4) . . . . . . . .

|

Agenda (Open Portion) Finance Committee Meeting - 13/12/2016 |

Page 30 ATTACHMENT d |

78. Application of Division

(1) Except as provided in subsection (2), this Division does not apply to or in respect of –

(a) land owned by a local council; or

(b) land owned by the Crown in right of this State; or

(ba) Aboriginal land, within the meaning of the Aboriginal Lands Act 1995, which is unoccupied or occupied principally for Aboriginal cultural purposes; or

(bb) land owned, vested in or occupied by a GBE that is not specified in Schedule 8 to the Government Business Enterprises Act 1995; or

(bc) State forest; or

(bd) Commonwealth land to which a fire protection services agreement applies; or

(c) the town of Savage River; or

(d) unimproved land, in any ownership, not exceeding 10 square metres in area; or

(e) a jetty that is –

(i) separately valued in the valuation list prepared under the Valuation of Land Act 2001; and

(ii) made entirely or mainly from non-combustible material; and

(iii) no more than 10 metres long; or

(f) a slipway that is separately valued in the valuation list prepared under the Valuation of Land Act 2001.

(2) This Division does apply to and in respect of land referred to in subsection (1)(a), (b) or (bb) if the land, or any part of it, is let or sublet to a private tenant.

(3) For the avoidance of doubt, a State-owned company is taken to be a private tenant for the purposes of this section.

(4) In this section –

exempt tenant, of land in a municipal area, means a tenant that the Commission, in its discretion and on the written application of the local council of the municipal area, has certified is occupying the land for –

(a) a benevolent, charitable or philanthropic purpose; or

(b) a non-profit community or non-profit sporting purpose;

fire protection services agreement means an agreement between the Commission and the Commonwealth under which the Commission undertakes to provide fire protection services in respect of specified Commonwealth land in this State in consideration of the Commonwealth making a contribution towards the operating costs of brigades;

GBE means a Government Business Enterprise within the meaning of the Government Business Enterprises Act 1995;

private tenant, of land in a municipal area, means a tenant other than –

(a) the Crown in right of the Commonwealth or in right of any State or Territory; or

(b) a local council; or

(c) a single authority or joint authority within the meaning of the Local Government Act 1993; or

(d) a State authority specified in Part 2 of Schedule 1 to the State Service Act 2000; or

(e) an exempt tenant;

State-owned company means a company incorporated under the Corporations Act that is controlled by the Crown in right of this State, by a GBE or statutory authority, or by another company that is so controlled;

statutory authority means a body or authority, whether incorporated or not, that is established or constituted by or under an Act or under the Royal Prerogative, being a body or authority which, or of which the governing authority, wholly or partly comprises a person or persons appointed by the Governor, a Minister or another statutory authority.

|

Agenda (Open Portion) Finance Committee Meeting |

Page 111 |

|

|

|

13/12/2016 |

|

6.2 Annual Review of Loan and Investment Portfolios - November 2016

File Ref: F16/133043

Report of the Manager Finance and the Director Financial Services of 8 December 2016.

Delegation: Council

|

Item No. 6.2 |

Agenda (Open Portion) Finance Committee Meeting |

Page 113 |

|

|

13/12/2016 |

|

REPORT TITLE: Annual Review of Loan and Investment Portfolios - November 2016

REPORT PROVIDED BY: Manager Finance

Director Financial Services

1. Report Purpose and Community Benefit

1.1. The purpose of this report is to provide details of the Council’s current loan and investment portfolios and to discuss early repayment options.

2. Report Summary

2.1. The Council’s loan portfolio as at 31 October 2016 was $13.097M, with a weighted average interest rate of 5.56% per annum.

2.2. The balance of the Council’s investment portfolio as at 31 October 2016 was $21.3M, with a weighted average interest rate of 2.45% per annum.

2.3. The Council is able to refinance loans which are attracting higher than the current market rate of interest at more attractive rates, but only after incurring significant up-front penalties. Furthermore, future cost savings would not be sufficient to recover the penalties in full.

2.4. Repaying loans using the Council’s owns funds is not an option due to restrictions or funds being earmarked for future spending, in particular the 10 year capital works program approved by the Council in April 2016.

|

That: 1. The Finance Committee receive and note the information contained in the report titled “Annual Review of Loans and Investment Portfolio – November 2016”. 2. The Council not pursue refinancing of its loan portfolio.

|

4. Background

4.1. At its meeting held on 21 September 2013, the Finance and Corporate Services Committee requested a report be provided reviewing the Council’s current loan and investment portfolios, noting the interest rate differential between the two portfolios, with such a review to occur annually.

4.2. Loan Portfolio

4.2.1. As at 31 October 2016, the balance of the loan portfolio was $13.097M. The details are as follows:

|

Lender |

Loan Amount ($,000) |

Principal & Interest (P&I) or Interest Only (IO) |

Drawdown Date |

Term (years) |

Maturity Date |

Interest Rate (fixed) |

Balance ($,000) |

Early repayment cost ($,000) |

|

Commonwealth Bank |

4,800 |

P&I |

30/06/2006 |

30 |

30/06/2036 |

6.41% |

4,052 |

1,312 |

|

Tascorp |

1,700 |

P&I |

30/06/2010 |

10 |

30/06/2020 |

6.48% |

836 |

7 |

|

Tascorp |

1,850 |

P&I |

30/06/2011 |

10 |

30/06/2021 |

6.24% |

1,066 |

14 |

|

Tascorp |

5,000 |

P&I |

29/06/2012 |

10 |

29/06/2022 |

4.89% |

3,284 |

74 |

|

Tascorp |

2,500 |

P&I |

28/06/2013 |

10 |

30/06/2023 |

5.13% |

1,878 |

47 |

|

Tascorp |

2,375 |

P&I |

30/06/2014 |

10 |

30/06/2024 |

4.56% |

1,981 |

52 |

|

|

|

|

|

|

|

|

13,097 |

1,506 |

4.2.2. As at 31 October 2016, the weighted average interest rate of the loan portfolio was 5.56% per annum. This average rate is a low rate, but nonetheless is higher than the rate being earned on investments (see 4.3 below).

4.2.3. The loan portfolio currently includes loans taken out between 2006 and 2014, during which time interest rates have reduced. As a result, these loans are costing more than the current market rate of interest.

4.2.4. Each loan is subject to an early repayment penalty which would be charged in addition to the outstanding principal and any accrued interest. This penalty makes it unattractive to refinance loans at a lower interest rate.

4.2.5. This is the same conclusion as previous reviews. As part of the 2015 review, Wise Lord & Ferguson reviewed the Commonwealth bank loan specifically, and also concluded that it would not be cost effective to refinance that loan.

4.3. Investment Portfolio

4.3.1. As at 31 October 2016, the balance of the investment portfolio was $21.3M and the weighted average interest rate of the term deposits was 2.45% per annum.

5. Proposal and Implementation

5.1. It is proposed that the Council does not retire any of its current debt early due to the punitive early retirement fees and the impact on other initiatives, in particular the 10 year capital works program.

6. Strategic Planning and Policy Considerations

Goal 5 – Governance is applicable in considering this report, particularly

Strategic 5.1 objective:

“The organisation is relevant to the community and provides good governance and transparent decision-making”.

7. Financial Implications

7.1. Funding Source and Impact on Current Year Operating Result

7.1.1. Early loan repayment penalties have not been budgeted for and are not included in current forecast results.

7.1.2. The Council is able to refinance loans which are attracting higher than the current market rate of interest at more attractive rates, but only after incurring significant up-front penalties. Furthermore, future cost savings would not be sufficient to recover the penalties in full.

7.2. Impact on Future Years’ Financial Result

7.2.1. Future cost savings would not be sufficient to recover early repayment in full.

7.2.2. The Council’s Long-Term Financial Plan is premised on requiring further debt from 2018/19 to fund the 10 year capital works program. Debt levels will need to increase as the capital works program progresses.

8. Delegation

8.1. This matter is delegated to the Council.

As signatory to this report, I certify that, pursuant to Section 55(1) of the Local Government Act 1993, I hold no interest, as referred to in Section 49 of the Local Government Act 1993, in matters contained in this report.

|

Fiona Dixon Manager Finance |

David Spinks Director Financial Services |

Date: 8 December 2016

File Reference: F16/133043

|

Item No. 6.3 |

Agenda (Open Portion) Finance Committee Meeting |

Page 115 |

|

|

13/12/2016 |

|

6.3 Outstanding Long Term Parking Debts as at 30 November 2016

File Ref: F16/134295

Memorandum of the Manager Finance and the Director Financial Services of 8 December 2016.

Delegation: Committee

|

Item No. 6.3 |

Agenda (Open Portion) Finance Committee Meeting |

Page 117 |

|

|

13/12/2016 |

|

Memorandum: Finance Committee

Outstanding Long Term Parking Debts as at 30 November 2016

Information on sundry and long term parking debts (greater than $2,000) is provided to the Finance Committee on a quarterly basis. At the Finance Committee meeting of 15 June 2016, it was resolved that the debts be reported separately to allow the reporting of long term parking debts to appear on the Open portion of the Finance Committee agenda.

This memorandum provides information on long term parking debts only. Debts relating to rates, sundry debts and parking fines are reported separately to the Finance Committee and animal debts are managed by City Planning Division.

The table below, in comparison to the same period last year, shows:

· a 9% decrease (-$6,377.70) in total debts outstanding;

· a $3,269.83 increase in the 90 days and over category; and

· a $1,777.69 increase in debts 30 days and older (*), although this is impacted by an invoice timing issue.

|

|

31-Nov-15 |

% of total O/S |

31-Oct-16 |

% of total O/S |

31-Nov-16 |

% of total O/S |

|

|

$ |

|

$ |

|

$ |

|

|

Current |

59,081 |

84% |

61,287 |

79% |

50,926 |

79% |

|

30 days |

5,931 |

8% |

-177 |

0% |

5,770 |

9% |

|

60 days |

908 |

1% |

8,196 |

11% |

-423 |

-1% |

|

90 days |

4,818 |

7% |

8,234 |

11% |

8,087 |

13% |

|

Total |

70,738 |

|

77,541 |

|

64,360 |

|

|

|

|

|

|

|

|

|

|

* 30 days+(all) |

11,657 |

16% |

16,254 |

21% |

13,434 |

21% |

DEBTS GREATER THAN $2,000

There are currently no outstanding long term parking debts greater than $2,000.

|

That the information contained in the memorandum of the Manager Finance and Director Financial Services of 2 December 2016 titled “Outstanding Long Term Parking Debts as at 30 November 2016” be received and noted.

|

As signatory to this report, I certify that, pursuant to Section 55(1) of the Local Government Act 1993, I hold no interest, as referred to in Section 49 of the Local Government Act 1993, in matters contained in this report.

|

Peter Jenkins Manager Finance |

David Spinks Director Financial Services |

Date: 8 December 2016

File Reference: F16/134295

|

Agenda (Open Portion) Finance Committee Meeting |

Page 118 |

|

|

|

13/12/2016 |

|

A report indicating the status of current decisions is attached for the information of Aldermen.

REcommendation

That the information be received and noted.

Delegation: Committee

|

Agenda (Open Portion) Finance Committee Meeting |

Page 127 |

|

|

|

13/12/2016 |

|

Regulation 29(3) Local Government

(Meeting Procedures) Regulations 2015.

File Ref: 13-1-10

The General Manager reports:-

“In accordance with the procedures approved in respect to Questions Without Notice, the following responses to questions taken on notice are provided to the Committee for information.

The Committee is reminded that in accordance with Regulation 29(3) of the Local Government (Meeting Procedures) Regulations 2015, the Chairman is not to allow discussion or debate on either the question or the response.”

8.1 State Government Support Funding for the Taste of Tasmania

File Ref: F16/132479; 13-1-10

Report of the Director Community Development of 13 December 2016.

Delegation: Committee

|

That the information be received and noted.

|

|

Item No. 8.1 |

Agenda (Open Portion) Finance Committee Meeting |

Page 129 |

|

|

13/12/2016 |

|

Memorandum: Lord Mayor

Deputy Lord Mayor

Aldermen

Response to Question Without Notice

State Government Support Funding for the Taste of Tasmania

|

Meeting: Finance Committee

|

Meeting date: 15 November 2016

|

|

Raised by: Alderman Sexton |

|

Question:

How does the recent announcement by the State Government regarding funding of $50,000 to support North West stallholders to participate in the Taste of Tasmania, affect stallholder selection?

Response:

The sponsorship agreement with the State Government was not negotiated until after Taste of Tasmania stallholder applications closed on 8 July 2016, and so this contribution did not affect the stallholder selection process.

Of the total number of 68 stallholders, there are 16 stallholders from the North / North West.

As resolved by the Council at its meeting held on 26 September 2016, this support has also assisted the Council to provide a reduction in fixed site fees for all stallholders, up to a maximum of $2,000 per stallholder.

Council staff are currently working with Department of State Growth staff to finalise the detail of the Grant Deed associated with the Tasmanian Government contribution to the event.

As signatory to this report, I certify that, pursuant to Section 55(1) of the Local Government Act 1993, I hold no interest, as referred to in Section 49 of the Local Government Act 1993, in matters contained in this report.

|

Philip Holliday Director Community Development |

|

Date: 8 December 2016

File Reference: F16/132479; 13-1-10

|

|

Agenda (Open Portion) Finance Committee Meeting |

Page 130 |

|

|

13/12/2016 |

|

Section 29 of the Local Government (Meeting Procedures) Regulations 2015.

File Ref: 13-1-10

An Alderman may ask a question without notice of the Chairman, another Alderman, the General Manager or the General Manager’s representative, in line with the following procedures:

1. The Chairman will refuse to accept a question without notice if it does not relate to the Terms of Reference of the Council committee at which it is asked.

2. In putting a question without notice, an Alderman must not:

(i) offer an argument or opinion; or

(ii) draw any inferences or make any imputations – except so far as may be necessary to explain the question.

3. The Chairman must not permit any debate of a question without notice or its answer.

4. The Chairman, Aldermen, General Manager or General Manager’s representative who is asked a question may decline to answer the question, if in the opinion of the respondent it is considered inappropriate due to its being unclear, insulting or improper.

5. The Chairman may require a question to be put in writing.

6. Where a question without notice is asked and answered at a meeting, both the question and the response will be recorded in the minutes of that meeting.

7. Where a response is not able to be provided at the meeting, the question will be taken on notice and

(i) the minutes of the meeting at which the question is asked will record the question and the fact that it has been taken on notice.

(ii) a written response will be provided to all Aldermen, at the appropriate time.

(iii) upon the answer to the question being circulated to Aldermen, both the question and the answer will be listed on the agenda for the next available ordinary meeting of the committee at which it was asked, where it will be listed for noting purposes only.

|

|

Agenda (Open Portion) Finance Committee Meeting |

Page 131 |

|

|

13/12/2016 |

|