City

of hobart

AGENDA

Finance Committee Meeting

Open Portion

Tuesday, 14 November 2017

at 5.00 pm

Lady Osborne Room, Town Hall

City

of hobart

AGENDA

Finance Committee Meeting

Open Portion

Tuesday, 14 November 2017

at 5.00 pm

Lady Osborne Room, Town Hall

THE MISSION

Our mission is to ensure good governance of our capital City.

THE VALUES

The Council is:

|

about people |

We value people – our community, our customers and colleagues. |

|

professional |

We take pride in our work. |

|

enterprising |

We look for ways to create value. |

|

responsive |

We’re accessible and focused on service. |

|

inclusive |

We respect diversity in people and ideas. |

|

making a difference |

We recognise that everything we do shapes Hobart’s future. |

|

|

Agenda (Open Portion) Finance Committee Meeting |

Page 3 |

|

|

14/11/2017 |

|

Business listed on the agenda is to be conducted in the order in which it is set out, unless the committee by simple majority determines otherwise.

APOLOGIES AND LEAVE OF ABSENCE

1. Co-Option of a Committee Member in the event of a vacancy

3. Consideration of Supplementary Items

4. Indications of Pecuniary and Conflicts of Interest

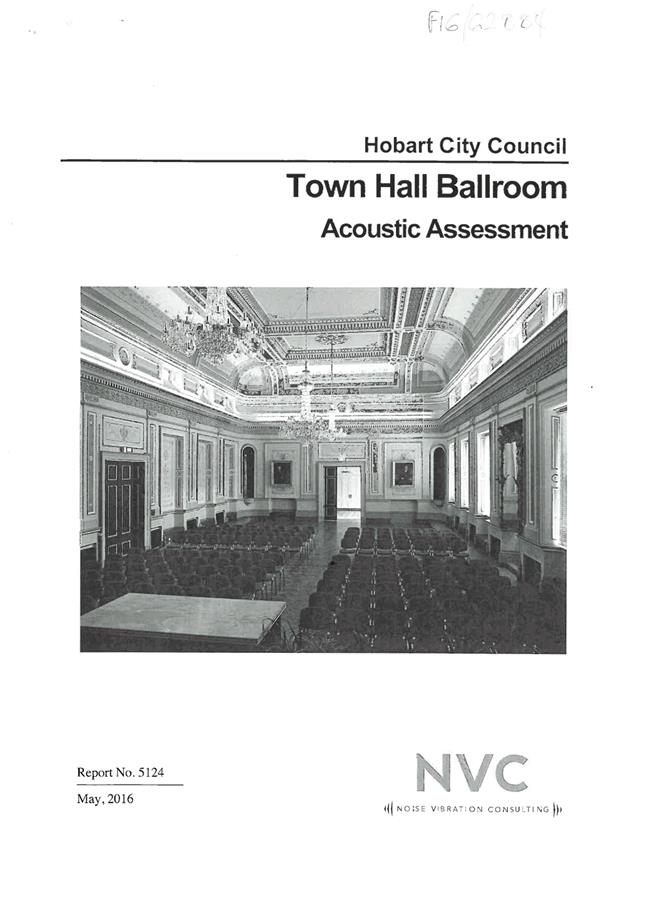

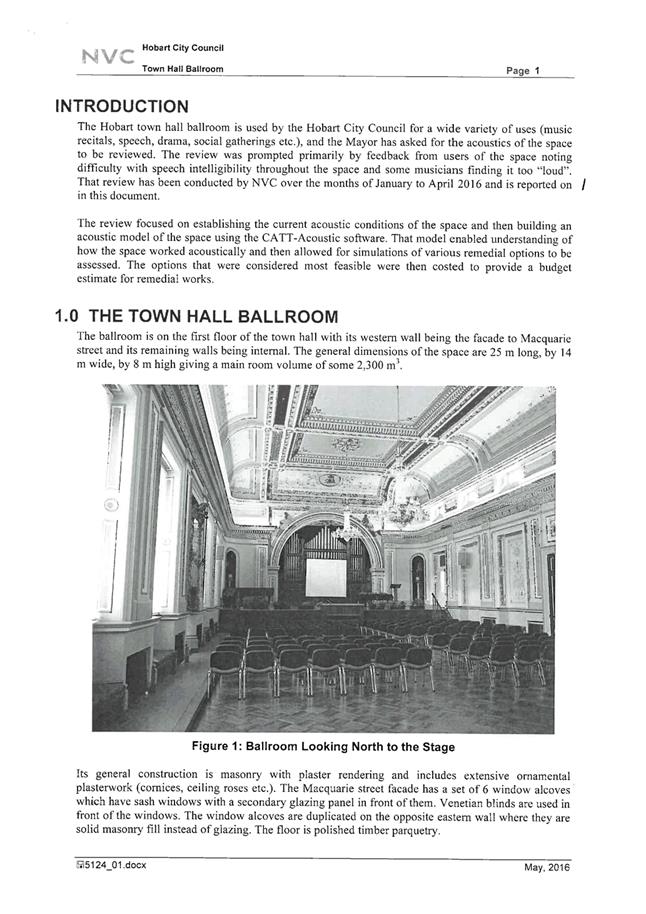

6.1 Hobart Town Hall Ballroom - Acoustics

6.2 Financial Report as at 30 September 2017

6.3 Occupancy Rates - Multi-Storey Car Parks

6.4 Grants and Benefits Listing as at 30 September 2017

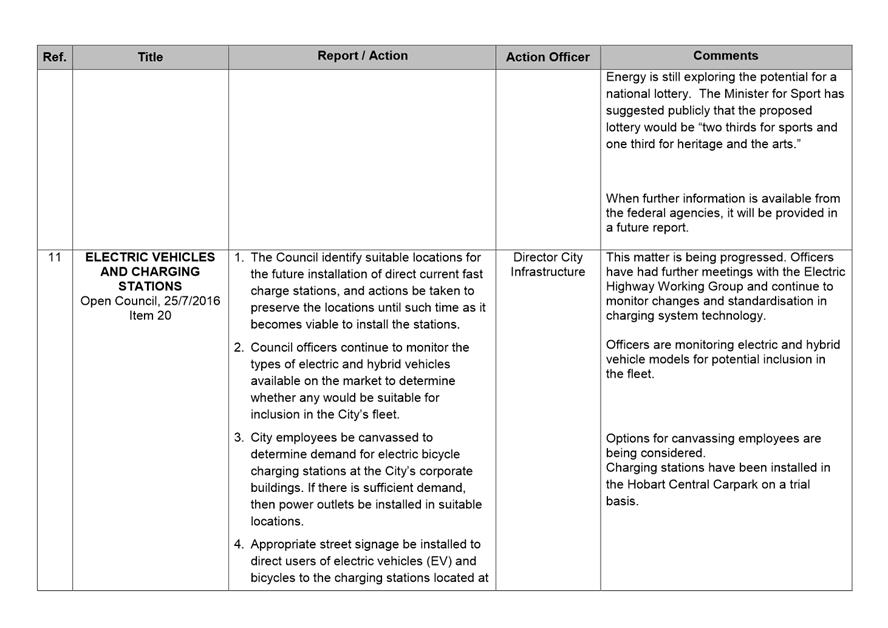

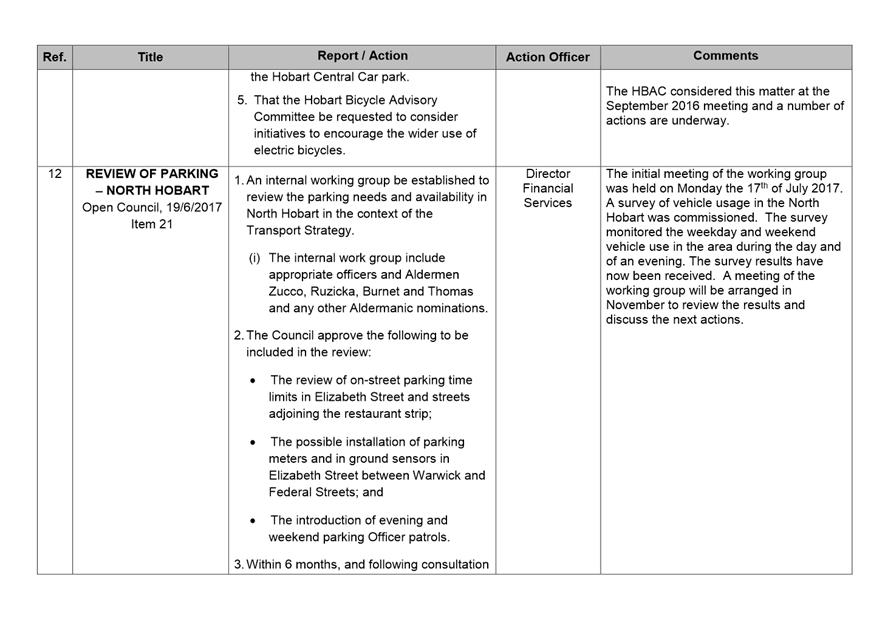

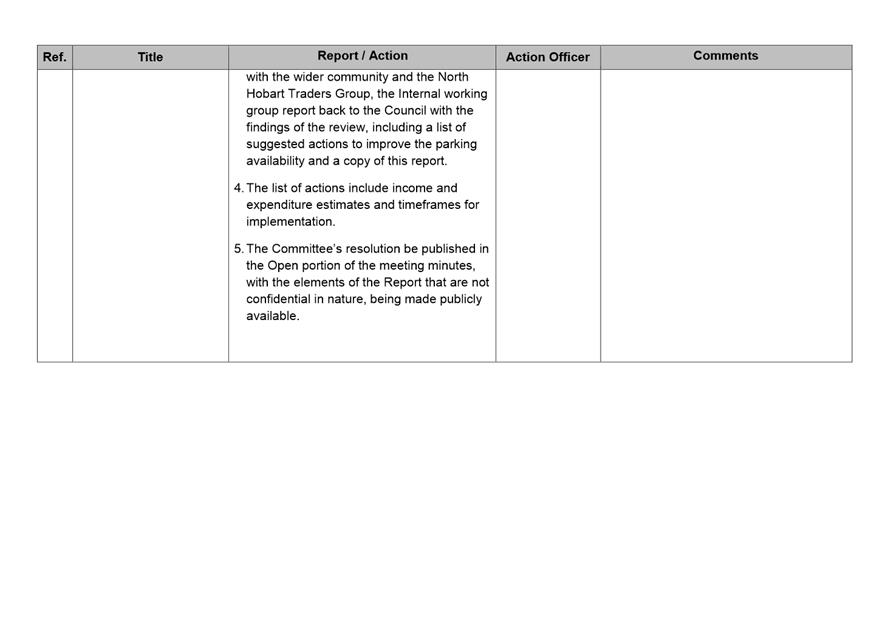

7 Committee Action Status Report

7.1 Committee Actions - Status Report

9. Closed Portion Of The Meeting

|

|

Agenda (Open Portion) Finance Committee Meeting |

Page 4 |

|

|

14/11/2017 |

|

Finance Committee Meeting (Open Portion) held Tuesday, 14 November 2017 at 5.00 pm in the Lady Osborne Room, Town Hall.

|

COMMITTEE MEMBERS Thomas (Chairman) Deputy Lord Mayor Christie Zucco Ruzicka Sexton

ALDERMEN Lord Mayor Hickey Briscoe Burnet Cocker Reynolds Denison Harvey |

APOLOGIES: Nil

LEAVE OF ABSENCE: Nil

|

|

The minutes of the Open Portion of the Finance Committee meeting held on Tuesday, 17 October 2017 and the Special Finance Committee meeting held on Monday, 6 November 2017, are submitted for confirming as an accurate record.

|

Ref: Part 2, Regulation 8(6) of the Local Government (Meeting Procedures) Regulations 2015.

|

That the Committee resolve to deal with any supplementary items not appearing on the agenda, as reported by the General Manager.

|

Ref: Part 2, Regulation 8(7) of the Local Government (Meeting Procedures) Regulations 2015.

Aldermen are requested to indicate where they may have any pecuniary or conflict of interest in respect to any matter appearing on the agenda, or any supplementary item to the agenda, which the committee has resolved to deal with.

Regulation 15 of the Local Government (Meeting Procedures) Regulations 2015.

A committee may close a part of a meeting to the public where a matter to be discussed falls within 15(2) of the above regulations.

In the event that the committee transfer an item to the closed portion, the reasons for doing so should be stated.

Are there any items which should be transferred from this agenda to the closed portion of the agenda, or from the closed to the open portion of the agenda?

|

Agenda (Open Portion) Finance Committee Meeting |

Page 6 |

|

|

|

14/11/2017 |

|

6.1 Hobart Town Hall Ballroom - Acoustics

Report of the Group Manager City Government & Customer Relations and the Deputy General Manager of 9 November 2017 and attachment.

Delegation: Council

|

Item No. 6.1 |

Agenda (Open Portion) Finance Committee Meeting |

Page 7 |

|

|

14/11/2017 |

|

REPORT TITLE: Hobart Town Hall Ballroom - Acoustics

REPORT PROVIDED BY: Group Manager City Government & Customer Relations

Deputy General Manager

1. Report Purpose and Community Benefit

1.1. The purpose of this report is to respond to the following Council resolution from its meeting held on 22 June 2015;

That: 1. A report be prepared documenting the quality of acoustics for the Hobart Town Hall ballroom.

2. The report should identify any deficit in audio and instrumental acoustic quality and make recommendations as to how improved levels of instrumental and speech intelligibility can be achieved and what steps need to be taken to achieve these outcomes.

3. The report further address the costs associated with the recommendations made.

1.2. As a usable venue, the Town Hall ballroom is a popular location for a wide range of functions including weddings, receptions, cocktail functions, floral shows, concerts and meetings, with the historical setting and unique presentation setting it aside from other spaces available for hire.

2. Report Summary

2.1. The Council resolution arose from a notice of motion put forward by the Lord Mayor, which was prompted by feedback from the public regarding the poor acoustic quality of the venue for speaking engagements and some musical events.

2.2. Following the Council resolution consultant engineers, NVC (Noise Vibration Consulting) were engaged to provide an acoustic assessment of the ballroom.

2.3. The assessment was conducted from January to April 2016 and focused on establishing the current acoustic conditions of the ballroom and creating an acoustic model of the space which allowed for simulations of various remedial options. Their report is provided at Attachment A.

2.4. A range of measures have been recommended by the consultants which are covered in more detail in Section 5 of this report.

2.5. The findings of the report conclude that:

2.5.1. The background noise level is not causing intelligibility when the PA is used however unamplified speech and musical performances will be adversely affected by the background noise level.

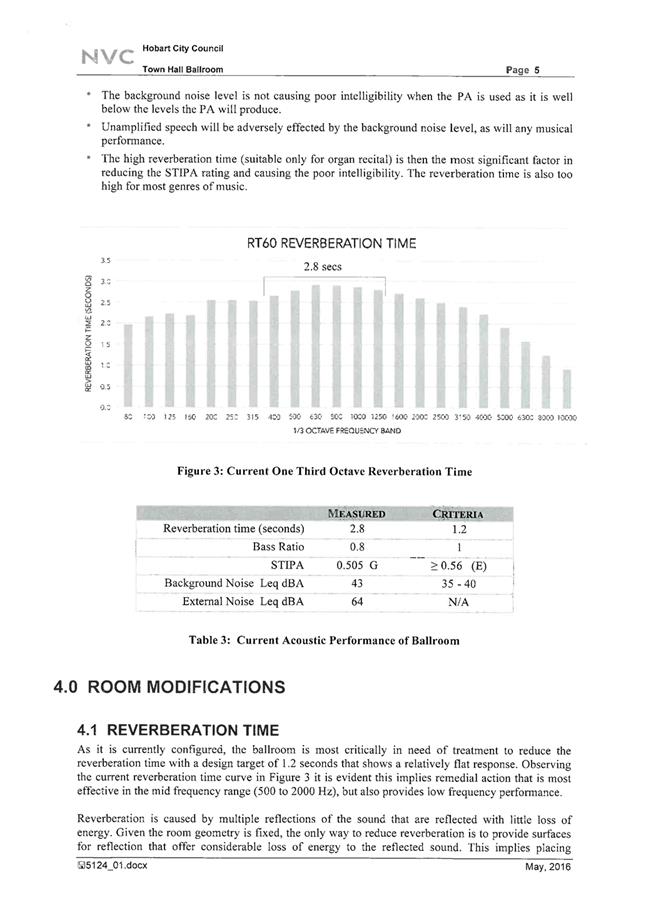

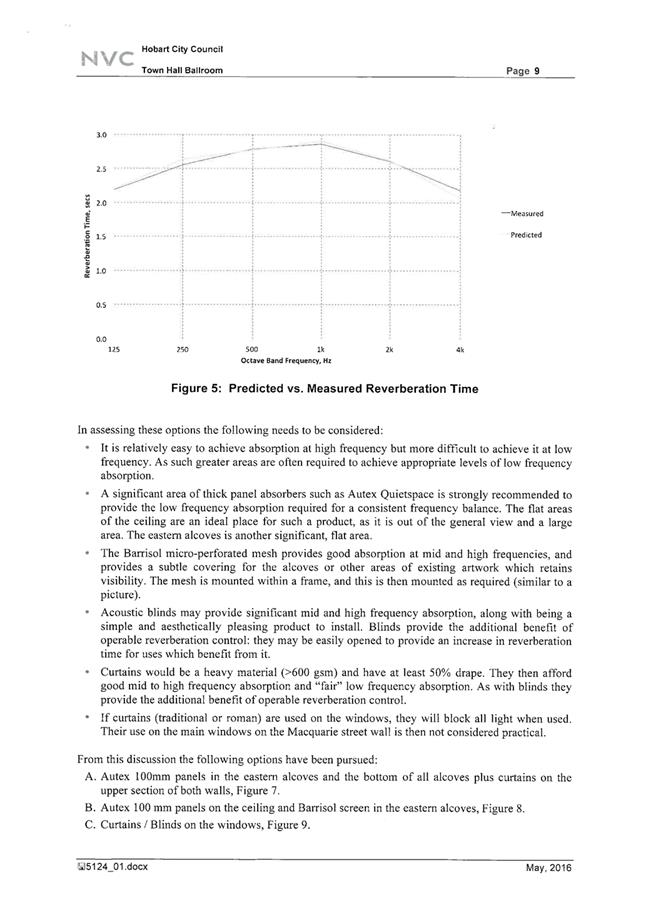

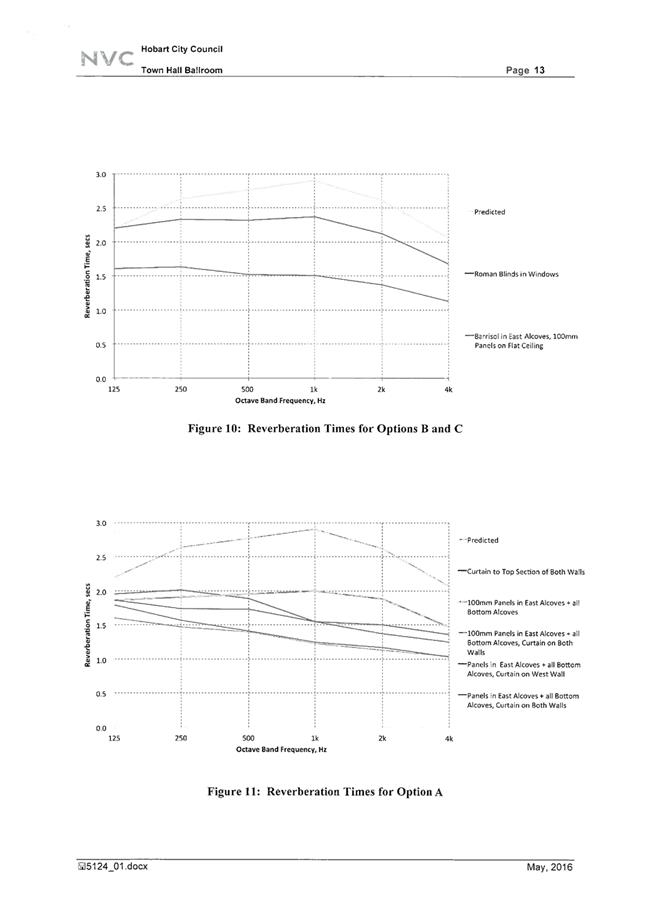

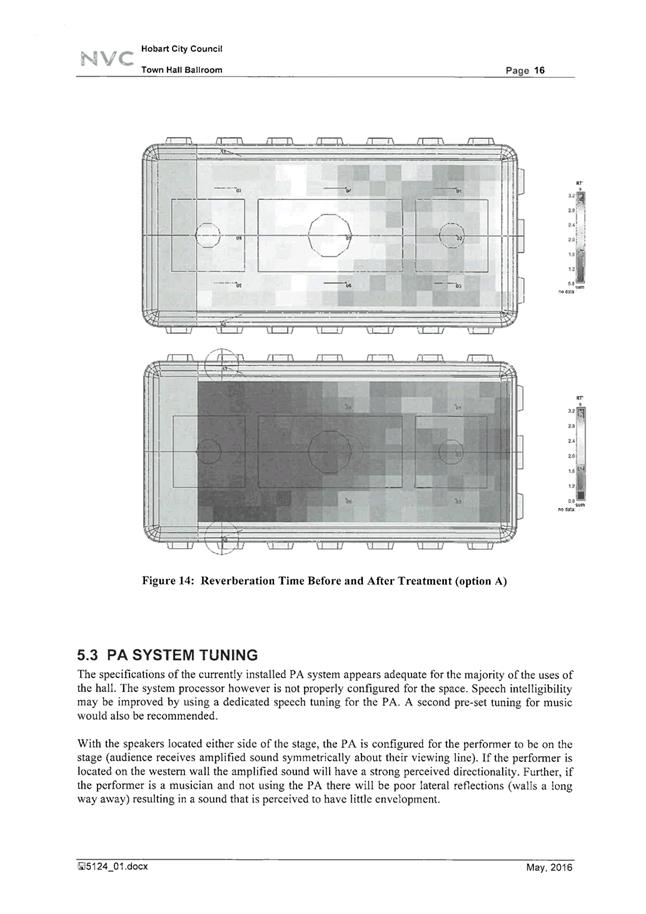

2.5.2 The high reverberation time of 2.8 seconds is the most significant factor and to improve the acoustics in the ballroom treatment to improve the reverberation time is required.

2.6. Upon its opening, the Town Hall ballroom was used for society events such as concerts, grand balls and organ recitals.

2.7. Of note is the optimum suitability acoustics of the ballroom for organ recitals.

2.8. The uniqueness of the space and its importance to the City has been acknowledged over many years, highlighted by the focus on restoring and preserving it for future generations.

2.9. The passage of time and the changes that brings with it present challenges in terms of the type of activities which are suitable for the ballroom, without negatively impinging on the historic fabric of the room.

2.10. A range of measures suggested by the consultant can be suitably accommodated and will deliver improvements for users of the space. Others however are not recommended at this stage as they involve material changes to existing historical treatments within the room.

|

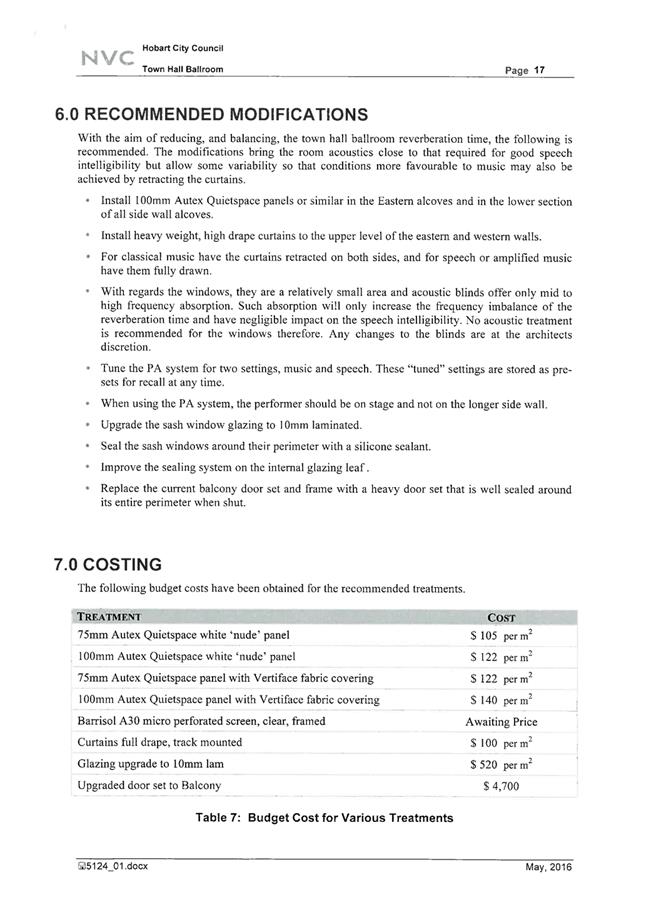

That: 1. The report prepared by NVC (Noise Vibration Consulting) in respect to the Town Hall Acoustic Assessment be received and noted. 2. The following measures, as recommended by the consultant, be endorsed, at an estimated cost of $10,000, as a means of improving the acoustics of the Town Hall Ballroom: 2.1. Upgrade the sash window glazing to 10mm laminated. 2.2 Seal the sash windows around the perimeter with a silicone sealant (this will mean they are no longer operable). 2.3 Improve the sealing system on the internal glazing leaf. 2.4 Replace the current balcony door set and frame with a heavy door set that is well sealed around the entire perimeter when shut.

|

4. Background

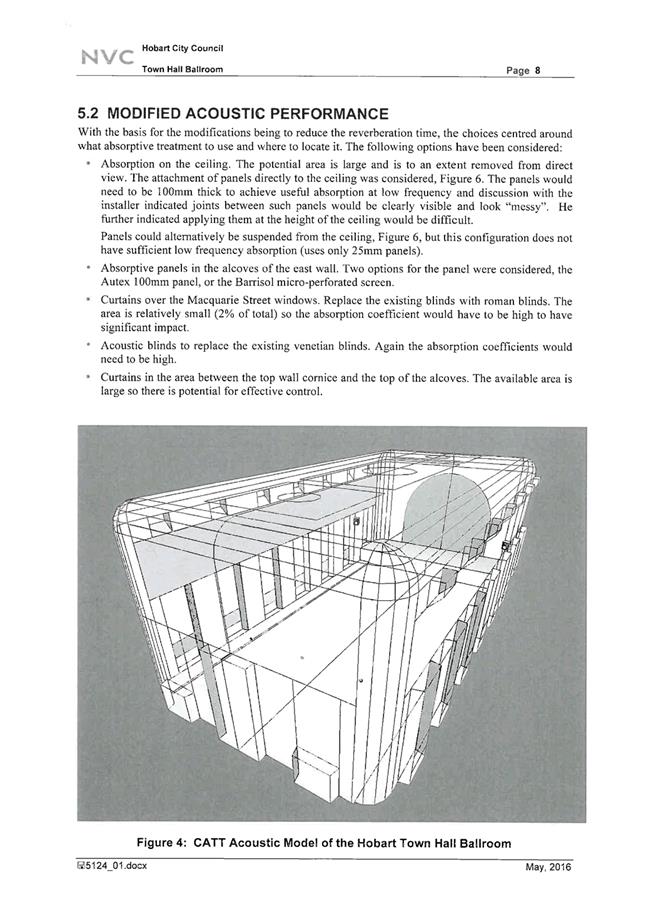

4.1. The consultant’s assessment identified the main cause of the poor acoustics in the ballroom as the volume to seating capacity being very high. A reduced volume could be achieved by having a lower ceiling and / or raked seating, neither of which are achievable for the ballroom.

4.2. Due to the mixed use of the ballroom for a range of speech and music conditions, the assessment worked on a compromise between speech and music conditions with a leaning towards good speech conditions.

4.3. The current acoustic quality of the ballroom was measured under several conditions. The results identified that:

4.3.1. The reverberation time was determined to be 2.8 seconds; ideally the time for speech is 1.0 seconds and 1.12 seconds for music. The design target for the ballroom, which is a compromise between good speech and music conditions, is 1.2 seconds.

4.3.2. Background noise levels from traffic on Macquarie Street were found to be a secondary effect which will impact on both speech and music quality, where amplification is not used.

5. Proposal and Implementation

5.1. The results of the assessment reflect that use of the ballroom for speaking engagements presents the most significant problems.

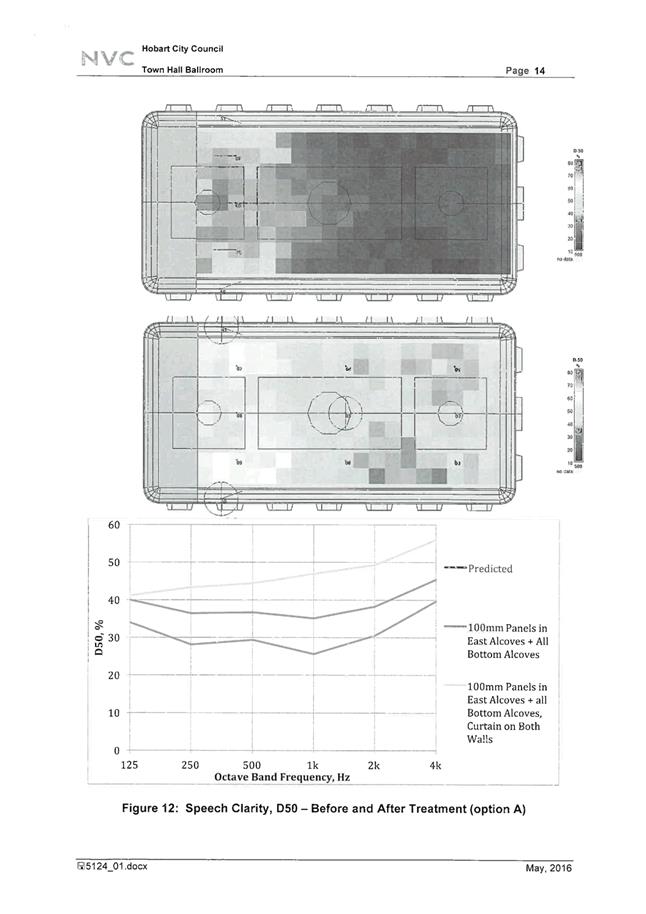

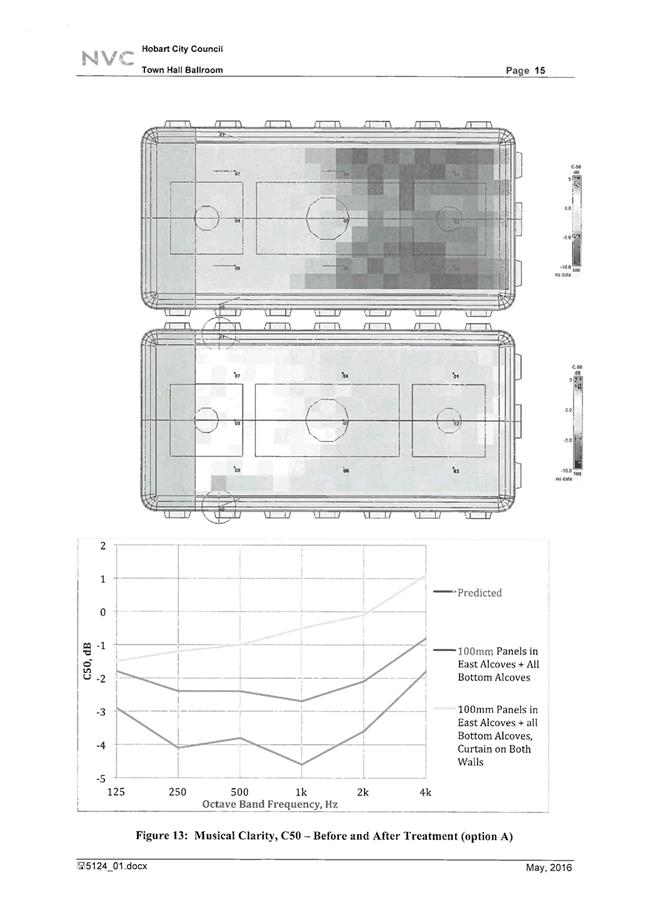

5.2. The assessment report concluded that several remedial actions could be employed to reduce the reverberation time in the space and provide some improvement to the background noise levels.

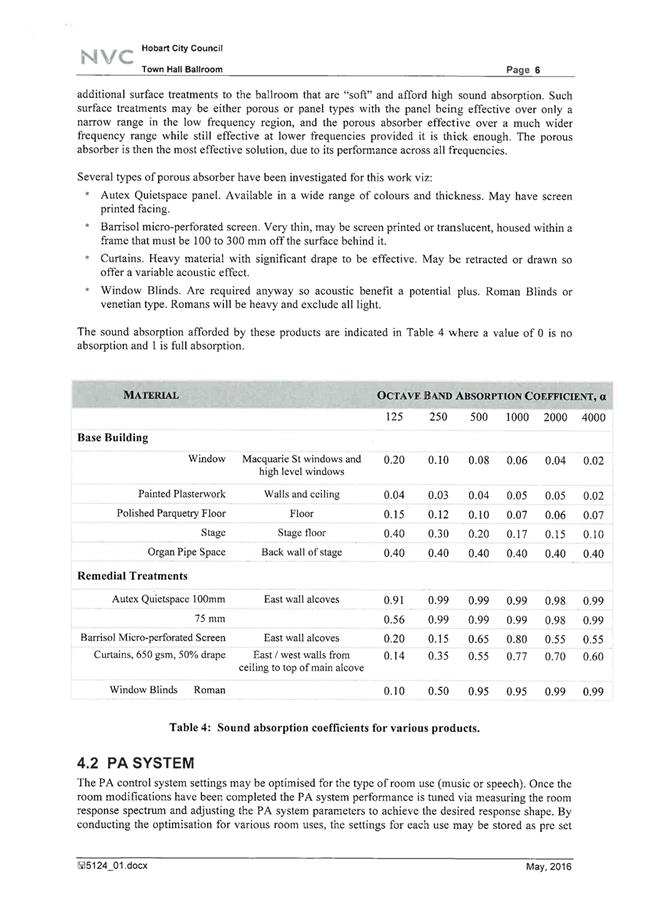

5.3. These actions include the use of additional surface treatments that are “soft” and provide high sound absorption and include the provision of porous or panel absorbers, curtains and window blinds.

5.4. Specifically the recommendations include the following additional installations in the ballroom:

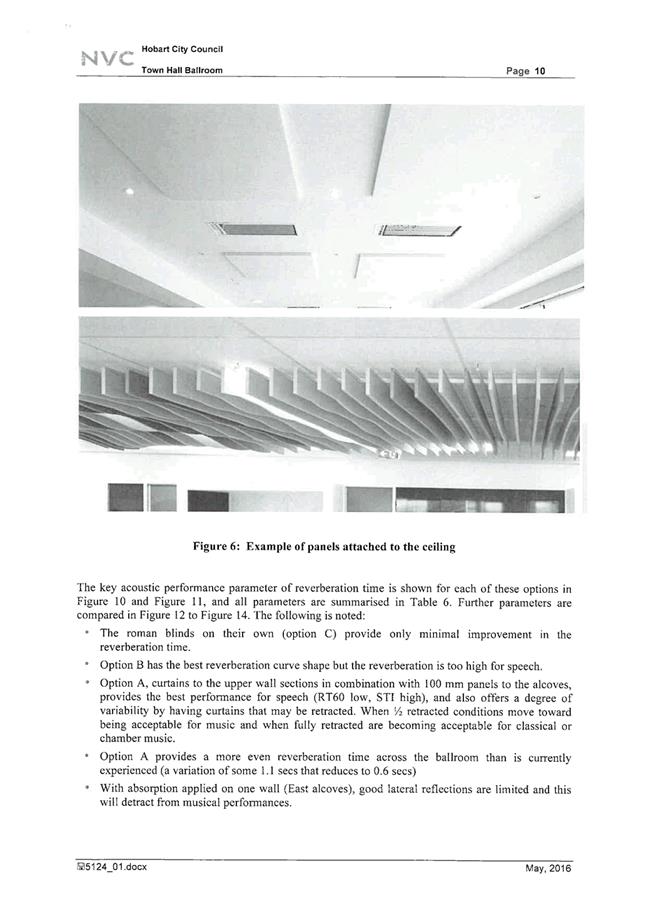

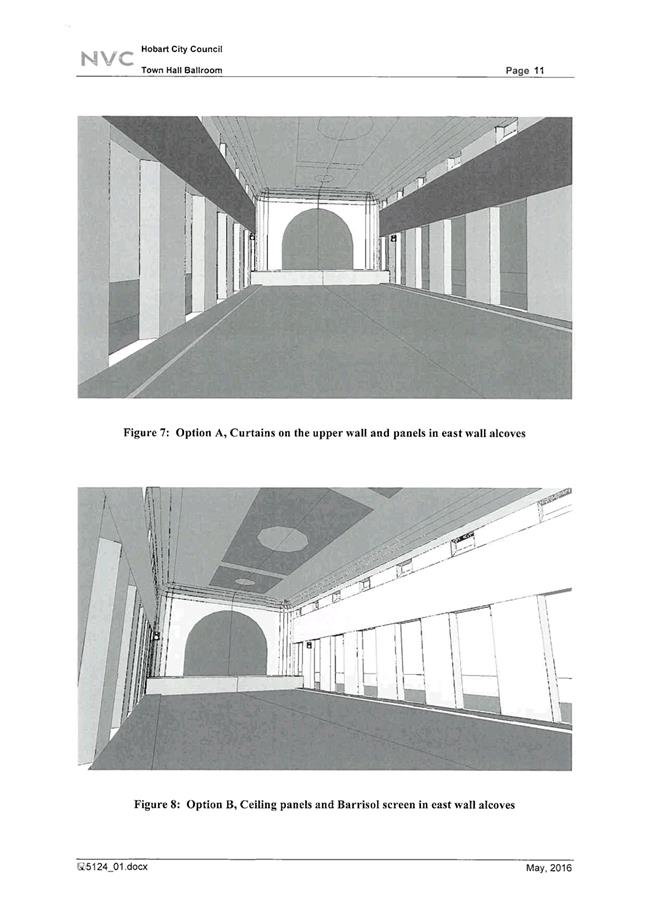

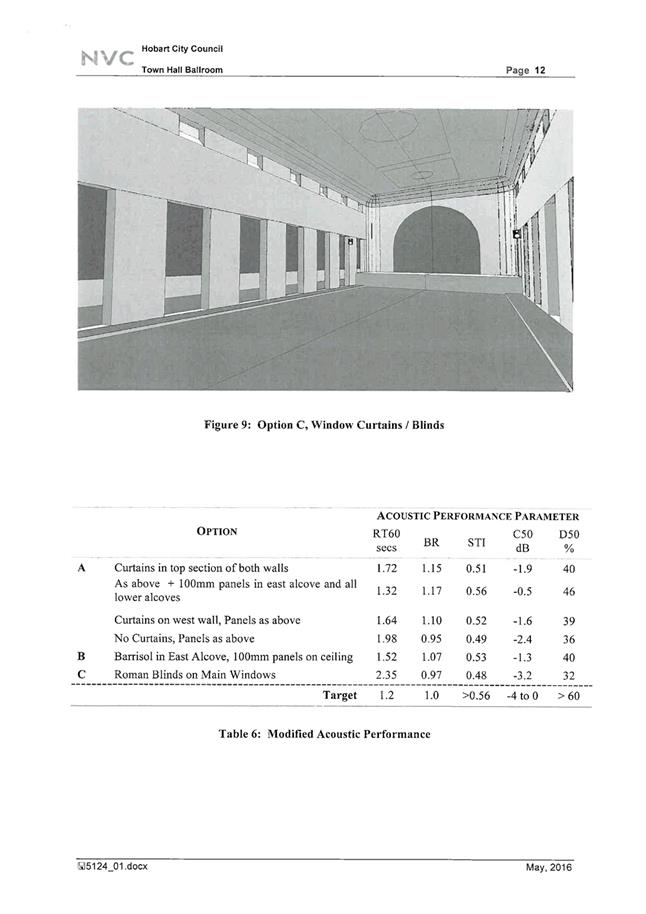

5.4.1. 100mm panels in the eastern alcoves of the ballroom and in the lower section of all wall alcoves.

5.4.2. Heavy weight, high drape curtains to the upper level of the eastern and western walls. (For classical music the curtains should be retracted on both sides, and for speech or amplified music have them fully drawn).

5.4.3. Upgrade the sash window glazing to 10mm laminated.

5.4.4. Seal the sash windows around the perimeter with a silicone sealant (this will mean they are no longer operable).

5.4.5. Improve the sealing system on the internal glazing leaf.

5.4.6. Replace the current balcony door set and frame with a heavy door set that is well sealed around the entire perimeter when shut.

5.5. Those treatments which are recommended include those outlined in clauses 5.4.3 to 5.4.6 above.

5.6. These measures will have no material effect on the presentation of the ballroom and will deliver practical improvements to the acoustics within the space.

5.7. In addition to these improvements, the consultant has recommended that:

5.7.1. The public address (PA) system be specifically tuned to two separate settings to accommodate music and speech.

5.7.2. When using the PA system, the performer should be on the stage and not on the longer side wall.

5.8. In terms of the remaining recommended treatments, which involve the provision of curtains and the installation of modified acoustic performance materials, these are not supported at this time as they would have an impact on the material fabric and appearance of the ballroom.

5.8.1. The blinds in the ballroom have also been upgraded since preparation of the consultant’s report.

6. Strategic Planning and Policy Considerations

6.1. The availability of suitable community spaces for use and the preservation of our heritage buildings supports the following goals within the Strategic Plan 2015-2025:

6.1.1. Economic development, vibrancy and culture;

6.1.2. Strong, safe and healthy communities; and

6.1.3. Unique heritage assets are protected and celebrated.

7. Financial Implications

7.1. Funding Source and Impact on Current Year Operating Result

7.1.1. The proposed works have been costed in the order of $10,000 and can be accommodated within the current operating plan.

8. Legal, Risk and Legislative Considerations

8.1. There are no legal considerations arising from this report.

9. Delegation

9.1. This matter is reserved to the Council.

As signatory to this report, I certify that, pursuant to Section 55(1) of the Local Government Act 1993, I hold no interest, as referred to in Section 49 of the Local Government Act 1993, in matters contained in this report.

|

Margaret Johns Group Manager City Government & Customer Relations |

Heather Salisbury Deputy General Manager |

Date: 9 November 2017

File Reference: F16/132225; 60-1-1; 13-1-9

Attachment a: Consultants

Report - Town Hall Acoustic Assessment ⇩ ![]()

|

Agenda (Open Portion) Finance Committee Meeting |

Page 33 |

|

|

|

14/11/2017 |

|

6.2 Financial Report as at 30 September 2017

Report of the Budget and Reporting Manager, the Manager Finance and the Director Financial Services of 9 November 2017 and attachment.

Delegation: Council

|

Item No. 6.2 |

Agenda (Open Portion) Finance Committee Meeting |

Page 34 |

|

|

14/11/2017 |

|

REPORT TITLE: Financial Report as at 30 September 2017

REPORT PROVIDED BY: Budget and Reporting Manager

Manager Finance

Director Financial Services

1. Report Purpose and Community Benefit

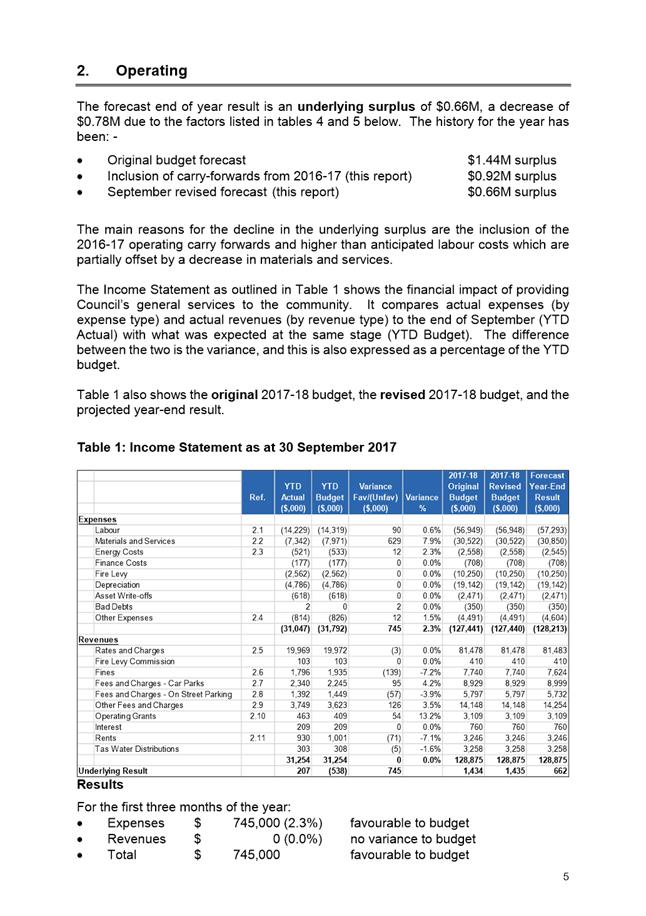

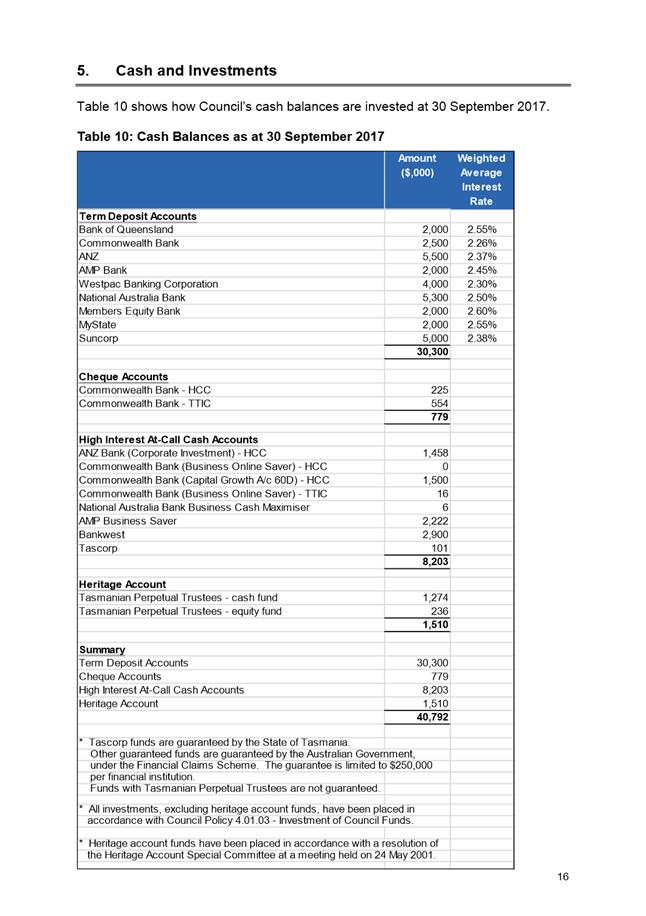

1.1. The purpose of this report is to present Council’s Financial Report for the period ending 30 September 2017 and to seek approval for changes to the 2017/2018 Estimates (budget).

2. Report Summary

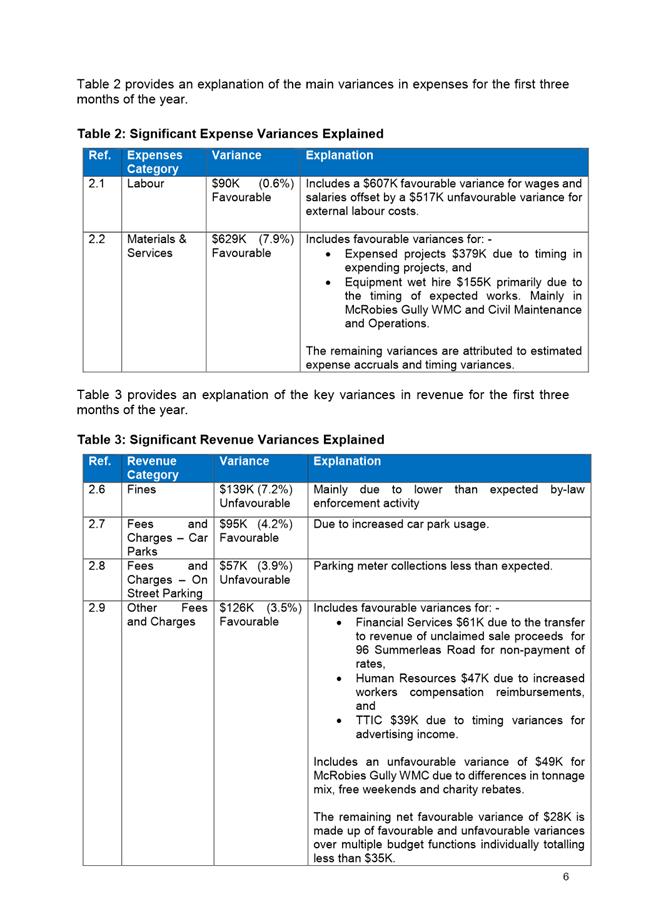

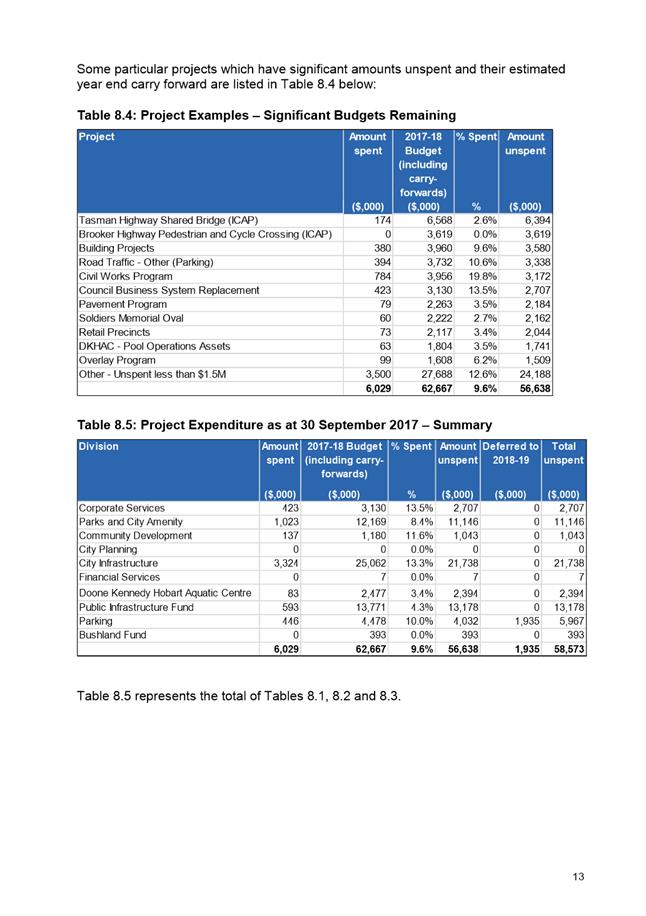

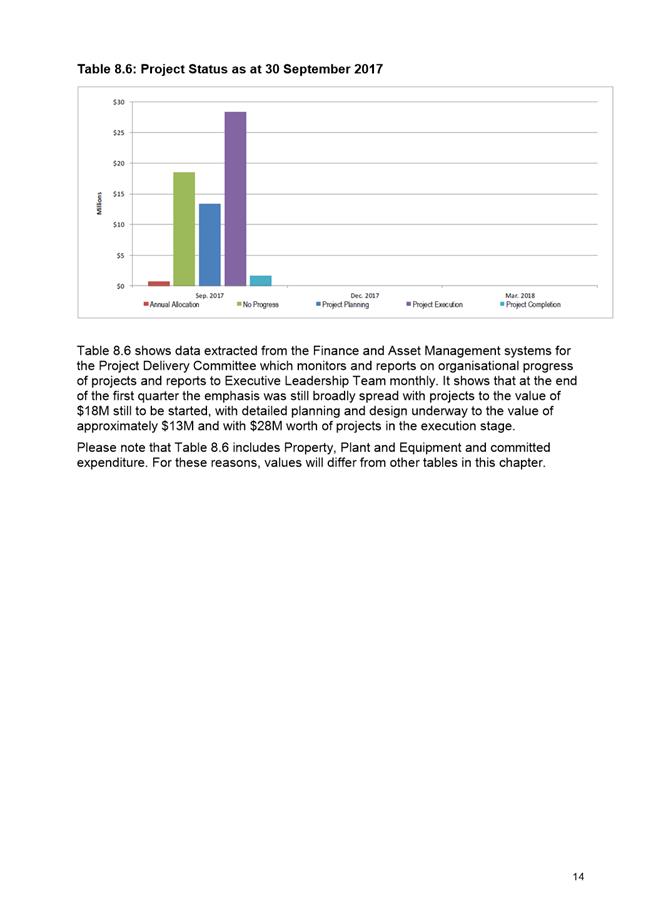

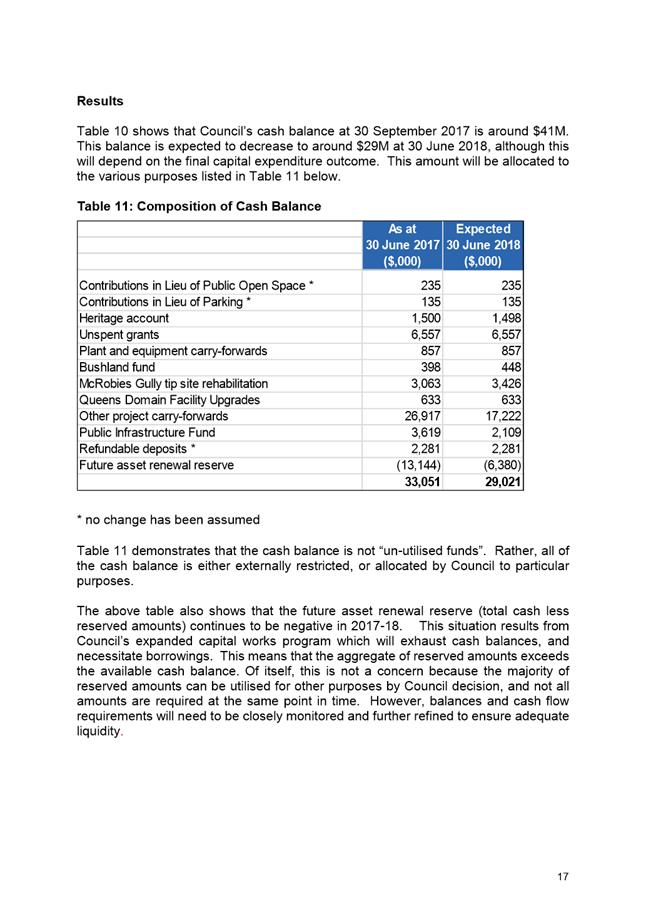

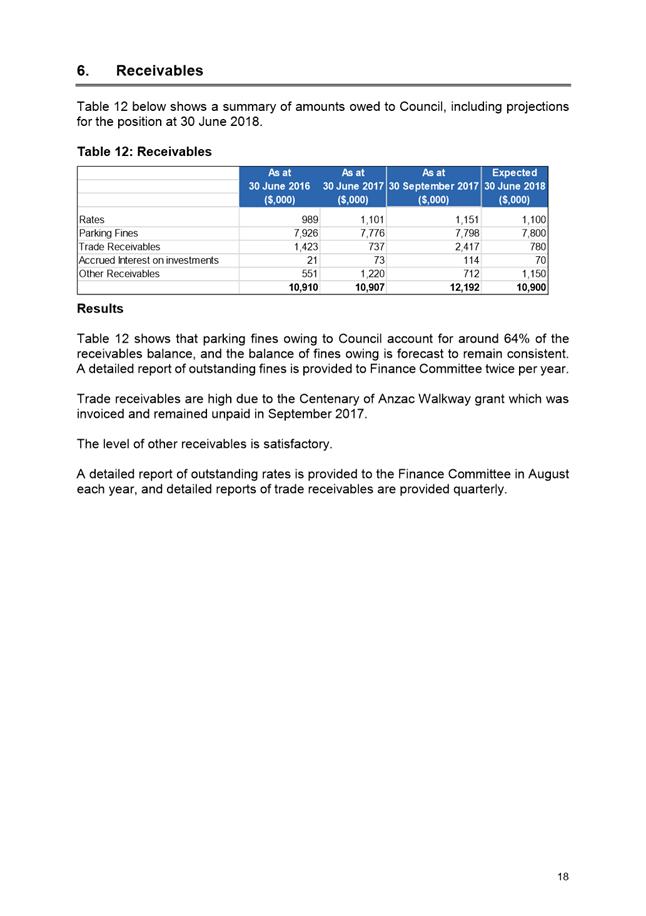

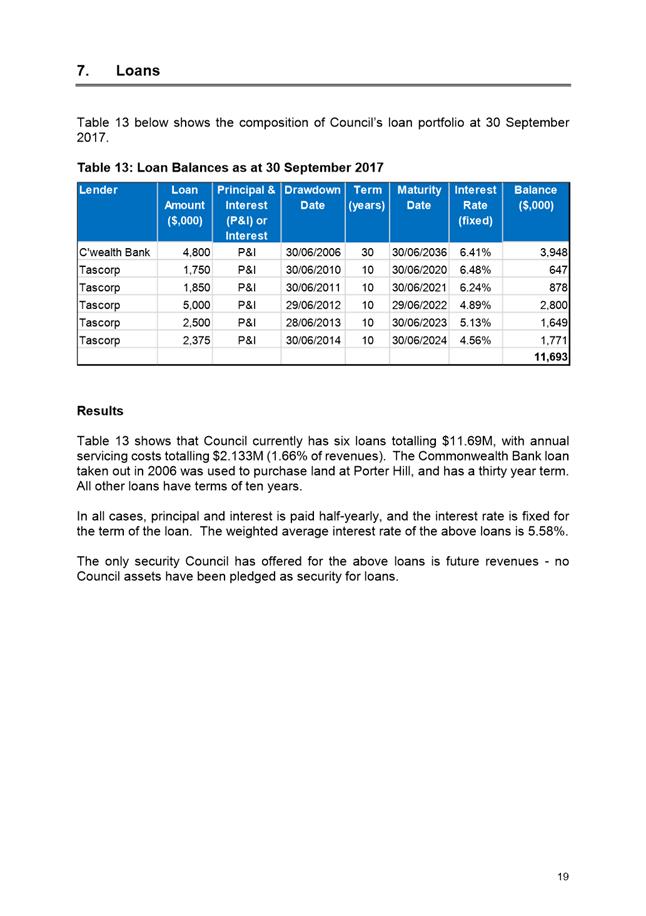

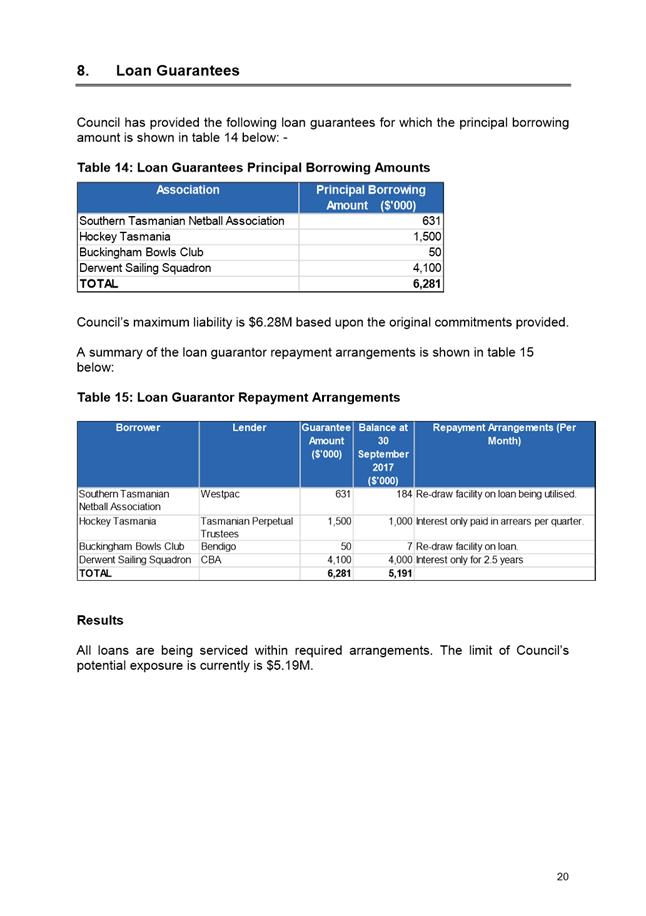

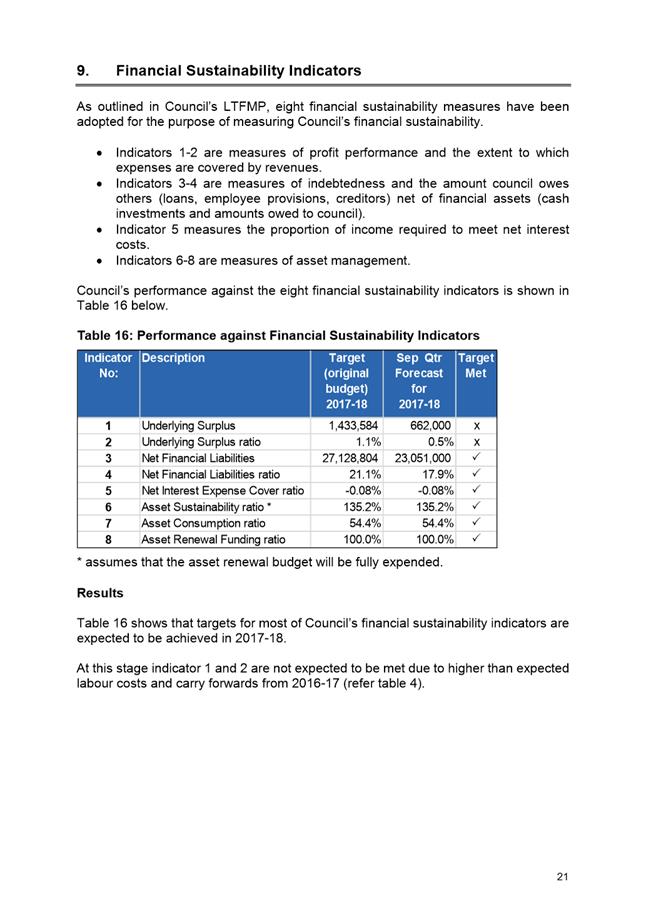

2.1. The Financial Report for the period ending 30 September 2017 is presented for consideration. It shows that expenses are currently favourable when compared to budget, and forecasts the following financial outcomes for 2017/2018:

2.1.1. An underlying surplus of $0.66M;

2.1.2. A closing cash balance of around $29M; and

2.1.3. The achievement of targets set for most of the Council’s eight financial sustainability indicators.

2.2. The Council remains in a strong, sustainable financial position.

|

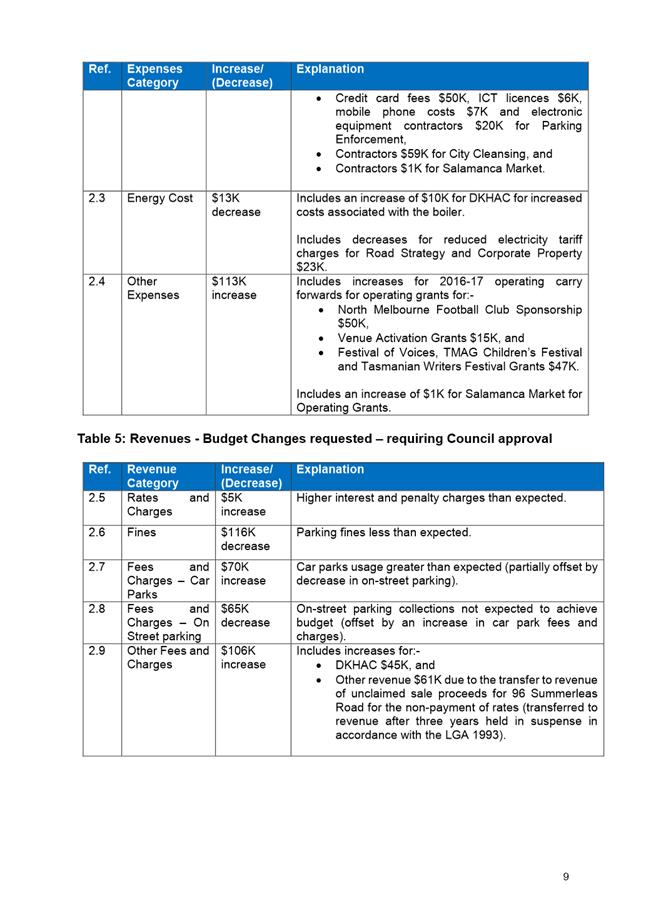

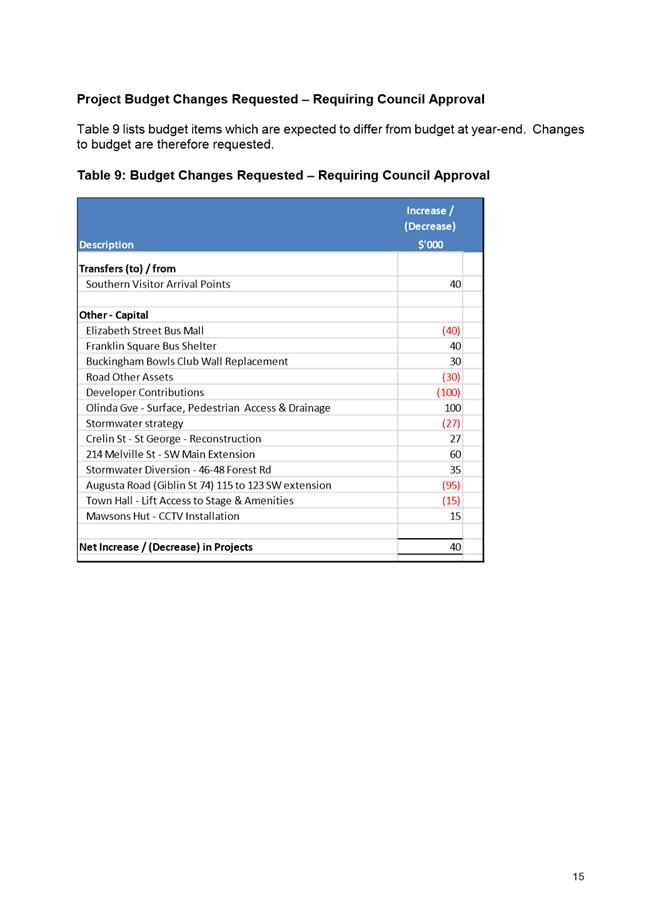

That: 1. The Council approve the changes to the 2017/2018 Estimates listed in tables 4, 5, 7 and 9 of Attachment A, the financial impacts of which are to decrease the underlying surplus by $0.78M, and to increase the cash balance by $0.88M. |

4. Background

4.1. The Financial Report as at 30 September 2017 is provided at Attachment A. The Financial Report provides details of:

4.1.1. The Council’s financial position as at 30 September 2017;

4.1.2. The result of operations for the first three months of the 2017/2018 financial year;

4.1.3. Forecasts for 30 June 2018; and

4.1.4. Progress towards the achievement of the Council’s financial sustainability outcomes.

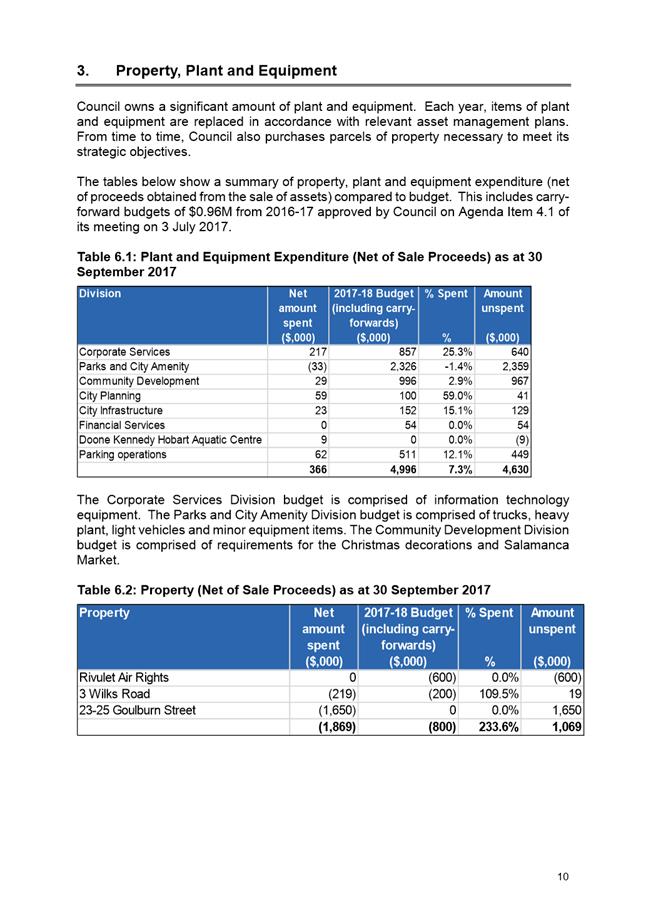

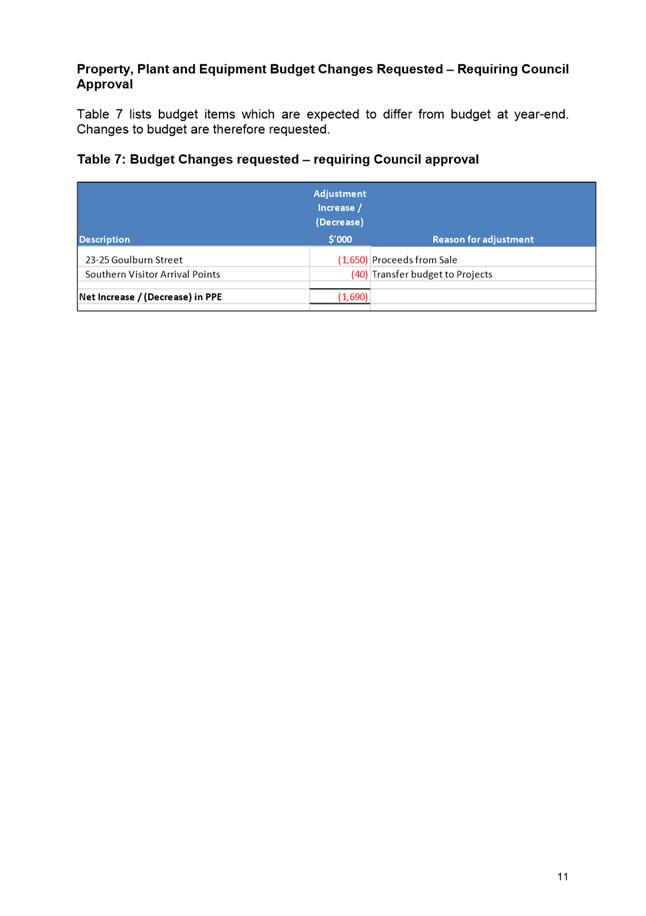

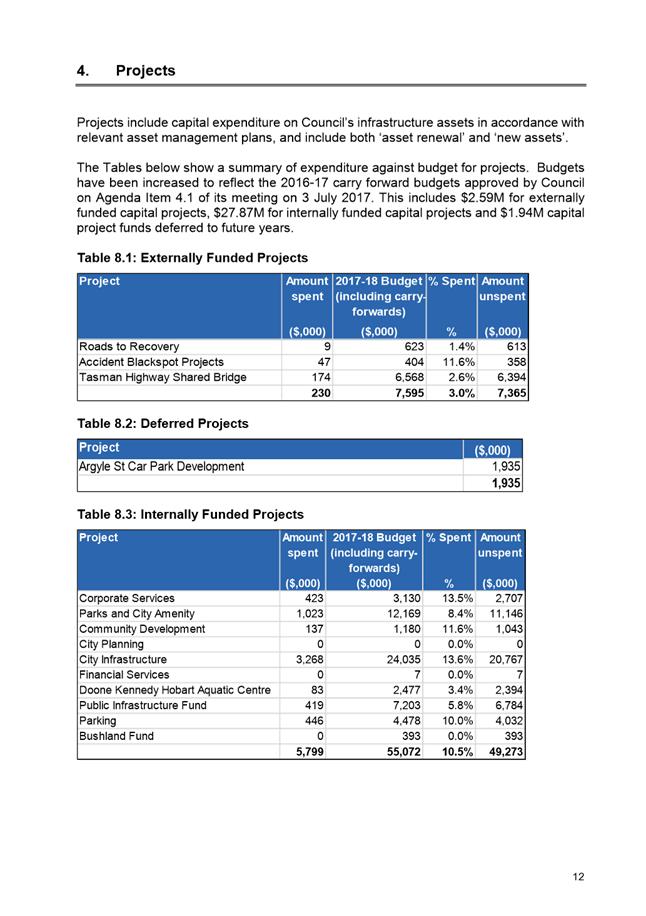

4.2. In accordance with the Council’s decision on Agenda item 4.1 of its meeting on 3 July 2017 unspent 2016/2017 capital funding has been carried forward to the 2017/2018 year.

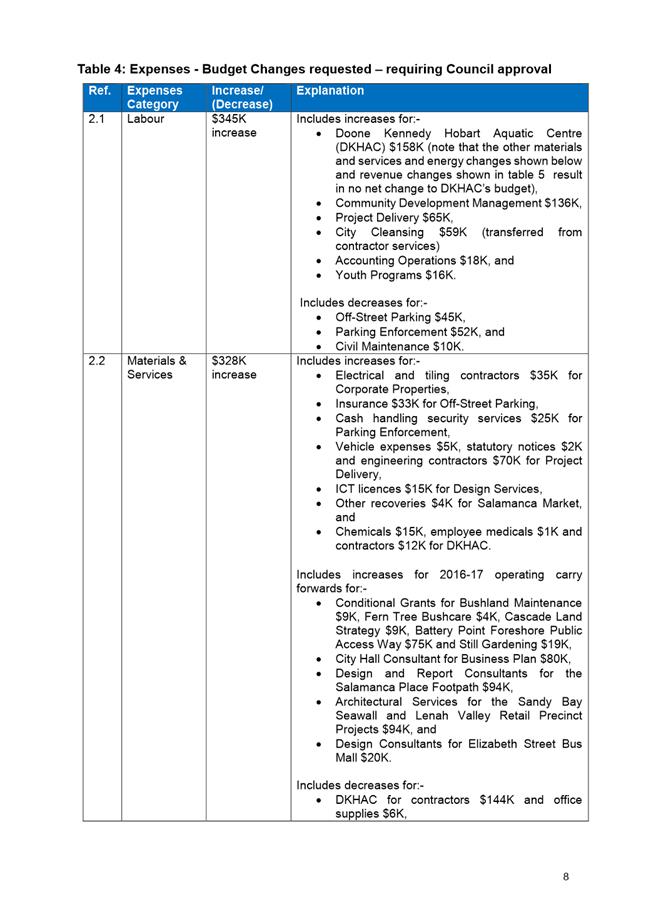

4.3. Operating carry forwards from 2016/2017 have not been approved by Council and are included in table 4 of Attachment A. These total $0.52M and will result in the forecast underlying surplus for 2017/2018 reducing from $1.44M to $0.92M.

5. Proposal and Implementation

5.1. The Financial Report seeks to have the 2017/2018 estimates (budget) amended to take account of expected differences from budget at 30 June 2018 (permanent variances).

5.2. It is proposed that the Council approve changes to the 2017/2018 Estimates as set out in tables 4, 5, 7 and 9 of Attachment A.

6. Strategic Planning and Policy Considerations

6.1. Goal 5 – Governance is applicable in considering this report, particularly Strategic 5.1 objective:

“The organisation is relevant to the community and provides good governance and transparent decision-making”.

7. Financial Implications

7.1. Funding Source

7.1.1. The proposed changes to the Estimates will result in net expenditure decreasing (and the forecast cash balance increasing) by $0.88M.

7.1.2. The increase in the forecast cash balance is due to an increase in property sale proceeds partly offset by an increase in operating expenditure.

7.1.3. The final cash balance may differ from the current forecast for the following reasons:

7.1.3.1. Current budget variances which are assumed to be timing variances (and therefore forecasts have not been amended) may prove to be permanent variances,

7.1.3.2. Further variances could arise during the remainder of the year, and

7.1.3.3. Capital expenditure could be higher or lower than forecast.

7.2. Impact on Current Year Operating Result

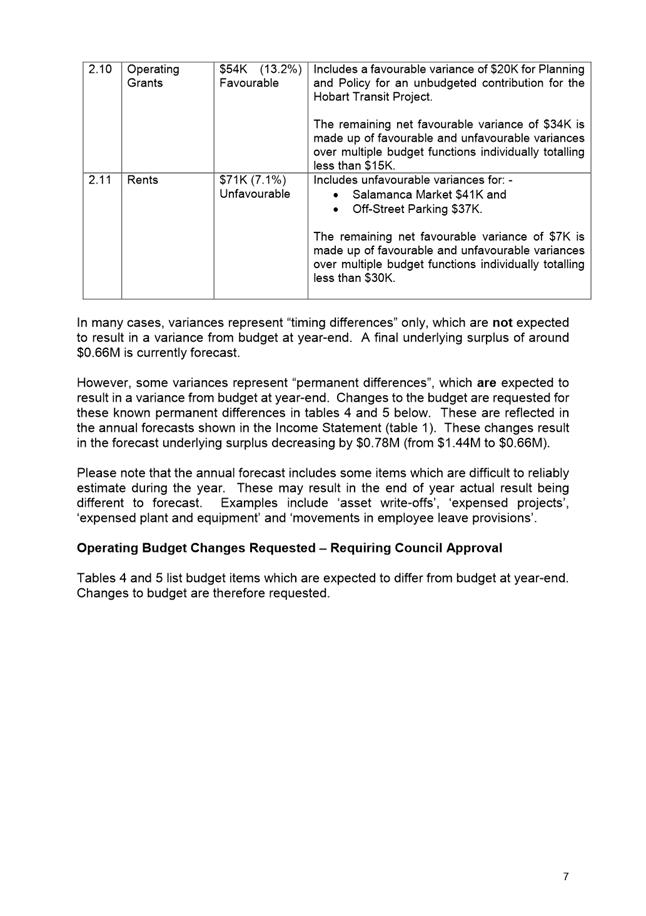

7.2.1. The impact of the proposed changes to the Estimates is to decrease the forecast underlying surplus by $0.78M (from $1.44M to $0.66M).

7.2.2. The decline in the forecast underlying surplus is mainly due to the inclusion of the 2016-17 operating carry forwards and higher than anticipated labour costs.

7.2.3. Whilst an underlying surplus of $0.66M is currently forecast for 2017/2018, expenses are currently favourable when compared to budget. If this position continues, the final result will exceed the current forecast.

7.2.4. The final operating result may differ from the current forecast for the following reasons:

7.2.4.1. Current budget variances which are assumed to be timing variances (and therefore forecasts have not been amended) may prove to be permanent variances; and

7.2.4.2. Further variances could arise during the remainder of the year.

7.3. Impact on Future Years’ Financial Result

7.3.1. The impact on future years’ underlying surpluses is difficult to estimate reliably because some changes may be ongoing, whilst others may not.

7.4. Asset Related Implications

7.4.1. No significant asset related implications are anticipated.

7.5. Financial Sustainability Indicators

7.5.1. Budget targets for six of Council’s eight financial sustainability indicators are expected to be achieved in 2017/2018.

7.5.1.1. Budget targets for both the ‘underlying surplus’ and ‘underlying surplus ratio’ are not expected to be achieved mainly due to the deterioration in the forecast underlying surplus which results mainly from higher than expected labour costs and operating carry forwards from 2016/2017.

7.5.1.2. Benchmarks are expected to be achieved for all financial sustainability indicators.

8. Legal, Risk and Legislative Considerations

8.1. Not Applicable.

9. Delegation

9.1. This matter is delegated to the Council.

As signatory to this report, I certify that, pursuant to Section 55(1) of the Local Government Act 1993, I hold no interest, as referred to in Section 49 of the Local Government Act 1993, in matters contained in this report.

|

Karelyn Stephens Budget and Reporting Manager |

Peter Jenkins Manager Finance |

|

David Spinks Director Financial Services |

|

Date: 9 November 2017

File Reference: F17/144428; 21-1-1

Attachment a: Financial

Report ending September 2017 ⇩ ![]()

|

Agenda (Open Portion) Finance Committee Meeting |

Page 60 |

|

|

|

14/11/2017 |

|

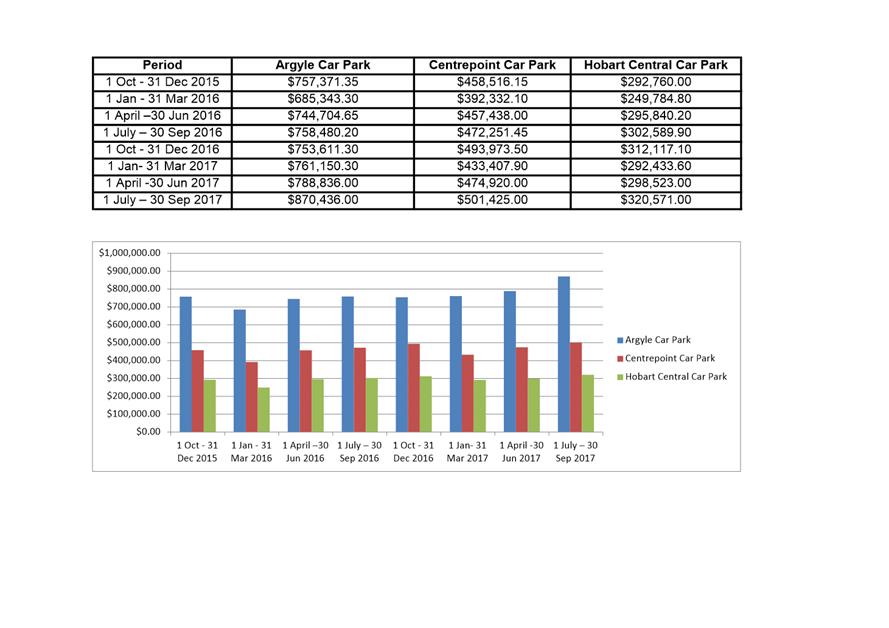

6.3 Occupancy Rates - Multi-Storey Car Parks

Memorandum of the Operations Manager - Car Parks, the Group Manager Parking Operations and the Director Financial Services of 9 November 2017 and attachments.

Delegation: Committee

|

Item No. 6.3 |

Agenda (Open Portion) Finance Committee Meeting |

Page 61 |

|

|

14/11/2017 |

|

Memorandum: Finance Committee

Occupancy Rates - Multi-Storey Car Parks

At the meeting of the Finance and Corporate Services Committee on 20 August 2013 (Open agenda item 13 - Questions Without Notice) Alderman Cocker requested the following:-

“Could Aldermen be provided regular updates on the occupancy rates of the Council Multi-storey car parks?”

The General Manager advised that Aldermen will be provided with the figures quarterly.

The initial quarterly car parks occupation rates report was provided to Aldermen at the meeting of the Finance and Corporate Services Committee on 22 October 2013 (item 8 - Closed agenda). The Committee resolved that the report be received and noted. In addition the Chairman informally requested that future reports include occupancy percentages.

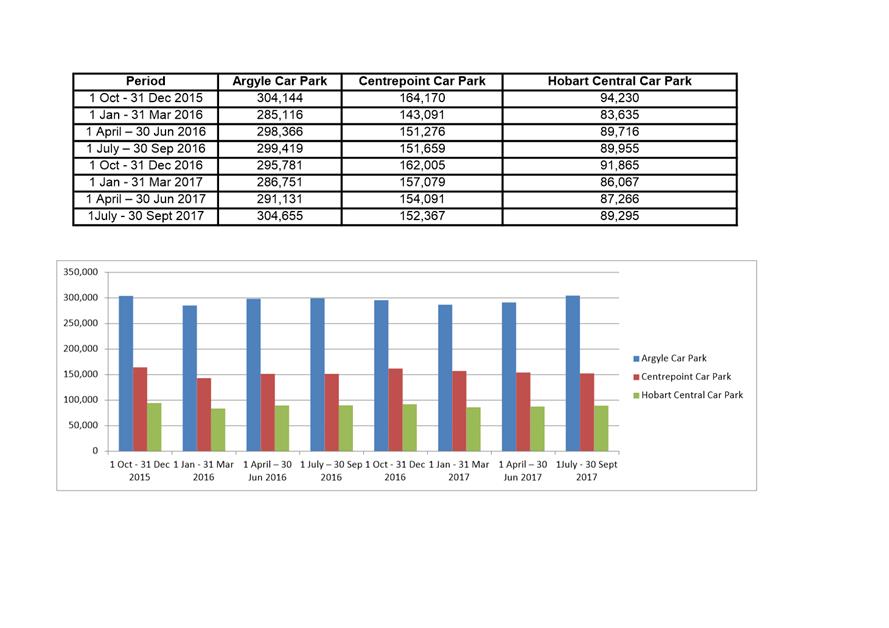

This report, for Quarter one (July - September) of the 2016-17 financial year contains:

· The occupancy rates and income of each of the three multi-storey car parks for the quarter ending September 2017 compared with the same period in 2016 (Table 1).

· Weekday hourly occupation percentages for each of the three multi-storey car parks for the same period (Attachment A).

· Three month overview of the occupancy rates and income generated by the Trafalgar Car Park through permit and early bird parking (Table 2).

Summary of results

The overall result across the car parks is:

· 1.07% decrease in vehicle usage; and

· Increase in income of 10.37%.

· Trafalgar car park continues to perform well, being slightly ahead of budget.

table 1

|

2016 |

ARGYLE STREET |

CENTREPOINT |

HOBART CENTRAL |

||||||

|

|

Cars |

Income |

Cars |

Income |

Cars |

Income |

|||

|

July |

98812 |

$257,332.10 |

50784 |

$163,951.55 |

30053 |

$98,977.80 |

|||

|

August |

101355 |

$233,305.20 |

50479 |

$146,081.60 |

30382 |

$98,128.00 |

|||

|

September |

99252 |

$267,842.90 |

52159 |

$162,218.30 |

29520 |

$105,483.20 |

|||

|

Totals |

299419 |

$758,480.20 |

153422 |

$472,251.45 |

89955 |

$302,589.00 |

|||

|

|

|||||||||

|

2017 |

ARGYLE STREET |

CENTREPOINT |

HOBART CENTRAL |

||||||

|

|

Cars |

Income |

Cars |

Income |

Cars |

Income |

|||

|

July |

100275 |

$281,334.00 |

50622 |

$159,483.00 |

29464 |

$100,141.00 |

|||

|

August |

102837 |

$296,635.80 |

53796 |

$173,501.50 |

30184 |

$114,626.00 |

|||

|

September |

101543 |

$292,467.10 |

50243 |

$168,441.50 |

29647 |

$105,804.00 |

|||

|

Totals |

304655 |

$870,436.90 |

154661 |

$501,426.00 |

89295 |

$320,571.00 |

|||

|

Argyle Street |

Centrepoint |

Hobart Central |

|||||||

|

Car park increase/decrease |

5236 |

$111,956.70 |

1239 |

$29,174.55 |

-660 |

$17,982.00 |

|||

|

1.74% |

14.76% |

0.80% |

6.17% |

-0.73 |

5.94% |

||||

|

Overall increase |

Cars |

5815 |

|||||||

|

Income |

$159,113.25 |

||||||||

Vehicle numbers increased slightly in all but Hobart Central, which decreased only slightly, however due to fee increase, income was up in all three car parks.

· The increase in revenue in Hobart Central income was due to an increase in early bird uptake during and a higher income per vehicle for short term vehicle parking.

· Income increased in Argyle Street car park by 14.76%, which reflects fee increase and longer stays.

· Income increased in Centrepoint car park of 6.17% which is a result of fee increases and a continuation of early bird parking.

Trafalgar Car Park

Parking Operations assumed operational responsibility of the 544 parking space Trafalgar Car Park on 1 July 2013. As at that date, 388 spaces were leased to permit holders who pay a monthly rental of either $255.00 or $275.00 depending on the conditions of their permit.

The goal is to fully occupy the car park with monthly tenants, however in the interim the void between actual and full occupancy is being filled with early bird parkers.

As at 30 September 2017, the number of spaces leased to permit holders was 483, with 61 vacant spaces being utilised by Early Bird parking. Saturday income decreased due to a decrease in Salamanca Market patrons taking advantage of the $6.00 all day parking fee also a decrease in early bird patronage of a weekday. As at 30 September 2017, the budget for the Trafalgar Car Park showed a favourable balance due to a decrease in expenditure through this period.

The income for the period 1 July 2017 – 30 September 2017 was split as follows:

Table 2

|

|

Jul-17 |

Aug-17 |

Sep-17 |

Total Income |

Budgeted Income |

|

Permits |

$98,890 |

96,700 |

$97,374 |

$289,964 |

$324,378 |

|

Early Bird |

$16,418 |

17,352 |

$15,453 |

$49,223 |

$56,000 |

|

Saturday |

$2,950 |

$2,256 |

$3,448 |

$8,654 |

$10,000 |

|

Total |

$115,258 |

116,308 |

$116,275 |

$347,841 |

$390,378 |

Car Park Occupancy Rates Jul – Sep 2017

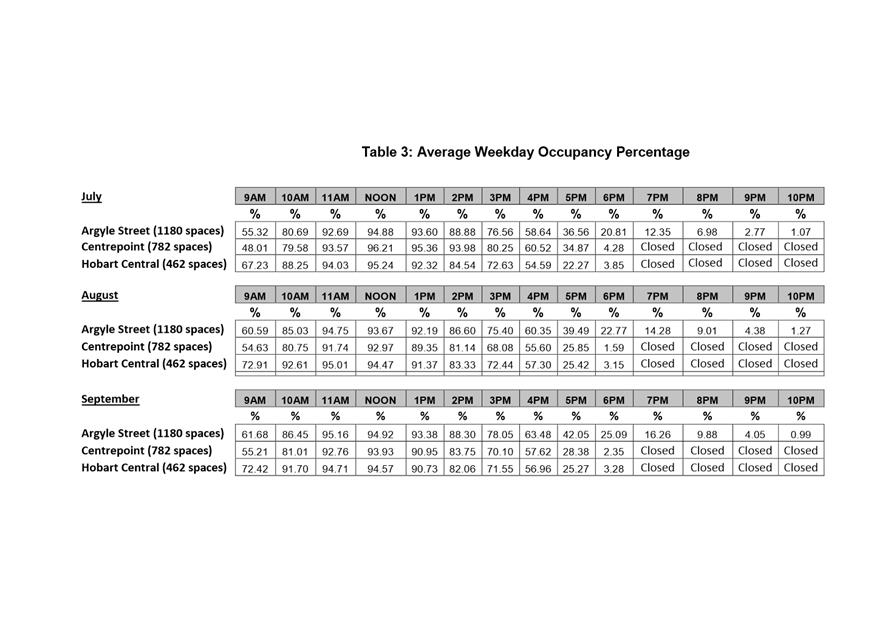

(See Attachment A)

During July Centrepoint Car Park recorded average occupation rates of 84.71% during the peak period of the day (11.00am – 2.00pm). Argyle Street averaged 92.51% and Hobart Central averaged 91.53 % for the same period.

In the following two month period (1 August 2017 – 30 September 2017) occupancy rates in all three car parks at the peak period of the day were higher – averaging at or above 90.30 %.

Hobart Central and Centrepoint car parks both accept “Early Bird” parking. During quieter periods the car park operators manually adjust the number of early birds they accept based on the vehicle usage statistics. The higher percentages of occupation in both of these car parks are reflective of this.

During the three month period vehicular traffic in Argyle Street car park remained constant, with the car park not quite filling during the three month period. The average number of vacant spaces available during the peak period of the day was in the vicinity of 102.

Centrepoint and Hobart Central car parks both had busy periods during July May and June both car parks filled but only momentarily. Accordingly, early birds were adjusted daily to ensure vacancies remained.

The usage statistics demonstrate that parking capacity remains available even during the busiest periods of the day, which in turn allows for parking availability on-street, thus giving options to parkers when in the City.

|

That the information contained in the memorandum of the Operations Manager – Car Parks, the Group Manager Parking Operations and the Director Financial Services of 9 August 2017 titled “Occupancy Rates – Multi-Storey Car Parks” be received and noted.

|

As signatory to this report, I certify that, pursuant to Section 55(1) of the Local Government Act 1993, I hold no interest, as referred to in Section 49 of the Local Government Act 1993, in matters contained in this report.

|

David Fox Operations Manager - Car Parks |

Matthew Tyrrell Group Manager Parking Operations |

|

David Spinks Director Financial Services |

|

Date: 9 November 2017

File Reference: F17/142668

Attachment a: Occupancy

Percentages ⇩ ![]()

Attachment

b: Occupancy

Rates ⇩ ![]()

Attachment

c: Financial

Performance ⇩ ![]()

|

Agenda (Open Portion) Finance Committee Meeting |

Page 68 |

|

|

|

14/11/2017 |

|

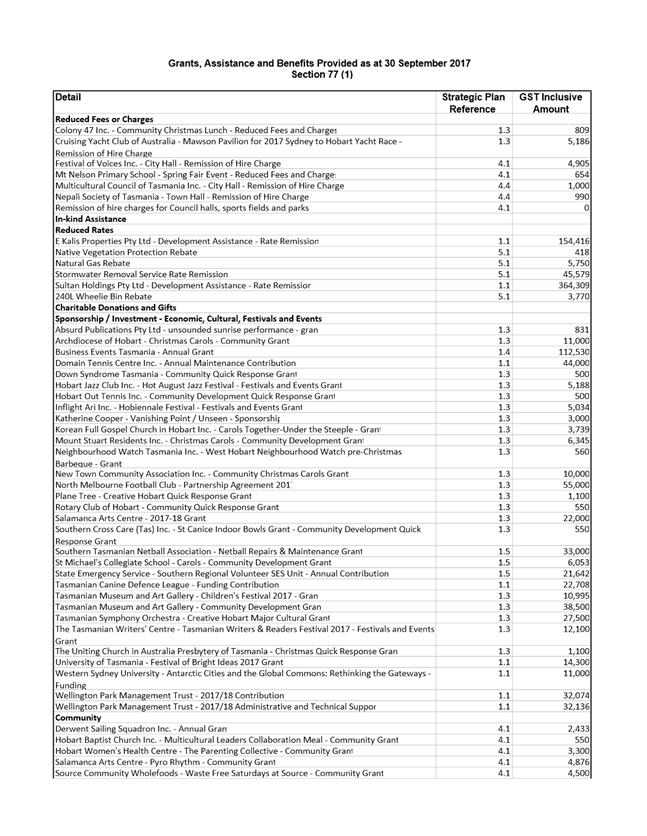

6.4 Grants and Benefits Listing as at 30 September 2017

Report of the Group Manager Rates and Procurement and the Director Financial Services of 8 November 2017 and attachments.

Delegation: Committee

|

Item No. 6.4 |

Agenda (Open Portion) Finance Committee Meeting |

Page 69 |

|

|

14/11/2017 |

|

REPORT TITLE: Grants and Benefits Listing as at 30 September 2017

REPORT PROVIDED BY: Group Manager Rates and Procurement

Director Financial Services

1. Report Purpose and Community Benefit

1.1. The purpose of this report is to provide a listing of the grants and benefits provided by the Council for the period 1 July 2017 to 30 September 2017.

2. Report Summary

2.1. At its meeting on 12 February 2015, the then Parks and Customer Services Committee requested that a quarterly report be provided for the information of the then Finance and Corporate Services Committee outlining all grants and benefits provided by Council Committees and Council.

2.2. A report is attached being for the period 1 July 2017 to 30 September 2017.

2.3. It is proposed that the Committee note the listing of grants and benefits provided for the period 1 July 2017 to 30 September 2017 and that these are required, pursuant to Section 77 of the Local Government Act 1993 (LG Act), to be included in the annual report of Council.

|

That the Finance Committee receive and note the information contained in the report titled “Grants and Benefits Listing as at 30 September 2017”.

|

4. Background

4.1. At its meeting on 12 February 2015, the then Parks and Customer Services Committee resolved that:

4.1.1. A quarterly report be provided for the information of the [then] Finance and Corporate Services Committee outlining all grants and benefits approved by Council Committees and Council.

4.2. At its meeting on 19 May 2015, the Finance Committee resolved that:

4.2.1. Details of all grants and benefits provided under Section 77 of the Local Government Act 1993 be listed on the City of Hobart’s website.

4.3. A report outlining the grants and benefits provided for the period 1 July 2017 to 30 September 2017 is attached – refer Attachment A.

4.4. Pursuant to Section 77 of the LG Act, the details of any grant made or benefit provided will be included in the annual report of the Council.

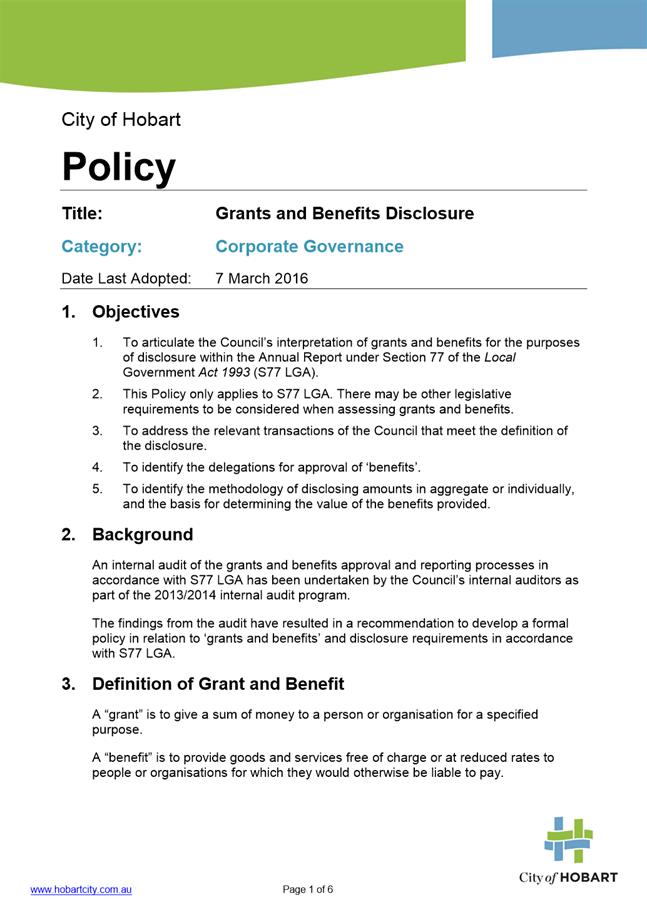

4.5. The listing of grants and benefits marked as Attachment A, has been prepared in accordance with the Council policy titled Grants and Benefits Disclosure – refer Attachment B.

5. Proposal and Implementation

5.1. It is proposed that the Committee note the grants and benefits listing as at 30 September 2017.

5.2. It is also proposed that the Committee note that the grants and benefits listed are required to be included in the annual report of the Council and will be listed on the City of Hobart’s website.

6. Strategic Planning and Policy Considerations

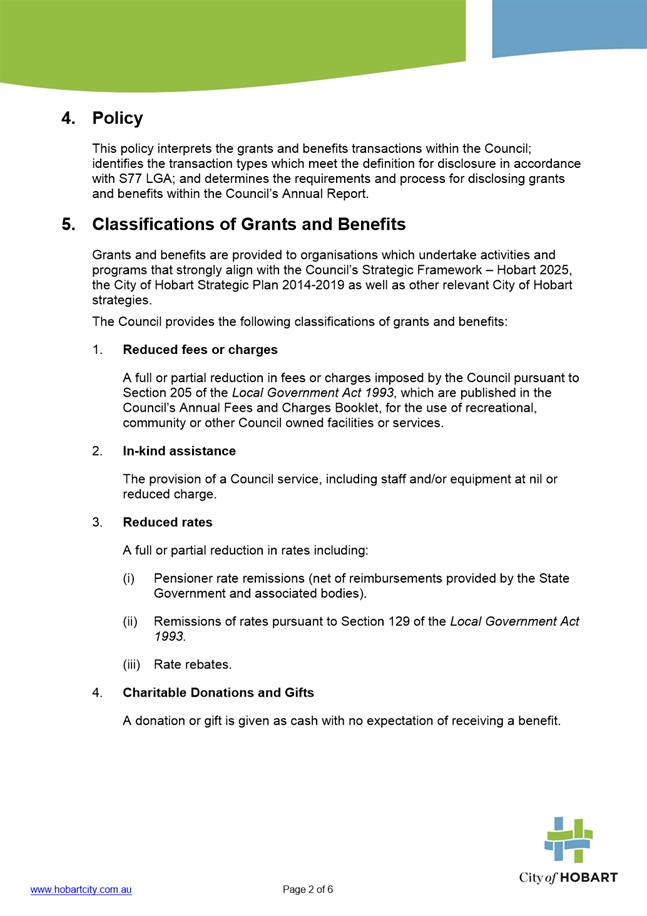

6.1. Grants and benefits are provided to organisations which undertake activities and programs that strongly align with the Council’s Strategic Framework – Hobart 2025, the City of Hobart Capital City Strategic Plan 2015-2025 as well as other relevant City of Hobart strategies.

6.2. The linkage between the City’s grants and benefits provided and the City of Hobart Capital City Strategic Plan 2015-2025 is referenced in Attachment A.

7. Financial Implications

7.1. Funding Source and Impact on Current Year Operating Result

7.1.1. All grants and benefits provided as at 30 September 2017 were funded from the 2017-18 budget estimates.

8. Legal, Risk and Legislative Considerations

8.1. The Council provides grants and benefits within the requirements of Section 77 of the LG Act as follows:

8.1.1. Grants and benefits

8.1.2. (1) A council may make a grant or provide a pecuniary benefit or a non-pecuniary benefit that is not a legal entitlement to any person, other than a councillor, for any purpose it considers appropriate.

(1A) A benefit provided under subsection (1) may include:

(a) in-kind assistance; and

(b) fully or partially reduced fees, rates or charges; and

(c) remission of rates or charges under Part 9 (rates and charges)

8.1.3. (2) The details of any grant made or benefit provided are to be included in the annual report of the council.

8.2. Section 72 of the LG Act requires Council to produce an Annual Report with Section 77 of the LG Act providing an additional requirement where individual particulars of each grant or benefit given by the Council must be recorded in the Annual Report.

8.3. Section 207 of the LG Act provides for the remitting of all or part of any fee or charge paid or payable.

8.4. Section 129 of the LG Act provides for the remitting of rates.

9. Delegation

9.1. This report is provided to the Finance Committee for information.

As signatory to this report, I certify that, pursuant to Section 55(1) of the Local Government Act 1993, I hold no interest, as referred to in Section 49 of the Local Government Act 1993, in matters contained in this report.

|

Lara MacDonell Group Manager Rates and Procurement |

David Spinks Director Financial Services |

Date: 8 November 2017

File Reference: F17/145044; 25-2-1

Attachment a: Grants

and Benefits Listing as at 30 September 2017 ⇩ ![]()

Attachment

b: Council

Policy - Grants and Benefits Disclosure ⇩ ![]()

|

Agenda (Open Portion) Finance Committee Meeting |

Page 80 |

|

|

|

14/11/2017 |

|

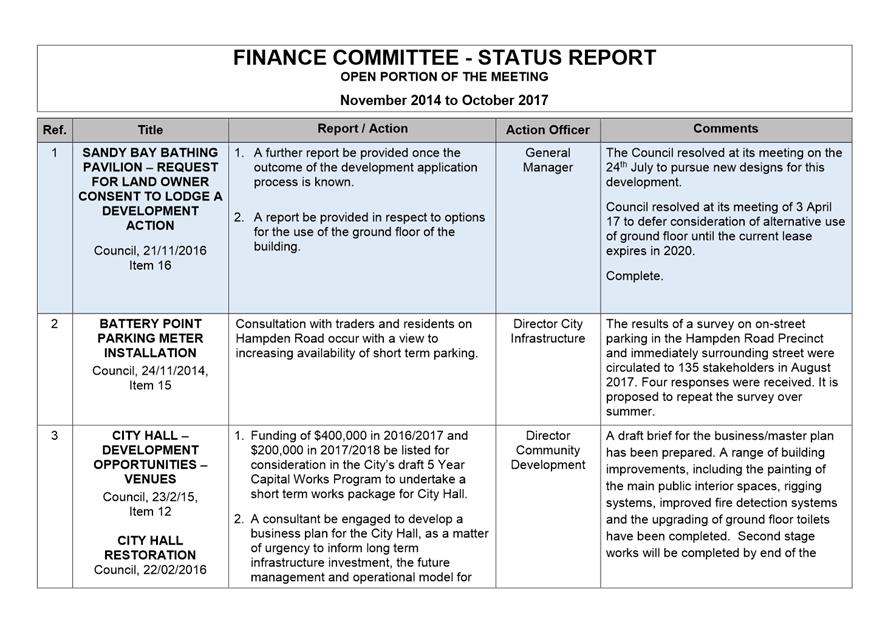

A report indicating the status of current decisions is attached for the information of Aldermen.

REcommendation

That the information be received and noted.

Delegation: Committee

|

|

Agenda (Open Portion) Finance Committee Meeting |

Page 89 |

|

|

14/11/2017 |

|

Section 29 of the Local Government (Meeting Procedures) Regulations 2015.

File Ref: 13-1-10

An Alderman may ask a question without notice of the Chairman, another Alderman, the General Manager or the General Manager’s representative, in line with the following procedures:

1. The Chairman will refuse to accept a question without notice if it does not relate to the Terms of Reference of the Council committee at which it is asked.

2. In putting a question without notice, an Alderman must not:

(i) offer an argument or opinion; or

(ii) draw any inferences or make any imputations – except so far as may be necessary to explain the question.

3. The Chairman must not permit any debate of a question without notice or its answer.

4. The Chairman, Aldermen, General Manager or General Manager’s representative who is asked a question may decline to answer the question, if in the opinion of the respondent it is considered inappropriate due to its being unclear, insulting or improper.

5. The Chairman may require a question to be put in writing.

6. Where a question without notice is asked and answered at a meeting, both the question and the response will be recorded in the minutes of that meeting.

7. Where a response is not able to be provided at the meeting, the question will be taken on notice and

(i) the minutes of the meeting at which the question is asked will record the question and the fact that it has been taken on notice.

(ii) a written response will be provided to all Aldermen, at the appropriate time.

(iii) upon the answer to the question being circulated to Aldermen, both the question and the answer will be listed on the agenda for the next available ordinary meeting of the committee at which it was asked, where it will be listed for noting purposes only.

|

|

Agenda (Open Portion) Finance Committee Meeting |

Page 90 |

|

|

14/11/2017 |

|